![]()

Chapter 1

Sustainability Context

THE NEED AND DEMAND FOR CHANGE has made sustainability reporting a critical success factor in business. Reporting is not only a key ingredient in a 3.4 trillion dollar sustainability sector growing at a rate of 25% per annum, but also the marshalling and distribution of the world’s 200+ trillion dollar wealth.

The journey

It is useful to frame the reporting journey in terms of the four principles of GRI reporting: sustainability context, inclusivity (stakeholder), materiality, and completeness (SIMC). It should be noted that this terminology is taken from the language of accounting. This is deliberate because sustainability reporting is simply an evolved form of corporate management accounts. Whereas once the financial accounts told us 100% of what we needed to know about the well-being of a company, it now only represents 20% of the information needs of stakeholders, with investors, for instance, needing information on social, environmental and economic performance to appreciate the short-, medium-and long-term prospects of an organisation.

A sustainability report sets out an organisation’s vision and intent; it states what environmental, social, governance and economic aspects are relevant to the organisation and its stakeholders, and the activities to improve performance in these areas. The common metrics used enable reporting organisations to be assured and ranked based on quality.

The journey to develop the actual report begins with understanding the ‘sustainability context’. The organisation should be able to present its performance in the wider context of sustainability issues. This involves appreciation of, and discussion on, the limits and demands placed on environmental or social resources at the sector, local, regional and global level. These include the following:

Climate change – Anthropogenic greenhouse gas emissions contributing to sea level rise, degradation of biodiversity and endangering food and water resources.

water – Aquifers and courses are being polluted, and scarce potable supplies are diminishing.

waste – The hierarchy is 1) prevention, 2) reuse, 3) recycling, 4) recovery, 5) disposal. Government policy in the UK and increasingly globally seeks a circular economy, a closed loop, cradle to cradle. Japan are the number one circular economy spending 7% of GDP in a £163 billion PA industry employing 650,000 people. China and USA are similar. Sadly, the UK are outside the top 10 for research (Circular Economy Taskforce Report, 2013). Waste-to-energy best practice includes recycling, composting, reusing metals and generating fuel.

wealth distribution – 85% of global wealth belongs to the richest 10%; the poorest half of the world’s population own 1% of global wealth, and the gap between rich and poor continues to grow. 400 million Africans earn less than $1.25 a day. Sustainability can enable and build different models so that growth is not a race to the bottom.

population – 7 billion and rising placing greater pressure on resources. The last two years’ growth is equivalent to twice the population of Holland.

Conservation – The need to preserve natural ecosystems and the environment.

pollution – Toxic chemicals into the air and sea, i.e. atmospheric aerosol loading and chemical pollution including radioactive compounds, heavy metals and organic compounds. Singapore recently had particulate levels 10 times higher than the exposure guidelines set out by the WHO due to smog caused by the burning of forests in Indonesia.

Once an organisation appreciates its sustainability context it is able to have more meaningful and strategic dialogue with its stakeholders. This is the requirement of ‘inclusivity’: the need to identify and engage very carefully as it is stakeholders who will identify the aspects selected as ‘material’.

‘Completeness’ relates to the ability of the organisation to command and control the material aspects based on the boundaries identified. It will be the impacts arising from these that enable stakeholders to assess an organisation’s performance.

The acronym I call ‘CRAB TC’ below lists the criteria for assessing the quality of the reporting process:

Clarity means readers should be able to understand the report and its contents.

Reliability means that the information can be laid out so that it can be checked.

accuracy means data should be accurate and capable of check and reproduction to achieve similar results.

Balance means the report should be an unbiased picture of the organisations performance.

Timeliness means publishing on a consistent schedule.

Comparability is where information is comparable with past performance years and if possible to other organisations.

Preliminaries

Sustainability Leader and Coordinator

This is the person in the organisation responsible for coordinating sustainability performance targets and coordinating sustainability report production. Ideally the Chief Executive or Chief Sustainability Officer is the sustainability leader and if they are unable to do it themselves they manage a member of staff with day-to-day responsibility for organising and co-ordinating and making sure that the sustainability reporting process is established, implemented and maintained and that documentation is produced in between meetings. The sustainability leader does not need to be an expert in sustainability issues. It is more important that they understand organisational culture, structure and operations, and that they have good networking and project management skills.

A Sustainability Team comprising representatives from the functional departments, should meet periodically to manage progress against targets, and ensure that staff are participating in the process by attending workshops and taking follow-up action as necessary. Senior management and decision-makers should be constantly involved and meet especially at the kick-off meeting and materiality validation that determines which indicators are the highest priority for the organisation to carry forward to the monitoring phase of the reporting cycle. (More on the kick-off meeting and materiality in the following chapters.) Regular review meetings should assess opportunities for improvement, SMART methods of data/information collection, objectives and target, monitoring, follow up on previous sustainability reports and meeting actions, and corrective actions, audits, etc. These should all be minuted. Schedule 1 provides the complete time line and the activities the sustainability leader must ensure are managed.

It is important that the Sustainability Leader does not try to do it all and that staff and other stakeholders are involved and understanding from the outset of the concept that everyone is responsible for their own ‘Sustainability’ performance.

Prepare the business case – Board approval

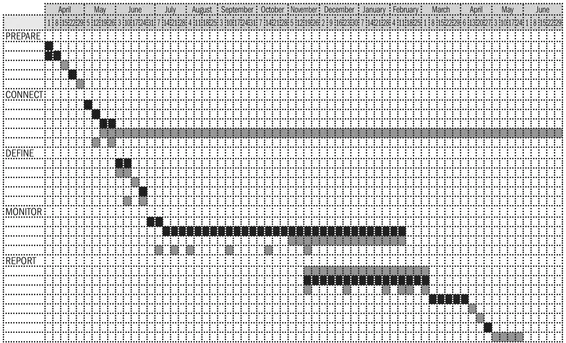

This section is not about the business case for reporting. This is about seeking board approval, a critically important governance activity where many would benefit from guidance. The activities in orange on the critical path analysis (CPA) in Figure 2 below shows the key activities. If they are delayed or are not carried out, the programme will be delayed unless the Lead Sustainability Coordinator and their team adjust the programme or revise the end date. The point is that CPA is an excellent way to manage the delivery of the process.

FIGURE 2. Schedule 1 sustainability reporting timeline (using critical path analysis).

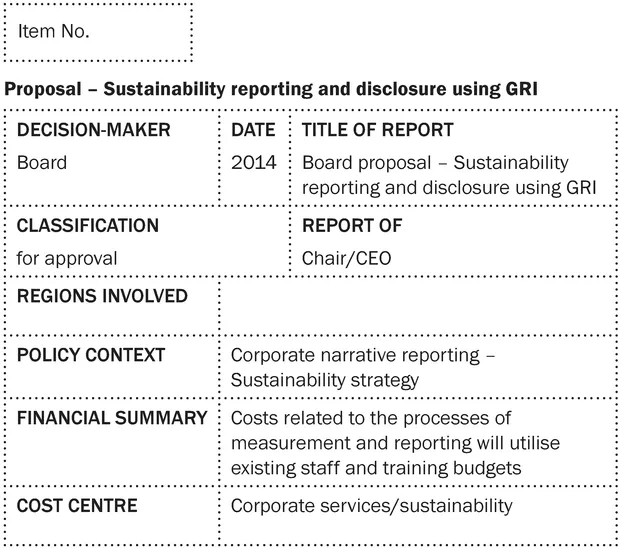

Template 1. Board report business case for sustainability reporting

1. Summary

Summarise how the proposal to report meets with strategic corporate objectives, values and policies. State any legislation and regulation that would be complied with. State any standards that would be complied with and any distinctions that may be obtained. State the final recommendation of the report that follows the summary.

Reporting embeds and communicates sustainable practice, through measurement, transparency and disclosure.

2. Recommendations

Recommendation to state outcome and include resources, cost and time where appropriate.

3. Previous policy/recommendations

Outline any past related approvals or failed requests as appropriate.

4. Background information

Articulate the internal and external sustainability context in relation to the organisation. It should provide an overview of the sustainability reporting framework proposed. This might include some detail on legislation, regulation, relevant recent sector reports, peer views and that of professionals and what is considered best practice. It may also include the leadership position of the most senior decision-makers. This section might also outline any anticipated successes and benefits including changed culture implications, reduced impacts, net positive expectations.

5. Proposal

State where the organisation is as regards sustainability and environmental social governance, and where it could be and why. Discuss how it will get to where it is going. It is helpful to position the government/s’ stock exchanges’ and regulators’ position for managing sector change and transition if applicable in this section.

The proposal should discuss common, comparable, consistent and rankable standards and perhaps articulate argument on the most appropriate standard considering any suitable alternatives available.

Discuss any areas of sustainability the organisation is already involved in. Cover any size issues, supply chain issues, impact is...