Financial Modelling in Commodity Markets provides a basic and self-contained introduction to the ideas underpinning financial modelling of products in commodity markets.

The book offers a concise and operational vision of the main models used to represent, assess and simulate real assets and financial positions related to the commodity markets. It discusses statistical and mathematical tools important for estimating, implementing and calibrating quantitative models used for pricing and trading commodity-linked products and for managing basic and complex portfolio risks.

Key features:

Provides a step-by-step guide to the construction of pricing models, and for the applications of such models for the analysis of real data

Written for scholars from a wide range of scientific fields, including economics and finance, mathematics, engineering and statistics, as well as for practitioners

Illustrates some important pricing models using real data sets that will be commonly used in financial markets

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

A forward contracts is a bilateral agreement to purchase or sell a certain amount of a commodity on a fixed future date at a predetermined contract price. The fixed future date is the delivery date of the commodity, and the predetermined contract price is the forward price. Thus, the participants of a forward contract on a commodity lock in a price today for future delivery. In Figure 1.1 we show the role of forward contract participants. The main characteristics of forward contracts are:

They are over-the-counter (OTC) trades, executed through brokers.

There are no cash flows until delivery.

On delivery date the seller of the contract has the obligation to deliver the commodity in return for the forward price.

A forward contract involves credit risk, where one of the counterparties does not, or cannot, fulfil his obligation to deliver or pay the commodity.

A forward contract can be mainly used for:

hedging the obligation to deliver or purchase a commodity at a future date;

guaranteeing a sales profit from a commodity production;

speculating on rising or falling commodity prices in case there is no liquid futures market.

FIGURE 1.1 Forward contract participants

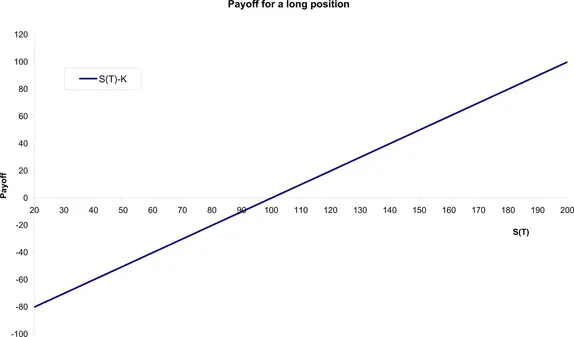

Consider a customer who is long on forward contract for delivery date T at contract price K. The payoff at time T is given by the difference between the actual price S(T) of the underlying and the contract forward price K. It is illustrated in Figure 1.2.

FIGURE 1.2 The payoff at maturity of a forward contract

Let us assume that at an initial time 0 a customer sells a forward contract with delivery T and contract price K. The forward price will be F(0, T). We want to estimate the value of the contract, X(t), at a generic time t. In order to do this, at time t we sell another forward contract at the current market forward price F(t, T), so that the physical deliveries of both forward contracts in the portfolio cancel.

In fact, if we indicate with S(T) the market price of the underlying forward contract at delivery T, Table 1.1 illustrates the strategy payoff at every considered time.

TABLE 1.1: Forward contract strategy

t

T

Long Forward at time 0

X(t)

S(T) − K

Short Forward at time t

0

F(t, T) − S(T)

Cash Flow

X(t)

F(t, T) − K

In order to avoid arbitrage possibilities, the fair value of a forward contract X(t) is uniquely given by

where r is the effective risk-free interest rate.

Example 1Example of Fair Value.

An electricity producer buys 10,000t coal to be delivered at time T at a price K = 50 USD/t. At time t, the forward price for coal to be delivered at time T is F(t, T)...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Dedication

Contents

Preface

Introduction

1. Commodity-linked Products

2. Spot Price Modelling

3. Forward Price Modelling

4. Derivative Valuation

5. Applications

6. Essential Statistics and Data Analysis

Bibliography

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Financial Modelling in Commodity Markets by Viviana Fanelli in PDF and/or ePUB format, as well as other popular books in Business & Commodities. We have over 1.5 million books available in our catalogue for you to explore.