Short-term interest rate futures (STIR futures) are one of the largest and most liquid financial markets in the world. The two main exchange-traded contracts, the Eurodollar and Euribor, regularly trade in excess of one trillion notional dollars and euros of US and European interest rates each day.STIR futures have some very unique characteristics, not found in most other financial products. Their structure makes them very suitable for spread and strategy trading and relative value trading against other instruments such as bonds and swaps.STIR Futures is a handbook for the STIR futures market. It clearly explains what they are, how they can be traded, and where the profit opportunities are. The book has been written for both aspiring and experienced traders looking for a trading niche in a computerised marketplace, where all participants trade on equal terms and prices.This fully revised and updated second edition now includes:- Details on the effects of the financial crisis on STIR futures pricing and trading.- An in-depth analysis of valuation issues, especially the effects of term and currency basis when relatively traded to other financial products.- A new section on using STIR futures to hedge borrowing liabilities.- An in-depth analysis of relative value trades against bond and swap derivatives.- Trading synthetic FX swaps using STIR futures.Plus updated case studies and examples throughout and an even better explanation of the basics.This book offers a unique look at a significant but often overlooked financial instrument. By focusing exclusively on this market, the author provides a comprehensive guide to trading STIR futures. He covers key points such as how STIR futures are priced, the need to understand what is driving the markets and causing the price action, and provides in-depth detail and trading examples of the intra-contract spread and strategy markets and cross-market relative value trading opportunities.An essential read for anyone involved in this market.

- 280 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

1. STIR Futures

Introduction to STIR Futures

What are futures?

Futures are derivatives, meaning that they derive their value from an underlying asset like a commodity such as oil or a financial asset such as a bond, stock index or interest rate.

Futures are traded on regulated futures exchanges such as Liffe in London or CME in the United States and are structured as legally binding contracts. This means a counterparty to a trade undertakes to physically or notionally make or take delivery of a given quantity and quality of a commodity at an agreed price on a specific date or dates in the future.

What are STIR futures?

STIR futures are a variety of future contract where the underlying asset is a Short Term Interest Rate.

A short-term interest rate (STIR) futures contract can be defined as:

- a legally binding contract

- notionally to deposit or borrow

- a given amount of a specified currency

- at an agreed interest rate

- on a specific date in the future

- for a specified period.

For example, the three-month Euribor futures contract traded on Liffe is:

- a legally binding contract

- notionally to deposit or borrow €1m

- at an agreed interest rate

- on the delivery date

- for a nominal 90-day period.

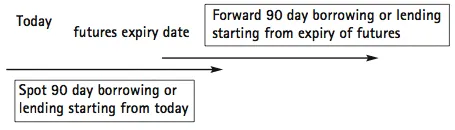

This effectively means that a Euribor future provides a mechanism for locking in a forward borrowing or lending rate for a specified amount of euros on a given date for a nominal 90-day period.

This contrasts with a spot borrowing or lending for 90 days, which would be fully funded and unsecured, starting today for 90 days.

Similarities with other futures contracts

STIR futures are similar to other futures contracts in that they are:

- traded on regulated futures exchanges that provide the legal framework, contract specifications and the trading mechanism

- settled via a central counterparty to remove credit risk between market participants

- characterised by a unit of trading, tick size and settlement procedures.

Differences with other futures contracts

STIR futures differ from other futures in that they:

- have multiple delivery cycles, sequential to several years, covering a broad spectrum of the near-dated yield curve; this means that STIR futures have many different expiries trading simultaneously within the same contract, which allows a unique trading perspective

- have highly similar risk characteristics between delivery cycles

- include spread trading and other trading strategies, allowing many different trade permutations and ideas, with different risk profiles

- are arguably the most liquid class of futures by nominal value.

Derived from interest rates

Futures are broadly classed as derivatives since they are derived from another product; and are called futures since they are not for immediate purchase or sale but at a future date.

STIR futures are derived from interest rates covering a deposit period of three months, extending forward from three months up to ten years. These interest rates refer to near-term money market interest rates which are comprised of the unsecured inter-bank deposits markets (also known as the depo market). From these money markets comes the daily fixing of London Inter-Bank Offered Rate (LIBOR), or its European equivalent: European Inter-Bank Offered Rate (EURIBOR). These are the reference rates that are used to settle STIR futures on expiry.

LIBOR

The London Inter-Bank Offered Rate is defined as the rate of interest at which banks borrow funds from other banks in reasonable market size (e.g. $5m) in the London inter-bank market just prior to 11am London time. It is considered a key benchmark rate in the financial markets, having been in widespread use since 1984. LIBOR covers ten currencies with 15 maturities up to 12 months and is used as the basis for pricing a variety of interest rate products such as floating-rate notes, interest rate swaps, interest rate caps and floors and exchange-traded STIR futures and options.

Reuters acts as official fixing agent on behalf of the British Bankers Association. It determines LIBOR fixings by obtaining rates from contributor banks prior to 11am and these contributed rates are ranked in order, with the top and bottom quartiles removed and the remaining rates arithmetically averaged.

EURIBOR

EURIBOR is very similar to LIBOR but is the market standard for the euro. It was established by the European Banking Federation and ACI with the first EURIBOR rates quoted on 4 January 1999.

The fixing process is similar to LIBOR, with the following differences:

- panel of around 44 of the most active banks in the euro zone area

- this leads to a greater ratio of smaller banks to larger banks in comparison to LIBOR

- computed as an average of quotes for 15 maturities with the top and bottom 15% rejected (rather than top and bottom 25% as with LIBOR)

- published at 11am (CET) daily.

The LIBOR fixing scandal (2012) will lead to a regulatory reform of the LIBOR and EURIBOR fixing processes. It is highly likely that responsibility for LIBOR will be removed from the British Bankers Association and there will be changes to the fixing methodology.

Movement of interest rates

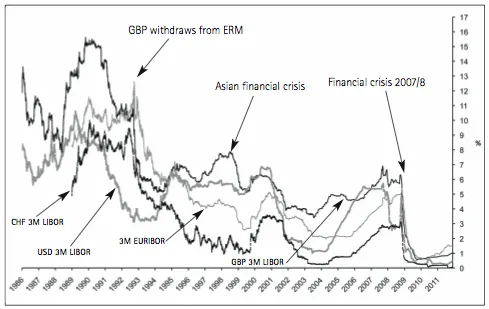

The following chart shows how these LIBOR rates for UK, USA, Swiss and EURIBOR rates have moved over time and how they have been influenced by major events.

It can be seen that country interest rates are influenced by the state of their economies and market expectations for interest rate levels in the future. Sharp movements are often caused by economic or political events. UK interest rates fell sharply in 1992 when sterling withdrew from the European Exchange Rate Mechanism (ERM) and global rates were cut sharply after 9/11 in 2001, after the tech market collapse in 2002 and the credit crunch in late 2008.

Fig. 1.1 – Three-month LIBOR rates for GBP, USD, CHF and three-month Euribor for EUR

Traded on exchanges

STIR futures are traded on regulated futures exchanges, such as London International Financial Futures Exchange (Liffe) in the UK or the Chicago Mercantile Exchange (CME) in the USA. Nowadays virtually all contracts are transacted electronically via computerised trading. These exchanges provide the mechanism and legal framework for access to their particular markets.

Different exchanges have different STIR products, usually determined by their geographical origins. Euribor futures (based on European interest rates) are traded on Liffe and the Eurodollar futures (based on US interest rates) are mainly traded on CME. However, competition between exchanges can mean that popular contracts are sometimes quoted on several exchanges.

Buyers and sellers of STIR futures connect to these exchanges, either directly as members of the exchange or indirectly using a member as an agent. These buyers and sellers can be banks, corporate treasurers or speculative traders such as hedge funds, proprietary groups or individuals, formerly called locals but now known as liquidity providers (LP). These speculative traders attempt to make money from price action, whereas banks and treasurers tend to use the markets as hedging tools to risk-manage other interest rate exposures.

Exchange-traded futures are often portrayed as having no inherent counterparty risk. Generally this is true for exchange members, since credit risk between the counterparties to a trade is removed by the intermediation of a highly capitalised clearing house, which effectively guarantees each side of the deal, meaning that a buyer of a futures contract need not worry about the creditworthiness of the seller and vice-versa.

However, traders who are not exchange members but use the services of one to access the markets can be at risk of default by the exchange member.

Where and how are they traded

Futures on short-term interest rates are traded by exchanges all over the world, including Euro...

Table of contents

- Cover

- Publication details

- About the Author

- Preface

- Introduction

- 1. STIR Futures

- 2. Mechanics of STIR Futures

- 3. Trading STIR Futures

- 4. Trading Considerations for STIR Futures

- Endgame

- Ten Rules for Trading STIR Futures

- Appendices

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access STIR Futures by Stephen Aikin in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.