Spending on M&A has, in aggregate, grown so fast that it has even overtaken capital expenditure on increasing and maintaining physical assets. Yet McKinsey, the leading management consultancy, reports that "Anyone who has researched merger success rates knows that roughly 70% fail". The idea that businesses might be using huge and increasing sums of shareholders' money for an activity that more often than not leads to failure calls into question the information on which M&A decisions are based.

This book presents statistical studies, case material, and standard-setters' opinions on company accounting before, during, and after M&A. It documents the manipulation of annual accounts by acquirers ahead of share for share bids, biased forecasts of post-merger earnings by bidders, and devices to flatter earnings when recording the deal. It explores the challenges for standard-setters in regulating information flows during and after M&A, and for account-users wishing to learn from financial statements how a deal has affected performance.

Drawing on a wide range of international examples, this readable book is targeted not just at accounting specialists but at anyone who is comfortable reading the serious financial press, is intrigued by what is going on in the massive M&A market, and is concerned with achieving better-informed M&A. As such it might be of particular interest to business executives, lawyers, bankers, and investors involved in M&A as well as graduate students interested in researching or learning about the role of accounting in M&A.

In the accounts of many Western businesses spending on M&A has grown to exceed even that on new fixed assets. Much of Asia is following the same trend.

The disappointing return on much M&A expenditure calls into question the (accounting) information on which the M&A decisions are based.

The last 25 years have seen revolution and counter-revolution in the rules governing accounting for M&A. The resulting changes in mandated procedures can yield vastly different numbers for the acquirer’s earnings and its equity.

The accounting standards currently in place for reporting listed companies’ M&A and its aftermath are not those deemed preferable by the UK regulators ASB or – before they were thwarted by corporate lobbyists – by the US regulators FASB. And they have subsequently been challenged by standard-setters and academics.

Accountants have been accused of issuing misleading information to inflate the bidder’s share price artificially and distort M&A decisions: managing the bidder’s pre-merger earnings upwards, and providing upwardly biased earnings forecasts.

Accountants have been accused of recording the integration of M&A deals in misleading ways – creating “cookie jars” from which illusory profits can be drawn in years following M&A; perpetuating anomalous treatments of intangibles in M&A; and misleadingly manipulating post acquisition write-offs.

Notwithstanding the flaws in accounting around M&A, some important economic questions about the effect of M&A on company performance can best – or sometimes only – be answered with accounting data (suitably constructed to avoid the many potential pitfalls).

In more detail:

In the accounts of many Western businesses spending on M&A has grown to exceed even that on new fixed assets. Much of Asia is following the same trend.

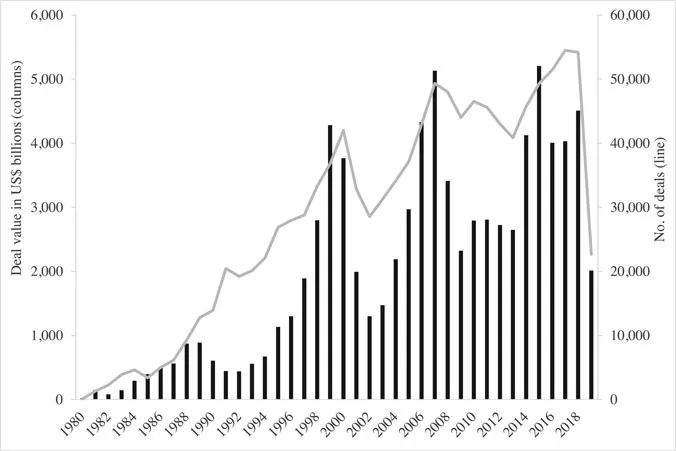

Mauboussin and Callahan (2014, 2015) show that for many businesses in the West spending on M&A has even overtaken CAPEX (buying, maintaining, or improving fixed assets such as land, buildings, or machines), and it is catching up in the East (see Chapter 2). Figure 1.1 charts the development of global M&A volumes and the number of transactions from 1980 to the first half of 2019. Annual M&A transaction values have first exceeded US $4 trillion in 1999 and then again in 2006–07 and have remained above that level in every year from 2014–18. And there have been no less than 40,000 M&A transactions annually since 2006. Seen from the target’s perspective, Meeks and Whittington (2019) report that no less than 83% of the companies listed on UK stock exchanges in 1948 had been acquired by 2018. As of writing of this book this trend seems to continue vigorously – in one extreme example, Refinitv, having been the re-branded data business of Thomson Reuters, was acquired in a leveraged buyout by Blackstone in 2018, less than a year later sold to London Stock Exchange in August 2019, which itself a month later became the target of a takeover offer by Hong Kong Stock Exchange. 2019 also has witnessed the continuation of several so-called mega mergers (e.g., the $54bn merger of Occidental and Anadarko, the $70bn acquisition of Saudi Basic Industries by Saudi Aramco, AbbVie’s $86bn bid for Allergan, the $89bn merger of United Technologies and Raytheon, and the $90bn Bristol-Myers Squibb offer for Celgene).

Figure 1.1 Global M&A volume (in US$ billion) and number of transactions (1980–2019*)

Note: *as of first half of 2019

Source: Refinitiv Eikon

The disappointing return on much M&A expenditure calls into question the (accounting) information on which the M&A decisions are based.

This evidence of disappointing returns has come from a variety of academic disciplines and practitioner sources. For example, in the academic finance literature Moeller, Schlingemann and Stulz (2005) analysed stock price movements and found that in their sample: “Acquiring firm shareholders lost 12 cents… for every dollar spent on acquisitions”. This general conclusion of wealth loss was echoed in the academic strategy literature by Cuypers, Cuypers and Martin (2017). The long-run stock price performance of acquirers post completion presented in Figure 1.2 shows that among 4,450 US acquisitions with a deal value exceeding $100 million completed between 2002–17 the acquiring companies on average performed significantly worse than their non-acquiring peers over the subsequent 12–24-month period post completion. Acquisition announced late in the economic cycle (and completed during recessions) perform particularly badly, but it seems that acquisitions in more recent years have performed slightly less badly overall.1 An earlier study in the industrial economics literature by Ravenscraft and Scherer (1987) of post-merger accounts found that “the estimated annual efficiency losses [attributed to US mergers] are in the range of 0.59 to 0.81 percent of current-dollar gross national product”. Part 3 analyses post-merger accounts for company samples from the US, UK, and China. Consultants McKinsey (2010) report that “Anyone who has researched merger success rates knows that roughly 70% fail”. Part 3 reports at length on post M&A performance. The shareholder-principals were often disappointed by the stewardship of their executive-agents’ performance after M&A, therefore, and concerns about governance/stewardship/accountability have been heightened by the findings of Harford and Li (2007) that “even in mergers where bidding shareholders are worse off [as a result of an acquisition], bidding CEOs are better off three-quarters of the time”. Stewardship issues are discussed in Chapters 4 and 5.

Figure 1.2 Average buy-and-hold abnormal returns (BHAR) of US acquirers in 4,450 acquisitions completed between 2002 and 2017

Note: Only acquisitions with deal values of more than $100 million by a US listed acquirer are included. Abnormal returns are calculated as the acquirer’s stock return minus the return on a size and book-to-market matched portfolio of non-acquirers rebalanced monthly and compounded over the 12 and 24 months post-completion. The sample of acquisitions has been obtained from Refinitiv Eikon, and stock returns and accounting variables are from CRSP and Compustat.

The last 25 years have seen revolution and counter-revolution in the rules governing accounting for M&A. The resulting changes in mandated procedures can yield vastly different numbers for the acquirer’s earnings and its equity.

In the US and UK over the last 25 years, acquiring firms have been variously encouraged, allowed, and forbidden by the standard-setters to leave out of their balance sheet the goodwill purchased in M&A, the excess they paid for a target over its book value.2 Accountants have struggled with the question whether/how any subsequent depletion of purchased goodwill should be reported. When they have included purchased goodwill in the balance sheet, acquirers have variously been required, allowed, or forbidden by the standard-setters to record in the income statement its depletion in value by means of a regular annual amortisation charge3 analogous with the depreciation of tangible fixed assets.

These changes in accounting rules can lead to drastically different bottom lines in the acquirer’s profit and loss account (profit) and balance sheet (equity). Chapter 2 simulates the effects of the different (recently mandated) accounting regimes in relation to Vodafone’s acquisition of Mannesmann in 2000. Vodafone paid £101 billion for Mannesmann’s assets (book value of target’s separable assets £18 billion, purchased goodwill £83 billion). In one of the years after the acquisition, the level of Vodafone’s reported equity in one of the simulated accounting regimes is only half that in an alternative regime. In one regime-year, the change in equity is plus £9 billion in one regime but minus £56 billion in another. For six post-acquisition years together, earnings are close to break-even for one regime, negative £56 billion for another, and negative £71 billion for the other two.

The accounting standards currently in place for reporting M&A and its aftermath are not those deemed superior by the UK regulators ASB or – before they were thwarted by corporate lobbyists – by the US regulators FASB. And they have subsequently been challenged by standard-setters and academics.

By the late 1990s, the UK standard-setter, ASB, had moved to a regime whereby goodwill purchased in the course of M&A was all recognised (included) in the balance sheet and then normally amortised through the profit and loss account with amortisation, occasionally supplemented by impairment (write-offs) (see Chapter 3). The American standard-setter, FASB, proposed a similar regime. The resulting US debate spilled over into national politics. The business lobby operated through Congress to challenge the standards being proposed for M&A accounting by FASB (Beresford, 2001; Zeff, 2002). A senior executive of Cisco Systems argued before a Senate hearing that changes to M&A accounting proposed by FASB would “stifle technology development, impede capital formation and slow job creation”.4 The proposal that attracted most hostility was for compulsory amortisation of purchased goodwill, to hold executives to account year by year in the income statement for the shareholders’ money they had spent on acquisitions. In the end, the business lobbying prevailed: amortisation was rejected. International standard-setters subsequently adopted the US settlement for listed companies, and UK arrangements were brought into line with that alternative regime.

Chapter 5 reviews the rationales presented by academics and practitioners for the alternative systems and offers econometric analysis of their impact. Chapter 4 reports the perspectives on these alternatives of two eminent international standard-setters, including their reservations about the present arrangements.

Accountants have been accused of issuing misleading information to inflate the bidder’s share price artificially and distort M&A decisions: managing the bidder’s pre-merger earnings upwards and providing upwardly biased earnings forecasts.

It has been argu...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Contents

Abstracts

List of figures

List of tables

List of contributors

Preface

Acknowledgments

List of abbreviations

1 Introduction

PART I Accounting procedures

PART II Managing perceptions of performance around M&A

PART III Using accounts to measure the impact of M&A on performance

PART IV Concluding remarks

Author index

Companies/corporations (short form name) index

Subject index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Accounting for M&A by Amir Amel-Zadeh, Geoff Meeks, Amir Amel-Zadeh,Geoff Meeks, Geoff Meeks, Amir Amel-Zadeh in PDF and/or ePUB format, as well as other popular books in Business & Accounting Standards. We have over 1.5 million books available in our catalogue for you to explore.