Find a method to evaluate stocks— and build a record of impressive returns

Short Selling for the Long Term describes the methods used by Joseph Parnes, President of Technomart, to obtain consistent returns in the stock market. Most investors fail to exceed the returns represented by the Standard and Poor's Stock Index, but Parnes often does using his investment philosophy. This book outlines his method of stock assessment, providing an understandable formula. If the formula tells a reader to buy a stock, then, as explained, there is a significant chance that stock will go up. If the formula tells a reader to short a stock, then the book shows how there is a significant chance that the stock will go down.

Parnes advocates the use of short selling as a long-term strategy in combination with long positions, so advisors and individual investors alike can profit in both rising and falling markets. While most investing books focus on how to make money over the long term in a rising markets, Parnes's focus on short selling as a way of capturing volatility sets this book apart from the crowd. He offers insights into the difference between option trading and shorting which make his system useful in both type of markets.

• Profit in a bear market

• Borrow the stock you want to bet against

• Sell borrowed shares

• Learn the secrets of long-term short selling strategy

• Buy shares back and close by delivering at the new, lower price

Short Selling for the Long Term is essential reading for investment advisors, fund managers, and individual investors.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

This book discusses my methods for evaluating the market, which differ significantly from those of many money managers. Succinctly stated, I invest—I do not trade. This book is an explanation of my method of investment.

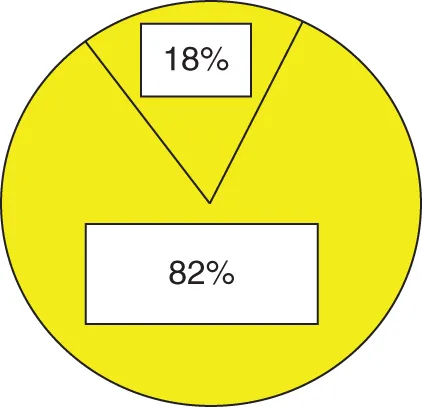

Individual investors have individual needs. This book describes a methodology that allows an investor to determine if this investment philosophy is compatible with their own needs. Some people are risk averse while others want income. Only you will know what works best for you. This book may provide you with the information that you need to help you with your decisions. Please see Figure 1.1.

Figure 1.1 The short and long positions in composite portfolios for 2016.

The pie chart in Figure 1.1 represents the short (18%) and long (82%) positions in composite portfolios for 2016. The long-to-short ratio is 4.8. This ratio changes year to year, depending on market conditions. In a bear market, there are more short positions than 18%, and in a bull market, there are more than 82% long positions.

The role of any investment advisor is to supply private and institutional clients with practical investment advice. This advice may encompass experience across a broad array of industries, with a special focus on growth companies and short-selling strategies. Many of my investment recommendations have appeared in Barron's, Forbes, Investor's Business Daily, and Modern Trader. I have been featured in and contributed to a broad array of media, including Bloomberg TV, CNBC, and First Business News. I have been recognized as one of the top wealth managers in 2004–2012 by Bloomberg Wealth Manager and featured in Barron's (Figure 1.2) and Forbes. These media outlets all seem to be interested in my investment approach. I was also invited by the Bank of England to be the keynote speaker at the Financial Markets Law Committee (FMLC) meeting in London. This committee was created by the Bank of England and was chaired by Lord Hoffmann, a former member of the Appellate Committee of the House of Lords, which is now called the Supreme Court, and is most analogous to the US Supreme Court.1

I employ a proprietary bottom-up approach to investing that focuses on company research, fundamentals, technical analysis, and cash flow to evaluate superior opportunities for long and short investment opportunities. Strategies may include sector balancing, growth, cash flow, bonds, income, short selling, risk aversion, and other investment strategies. These terms will be explained later, in appropriate sections of the book. I focus on in-house company research to evaluate the fundamentals, technical analysis, and cash flow on the various issues selected. In-house company research often carries none of the biases of research from institutional investors, which often have significant holdings in the companies that they recommend for purchase, which is out of date by the time it is published.

I discourage investors from becoming clients if they depend on the money they want us to manage for living expenses. If you have certain minimum living expenses that require a return on investment, these must be secured first. If you need funds for living expenses, this creates a situation where the investment philosophy of the client is counter to my own investment philosophy. This day-to-day need for funds clouds the judgment of an investor. If you are going to invest for the future, and invest to grow your assets, do not use money you need to live. Simply stated, do not invest money if you cannot afford to lose it. Only put surplus capital into an investment fund. Ideally, you should invest, and check in routinely to see how you have done, but do not worry about short-term changes. The current market conditions that are impacted by global traders creates a new environment and produces a more volatile market than in the past. The natural market fluctuations, retractions, hiccups, sell-offs, and so on are to be expected. Do not let the volatility impact your investment judgment. You will want to sell off when there is a short-term profit, rather than hold for the long term. When an issue drops 15–20%, it takes a truly sophisticated investor to see the long-term picture by seeing the drop as an opportunity.

Trading is not the hallmark of my strategy. It is my belief, developed through years of experience, that maximum returns will be lost in a short-term trading strategy. Very often, once a position is traded with the thought of repurchasing the position later, some other factors have intervened and the repurchase opportunity is lost. Many times, once a position is sold out, not only will there be a tax burden to the investor but discipline is needed to reacquire the position. The advantages of having held the position at a lower price are often lost with a repurchase strategy. The inconsistency of traders in repeating their previous gains would subject the investors to a new element of the risk. Therefore, my trading strategy is best described as “not trading.” A company with solid fundamentals, good management, a strong cash position, little or no debt, a reasonable price-to-earnings ratio compared to its peer group, and a strong market position compared to its peer group has all the elements of a solid investment. This type of company will be able to ride out various market bumps, corrections, and sell-offs, and should be held for the long term. The shortsighted approach of “take my profit and run” probably reduces the overall return on investment when calculated over a six- or eight-quarter period.

Being a wealth manager, my intent is to maximize performance and its value in the time frame of one to three years, or even five years, by a double- to triple-digit increase in asset value invested. I select long positions based on a strategy of following the technical analysis over time, and fundamentals. My clients' accounts are customized commensurate with the objectives of the investors. I personally and actively evaluate 40 to 60 issues. Then, based on the requirements of the individual client, I usually narrow down investments in a single portfolio of 18 to 24 positions, dividing the assets in large accounts into $30,000–$60,000 or higher tranches. Basically, the more positions in the account, the less the volatility. This degree of diversity helps weather the normal market fluctuations while capitalizing on and maximizing the profit potential of individual issues.

The aggregate portfolio of a client varies subject to risk tolerance and objectives of the investors and the size of the portfolio. I review the movements, corrections, and retractions of each issue. Near-term objectives, intermediate objectives, and stop losses are set and reassessed on each issue to avoid being “stopped out.” For individual issues, I look at 10-day, 50-day, and 200-day moving averages, which are viewed as a tool to evaluate the momentum of the various issues, knowing full well that the deviations, plunges, and down-gaps may involve institutional, hedge fund, or mutual fund investors taking positions or eliminating positions (these terms and their significance will be explained in the appropriate sections of this book). When the momentum of a stock overextends its respective movements above the set barriers or resistance lines, I know it is time to reevaluate that stock. On long positions, I look for relative strength as well as flow movements: short positions of institutional investors play a strong part in that evaluation.

Shorts are difficult to master, primarily because of the scarcity of float/liquidity, that is, the number of shares available. Ideally, I maintain 10% to 15% of the initial stock value as a stop loss in short trades, depending on the volatility of the issue. In volatile long positions, I evaluate the stop loss, depending on the retraction, to see if there is a change in the fundamentals of the company, or if the retraction is in response to some external event, such as commentaries made by short sellers, to drive the price of the stock down. Eventually, due to the strength of the fundamentals of the company, the short sales will dry up and the price will rise due to covering of the shorts. By being aware of certain market investors or traders, such as high-frequency traders (HFTs), computerized high-frequency trading (HFC), institutional traders, and algorithm traders, who capitalize on volatility to enhance their performance, I look for them to cover their short position, which typically drives a stock to even higher prices. Contrary to the herd mentality, I take note when the level of bullishness on the subject issue becomes overextended. I focus on technical elements on an issue when the following elements become transparent: overheating, primary/secondary support level, breakdown, topping (on individual issues in the general market/sectors), and trading charts that show ridging/head and shoulder, plunging gaps, reverse cup with handles, volume, deterioration of accumulation/distribution mode, length of the distribution, downward penetration on the 50-day and 200-day moving averages, and formation of the “death cross” pattern. All these terms and their applications and implications will be described in the pages that follow. Other data of importance in short selling are short interest in the New York Stock Exchange/NASDAQ composites, put/call ratio, major indices trends, and volatility index.

While a home-run investment in the stock market is usually spectacular, I am not looking for the “big kill.” Those astounding investments with 500% or 1,000% returns in three months do happen, but they happen far less frequently than people taking losses. I always remind people that for many years, Babe Ruth held the Major League Baseball record for the most home runs in a single season, hitting 60 homers in 1927, while playing for the New York Yankees. But in his effort to send the ball out of the park, he also had a huge number of strikeouts, with 89 in the same year. In 1961, Roger Maris hit 61 home runs with 67 strikeouts. Compare that to Reggie Jackson, who hit 47 home runs in 1969 with 142 strikeouts, or Will Stargell, who in 1971 hit 48 home runs but had an astounding 154 strikeouts. You often hear about the great number of home runs of these players, but rarely do people mention the strikeouts, or, even more importantly, the ratio of strikeouts to home runs. When reexamined in those terms, Ruth had a strikeout-to-home-run ratio of 1.48, while Maris had a 1.09 ratio, Jackson had a 3.02 ratio, and Stargell had a 3.20 ratio. This means that Stargell was more than three times as likely to strike out as he was to hit a home run while Maris had a little less than even shot at it. Now we are getting down to useful numbers and into the realm of predictive analytics. If you invest with a money manager, is he going to have the Roger Maris result or the Will Stargell result?

CHAPTER 4: Explanation of the Use of the 50-Day Moving Average and 200-Day Moving Average

CHAPTER 5: The Theory Behind the “Parnes Parameters”: Using Pattern Recognition, Retrospective Analysis, and Bayesian Analytics

CHAPTER 6: Variables to Consider for the Parnes Parameters

CHAPTER 7: Shorting for the Long Term

CHAPTER 8: A Case Study for a Stock I Shorted for the Long Term—Chipotle

CHAPTER 9: Case Studies for Integrating Shorts for the Long Term with Longs

CHAPTER 10: Modern Trader Charts

Glossary

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Short Selling for the Long Term by Joseph Parnes in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.