The Political Economy of Pension Financialisation addresses – for numerous countries – how and why pension reforms have come to rely more on financial markets, how public policy reacted to financial crises, and regulatory variation.

The book demonstrates how the process of pension financialisation reveals that pension policy is not only a social policy that affects retirement income, but also a financial policy that impacts savings rates, corporate finance and the economy. The chapters shed light on pre-funded private pensions as one key component of financialisation, as they turn savings into investments via financial services providers. Readers will also see how pension financialisation and the broader financialisation of the economy are here to stay, despite negative developments during and after the financial crisis.

A systematic and comparative overwiew of the financialisation of pensions, The Political Economy of Pension Financialisation is ideal for scholars and postgradues working on Political Economy, Public Policy and Finance. This book was originally published as a special issue of the Journal of European Public Policy.

The political economy of pension financialisation: public policy responses to the crisis

Anke Hassel, Marek Naczyk and Tobias Wiß

ABSTRACT Financialisation has become a key feature of post-industrial economies. This special issue sheds light on pre-funded private pensions as one key component of financialisation, as they turn savings into investment via financial services providers. Public pension systems face financial pressures, resulting from ageing and rising public debt, while financial services are keen to move into the market of private pension provision. Pre-funded private pensions are shaped by regulatory policies that create and correct markets. The financial crisis has triggered policy responses including shifts in investment strategies and also a re-assessment of the role of pre-funded private pensions as a complementary, rather than a superior, source of old-age income. Policymakers’ growing awareness of the benefits of collective occupational schemes administered by the social partners may pave the way for a greater role for collective schemes.

Introduction

Pension systems play a crucial role in the evolution of post-industrial economies. Pension policy is not only a social policy that affects retirement income, but also a financial one that impacts savings rates, corporate finance and, indirectly, corporate behaviour.

Funded pensions ‘can be designed to create large sums of patient, far-sighted capital, thereby giving rise to a distinctive type of capitalism.’ (Estevez-Abe 2001: 190). In Japan, pension funds helped not only to provide funding for public infrastructure projects, but also to supply private manufacturers with patient capital that helped Japanese firms to develop capacities that propelled them to world levels from the 1960s. However the relationship between pension systems and types of capitalism has changed fundamentally in recent decades, as a wave of financialisation has swept the globe (van der Zwan 2014). The lifting of capital controls, the steep increase in profits from financial activities, the rise of shareholder value – a doctrine that has sometimes been pushed by pension funds – have all characterised the shift from industrial to finance capitalism. At the same time, public pensions have been targeted for partial privatisation, thereby opening up new business opportunities for financial firms, such as insurance companies, mutual funds and banks.

Historically, old-age pensions were understood as a deferred wage, both by trade unions and employers, and were at the core of welfare state expansion. As pension systems make long-term promises for payments in old age, individuals and families rely on them when making life choices. But population ageing, declining growth rates, rising public debt as well as the decreasing participation rates of elderly workers have put pressure on mature pension systems and have made pension reform a salient issue in political discourse. Despite numerous reforms that have lowered pension benefits and increased the retirement age, public pensions still amount to 8.2% of gross domestic product (GDP) and stood at 18% of total government spending in the OECD in 2013 (OECD 2017: 142).

In line with the World Bank’s multi-pillar model (Orenstein 2013; World Bank 1994), reforms in recent decades included ‘twin processes’: the – typically incremental – reduction of public pensions and the expansion of non-state – occupational and personal – pre-funded defined-contribution pensions. This led to a privatisation and marketisation (Ebbinghaus 2015), and ultimately to a financialisation of pensions. Privatisation shifted responsibility for pension provision to private actors, mainly financial services firms, employers and trade unions. Marketisation introduced market mechanisms into both public and private pension plans. Indeed, in both types of plans, clear commitments to guarantee pensions in relation to previous wages at retirement (so-called ‘defined benefits’) have been increasingly replaced by the ‘defined-contribution’ principle that consists of offering the insured what they have paid into the system, plus – financial or notional – returns on these contributions, thereby fostering a major reallocation of retirement risks onto individuals.

Pension financialisation lies at the intersection of the privatisation and marketisation of pensions. It refers to the rise of pre-funded defined-contribution plans managed by private financial services providers and to its implications in terms of the growing share of the financial services sector in GDP and employment growth, the growing dependence of pensioners’ livelihoods on the performance of financial markets and the growing role of pension funds as providers of capital. Pension financialisation is therefore a subcategory of the broader – and multidimensional – phenomenon of financialisation (cf. van der Zwan 2014; see also Dixon and Sorsa 2009; Ebbinghaus 2011; Engelen 2003; Hacker 2006; Langley 2008).

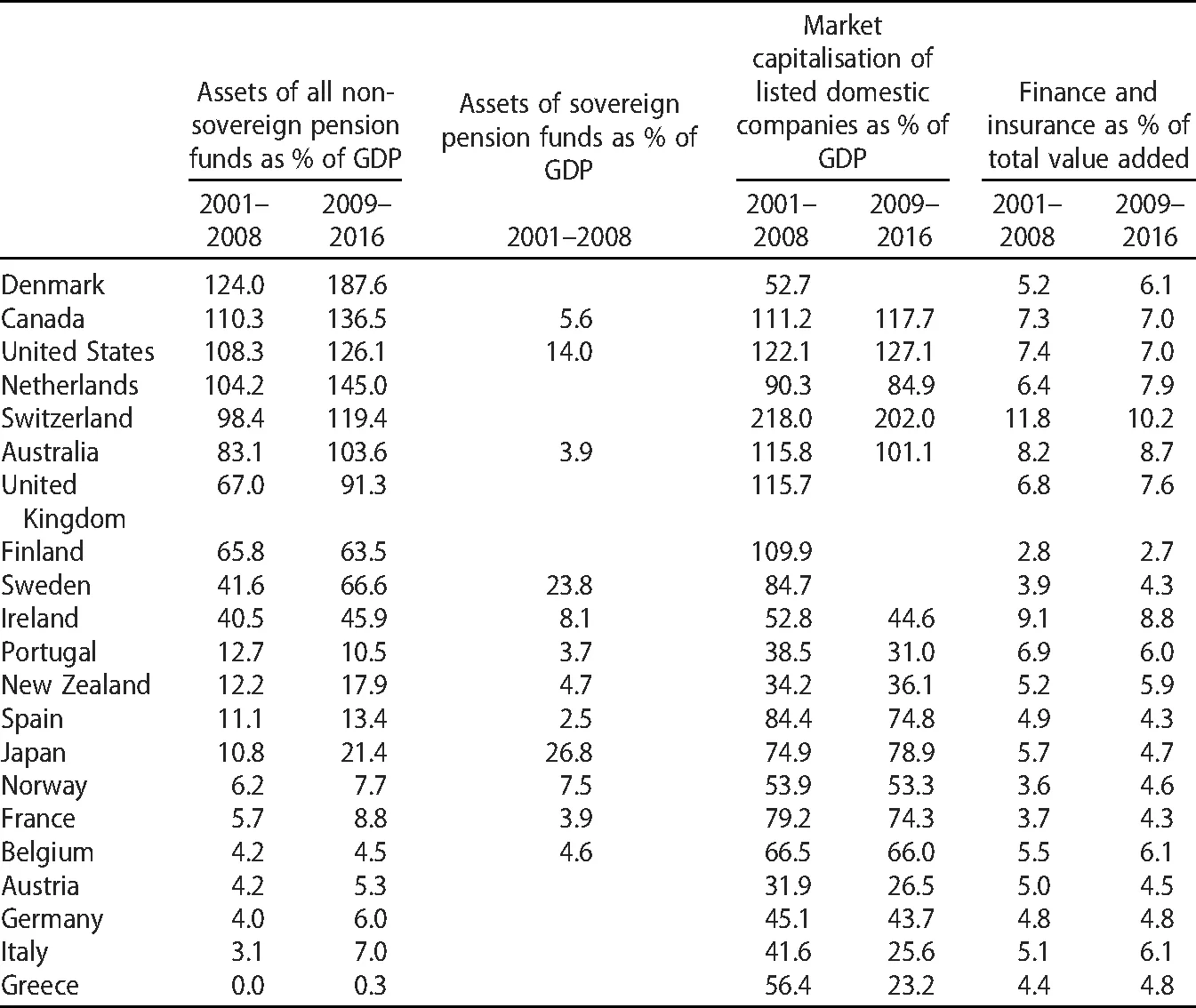

Despite a general trend towards the financialisation of pensions, three phenomena are striking: First, the extent to which pre-funded private defined-contribution pension plans play a role in mature welfare states still varies considerably. There has been no universal shift of pension systems towards comprehensive private provision. The size of assets held by pension funds – of the defined-contribution and defined-benefit type – in the OECD ranges from close to zero to more than 150% of GDP (Table 1).

Second, there is an important variation in the governance structures and distributional consequences of national systems of pre-funded private pension provision. For example, while some countries (i.e., the United States and the United Kingdom) have ‘pure’ defined-contribution plans, that fully expose individuals to investment risk, others (e.g., France and Germany) introduced regulations – such as minimum return guarantees – that aim to protect savers from stock market drops (Antolín et al. 2011). Risks do thus not have to be fully attributed to savers.

Third, the financial crisis has had an impact on the provision of pre-funded private – particularly defined-contribution – pensions. Although there has been no general reversal of pension financialisation, regulators, policymakers and pension funds themselves have started to address the negative fall-out of the crisis on pension accounts. One sees a mixed account: in some countries, there was a gradual adjustment towards more conservative investment (UK), but in other cases, asset allocation became even more risky, searching for yields in a low interest rate environment. On the other hand, there was more risk-sharing through collective schemes, while the pressure to join private defined-contribution schemes continued through auto-enrolment. Highly professional financial services industries have been more or less successful in influencing the most recent reforms.

Table 1. Pension funds and financialisation in 21 OECD countries.

Source: OECD Global Pension Statistics; World Development Indicators; OECD.Stat.

In this collection of articles, we shed light on the evolution of national pensions-finance nexuses – and the variation in pension financialisation – by analysing their emergence, regulation and readjustments. The focus of the analysis is on the response of policymakers to the financial crisis and the fall-out for private pensions. Pension financialisation presents sharp distributional and political dilemmas (Anderson 2019). Individualised financial market risks may increase inequality for pensioners and retirees face ‘cohort risk’ as falling financial asset prices at the time of retirement hit particular cohorts. Furthermore pension financialisation increases the political influence of financial actors.

Because of the rise of these new risks, we are interested in how different governance arrangements have managed to control them in times of financial crisis, and how policymakers have dealt with different kinds of demands from the insured and from other stakeholders, such as employers and financial services industries. This article first surveys the extent of financialisation of pension policy and its impact on the financialisation of the economy. It then looks more closely at the impact of the financial crisis on private pension provision and policy responses, and presents the articles featured in this special issue. It concludes by zooming in on critical future issues in the governance of multi-pillar pension systems.

Pension financialisation today: no convergence among OECD countries

The financialisation of advanced economies has recently attracted a lot of attention in the context of the public debate on the effects of the financial crisis and growing income inequality. Financialisation is a multidimensional concept that captures a variety of – largely interlinked – developments (van der Zwan 2014: 101–2).

One dimension that has characterised financialisation has been the growing share of the financial services industry in GDP and in employment growth (Boyer 2000). A second facet of financialisation has been the increasing reliance of non-financial firms on earnings generated through financial channels rather than through trade or commodity production and, relatedly, firms’ adoption of the doctrine of shareholder value maximisation (Krippner 2005; Lazonick and O’Sullivan 2000). A third very significant development has been the financialisation of households’ everyday lives through their increasing use of various financial products, such as private defined-contribution pensions (Martin 2002).

A debate exists about how social policies have been affected by – or might also affect – these developments. The Varieties of Capitalism (VoC) approach has, for a long time, assumed that the deregulation of financial markets and the rise of institutional investors – such as private pension funds – pushing for shareholder value maximisation posed the greatest threat for the resilience of coordinated market economies and their encompassing welfare states (Hall and Soskice 2001). Others have argued that the financialisation of everyday life resulting from the promotion of homeownership – for example because of mortgage holders’ attentiveness to interest rate changes or because of the wealth effects of house price appreciation – has eroded public support for redistribution and social insurance arrangements (Ansell 2014; Langley 2008; Schelkle 2012a; Schwartz and Seabrooke 2008). Social policy changes have also been seen as a major driver of financialisation: For example, welfare state retrenchment and its negative impact on the living standards of low and middle-income households is said to have contributed to a boom in consumer credit (Crouch 2009; Krippner 2011).

Old-age pensions have been considered a central constituent of financialisation processes, since they can be pre-funded through an accumulation of assets invested in capital markets (Engelen 2003). The rise of defined-contribution pensions – and the direct link such plans create between the level of benefits and financial market fluctuations – has contributed to turning households into ‘everyday’ investors (Langley 2008). Pension funds have pushed for a better protection of minority shareholder interests – and, sometimes, for a greater integration of shareholder value maximisation – in investee firms’ management practices (Gourevitch and Shinn 2005). Governments have also been increasingly attracted to pension privatisation because, in a context of deindustrialisation and, simultaneously, of the growing internationalisation of finance, they have seen it as a means to increase the competitiveness of their domestic financial industries and, therefore, to boost their countries’ economic growth (Naczyk and Palier 2014; see also, World Bank 1994).

While there has been a clear trend towards financialisation in pension policy in recent decades, reforms have not led to convergence among OECD countries. National pension systems have never relied on prefunded private pension provision to the same extent, neither before nor after the era of the retrenchment of public pensions. Moreover, countries’ different regulatory approaches have meant that private pension funds are not associated to the same extent with financial sector growth and with a financialisation of non-financial firms. Differences in the regulation of pension funds are responsible for varying degrees of individual financial risks or, in other words, a financialisation of daily life.

It has generally been accepted in the literature that generous public pension schemes are likely to ‘crowd out’ private pension provisions and that, consequently, the retrenchment of public pensions could help ‘crowd in’ private plans (Davis 1995; Ebbinghaus 2011). At the same time, it has long been argued that pension systems are a ‘locus classicus’ of path dependence, for example because of the very long periods of time over which workers accrue their pension rights and of the political resistance to any attempts to change the economic expectations that workers form over time (Myles and Pierson 2001: 306). Even though almost all affluent democracies have cut public pension entitlements over the last three decades (Ebbinghaus 2011), public expenditure on pensions has continued to increase across most OECD countries (see Figure 1). This is the result of financial pressures caused by population ageing, but also of long time lags between the enactment of pension cuts and their implementation (Bonoli and Palier 2007). Similarly, cross-national variation in current spending on private pensions and in the size of pension fund sectors is still, to a large extent, the legacy of regulations introduced several decades ago.

During the post-war period, most countries in Western and Southern Europe introduced generous earnings-related social insurance schemes that provided workers with income maintenance and largely crowded out pre-funded private pension plans (see top spenders on public benefits in Figure 1). Two notable exceptions in Continental Europe were Switzerland and the Netherlands, where much more basic social insurance pensions (in Switzerland) and universal flat-rate pensions (in the Netherlands) opened enough space for the development of private pension plans. Because of their reliance on basic – often flat-rate – public pensions, the English-speaking countries of Europe, North America and the Antipodes also saw the rise of what some have called ‘pension fund capitalism’ (Clark 2000). Nordic countries relied on somewhat more complex mixes of public and private arrangements. All of them introduced universal flat-rate pensions for their citizens between the 1930s and 1960s. In the 1960s, Sweden, Finland and Norway – but not Denmark – topped these schemes up w...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Table of Contents

Citation Information

Notes on Contributors

1 The political economy of pension financialisation: public policy responses to the crisis

2 Reinforcement of pension financialisation as a response to financial crises in Germany, the Netherlands and the United Kingdom

3 Multipillarisation remodelled: the role of interest organizations in British and German pension reforms

4 Re-assessing the role of financial professionals in pension fund investment strategies

5 Countering financial interests for social purposes: what drives state intervention in pension markets in the context of financialisation?

6 Insuring individuals … and politicians: financial services providers, stock market risk and the politics of private pension guarantees in Germany

7 EU Pension policy and financialisation: purpose without power?

8 Financialisation meets collectivisation: occupational pensions in Denmark, the Netherlands and Sweden

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Political Economy of Pension Financialisation by Anke Hassel, Tobias Wiß, Anke Hassel,Tobias Wiß in PDF and/or ePUB format, as well as other popular books in Law & Labour & Employment Law. We have over 1.5 million books available in our catalogue for you to explore.