![]()

one

Introduction to the Accounting for Sustainability Case Studies

Anthony Hopwood, Jeffrey Unerman and Jessica Fries

We can find our way to a new form of growth which is energy secure, cleaner, quieter, safer and more bio-diverse. And the transition to this form of growth over the next few decades will probably be the most dynamic and innovative in our economic history. It will be something like electricity or railways in earlier periods, or the rise of information technology more recently, but probably still more dynamic and on a larger scale than these radical economic transformations. Put another way, high-carbon growth would kill itself, first from very high prices of hydrocarbons and secondly and more fundamentally from the hostile physical environment it creates. On the other hand, low-carbon growth presents a very attractive and prosperous future. Pessimism and cynicism will be self-fulfilling; we must find a way. (Stern, 2009, p4)

Operating in an environmentally, socially and economically sustainable manner is one of the most urgent challenges facing organizations today. Issues such as climate change, the overconsumption of finite natural resources and the rapidly increasing destruction of the Earth’s ecosystems will drive fundamental shifts in society and the economy. It is increasingly important for organizations to understand and respond both to the manner in which these issues will affect their own continuity and long-term success, and to how they can help society as a whole in meeting the challenges faced. Accounting processes and practices have a key role to play in helping organizations develop the more sustainable operations that are a necessary part of this response. Such practices enable the systematic identification and interlinking of the economic, social and environmental costs and benefits of organizational strategies and actions. Accounting can also either help, or potentially hinder, the embedding of these considerations into organizations’ decision-making processes. To fulfil its potential in these important roles, accounting practice needs to develop from its traditional focus on the economic to also encompass the social and environmental dimensions of organizational strategies and actions.

As part of a long-standing commitment to sustainable development, His Royal Highness The Prince of Wales has underlined that economic development and human prosperity are reliant on, and fundamentally connected to, the continued health of the Earth’s ecosystems. Through the creation of The Prince’s Accounting for Sustainability Project (A4S) in 2004, he recognized the key role that accounting can play in ensuring that economic development is sustainable – that it is not achieved at the cost of long-term severe degradation to the environment and/or to social structures and cohesion which, if unchecked, will undermine economic progress. At the launch of A4S, The Prince of Wales emphasized the urgent need to develop appropriate sustainability accounting processes and practices. He stated that such accounting developments were needed ‘to help ensure that we are not battling to meet 21st century challenges with, at best, 20th century decision-making and reporting systems’.

A4S addresses these issues by recognizing the importance of integrating sustainability information into mainstream financial and management processes. This leads to more effective business management by more systematically connecting sustainability considerations to management decision-making and organizational action.

The main proposals from the project, which were based on work with over 200 companies, government agencies and other organizations, are explained in Chapter 2 of this book. These recommendations reflect steps to:

- embed sustainability considerations within organizations’ strategic and operational decision-making, processes and practices; and

- report all aspects of organizational performance in a connected, concise and consistent manner, reflecting the organization’s strategy and the way in which it is managed.

The aim of this book is, through a series of in-depth case studies, to document and probe the ways in which private- and public-sector organizations can apply the guidance developed by A4S and use these principles to embed sustainability into day-to-day decision-making and reporting.

The book also seeks to test and further develop the proposition underlying A4S’s work – namely, that a broad and inclusive concept of sustainability can be, and needs to be, integrated into mainstream financial processes. Through the case studies, it seeks both to further develop the tools that can support this integration and to disseminate and share best practice in this area. It does this by analysing the impact of methodologies and tools for integrated or connected sustainability reporting and decision-making on the case study organizations’ sustainability performance and on their strategic and operational decision-making.

Six leading companies (Aviva, BT, EDF Energy, HSBC, Novo Nordisk and Sainsbury’s) and two UK public-sector bodies (the Environment Agency and West Sussex County Council) have taken part in the case study project, the results from which are reported in this book. The case studies have been researched and written by a team of leading business and management academics from UK and continental European universities who have analysed the extent to which, and how, sustainability information has been embedded within the regular operations of the case study organizations. The case studies seek to support and enhance the work of A4S in moving sustainable decision-making into the mainstream of business practice.

To set the scene for the case studies that are presented in subsequent chapters, the following two sections of this chapter respectively deal with the relevance of sustainable development and climate change in today’s world, and with the role and significance of sustainability for organizations, including the business case for action. The subsequent section ‘Embedding sustainability considerations into business practice through accounting for sustainability’ then outlines the potential role of accounting processes and practices in fostering sustainable development. It also discusses how to embed considerations of sustainability – in the three connected spheres of economy, society and environment – into strategic and operational decision-making and action within organizations. The final section of the chapter ‘Summary of the case studies’ highlights the key findings from each of the case studies. These findings emphasize how accounting for sustainability processes and practices can be used to help embed sustainability within strategic decision-making and action, thereby addressing the challenges posed by, and realizing the opportunities inherent in, the sustainability agenda.

Sustainability, Sustainable Development and Climate Change

A prerequisite for individuals and organizations being able to survive and thrive in the long term is a society that is economically, environmentally and socially sustainable. If we ignore the need for durable sustainability in these three key areas, then we risk placing potentially intolerable burdens on ourselves and on future generations. Each of these three areas is necessary because:

- Economic sustainability provides us with future income and resources.

- Environmental sustainability provides a stable ecosphere that supports and protects life, including the provision of food and water.

- Social sustainability provides well-functioning societies that protect and enhance quality of life and safeguard human rights.

Taking the above factors into account, the concept of sustainable development recognizes the vital social role of economic activity and development. But it also seeks to ensure that this economic development is undertaken in a manner that weighs and balances positive economic and social impacts against negative social and environmental ones, taking into account the long-term sustainability of that economic activity and development.

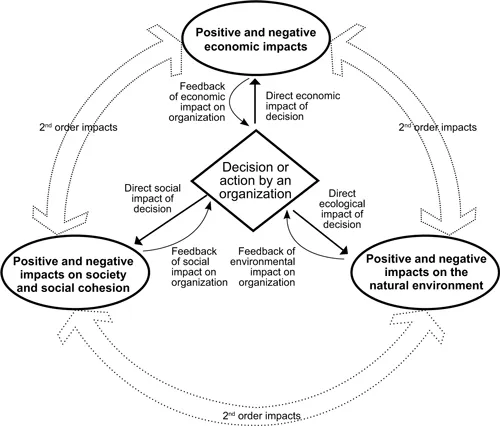

Figure 1.1 shows that these three spheres of sustainability are closely related, as it is increasingly recognized that actions and impacts in one sphere can and do affect sustainability in the other spheres. For example, since the start of the Industrial Revolution, economic development has involved the burning of large amounts of fossil fuels, which we have only relatively recently realized has contributed to environmental unsustainability through its impact on global warming. Conversely, economic deprivation through lack of economic development leads to numerous negative social impacts associated with poverty, including:

- hunger;

- inadequate housing;

- poor education;

- declining physical and psychological health (different aspects of which are associated with affluence); and

- increased human conflict, crime and violence.

Figure 1.1 Interconnectedness of organizational decisions on the three spheres of sustainability

Source: Jeffrey Unerman

Many of these negative social impacts reinforce poverty as they hinder the development of an adequate physical and intellectual infrastructure, which is needed to support economic development.

The Implications of Climate Change

Perhaps the most significant and urgent linkage between the three spheres of sustainability flows from environmental sustainability (or unsustainability) – in particular, climate change. The influential Stern Review (Stern, 2006) concluded that while the economic costs of reducing greenhouse gas emissions to environmentally sustainable levels would be high, the costs of dealing with the significant negative effects of global warming if emissions are not reduced to sustainable levels would be many times higher. Many of these costs would be imposed directly on business – for example, through higher costs of raw materials and energy, building obsolescence and damage to fixed assets through changing weather patterns, and changing patterns of consumer demand. Other costs would be imposed indirectly through the necessity of higher levels of taxation to fund increased government expenditure on mitigating the social and environmental consequences of global warming. Thus, in the long term, environmentally unsustainable business practices have the potential to significantly damage the financial sustainability of business. Climate change resulting from environmentally unsustainable practices will also produce significant negative social impacts for most of the world’s population (Meadows et al, 2004).

The reason that climate change poses such a significant threat to all three spheres of sustainability is the significant adverse impacts that forecast and probable levels of global warming are almost certain to have on essential matters, such as:

- food production;

- water supplies;

- rising sea levels, making coastal communities unviable;

- extreme weather events, such as storms, droughts, floods and heat waves; and

- the stability of many ecosystems upon which we rely (Stern, 2006).

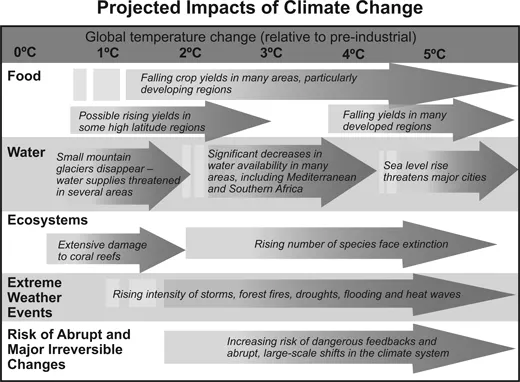

These impacts from global warming are predicted to increase in severity the greater that long-term average global temperatures rise above pre-industrial levels (see Figure 1.2). The overwhelming scientific consensus, accepted by the international community at intergovernmental level and recognized within the Copenhagen Accord and by more than 500 companies representing the international business community within the Copenhagen Communiqué, is that a rise of more than 2°C in average temperatures will lead to significantly negative and potentially irreversible environmental impacts. As these impacts will not be uniform throughout the world, they are also likely to lead to additional significant social disruption and conflict. Those people who will be worst affected will seek to move to regions that have been less affected, but which will nonetheless already be suffering negative impacts and stress from climate change. Dealing with these major consequences of environmental and social unsustainability will be very expensive, if not impossible, and will thus compromise economic sustainability. This will inevitably negatively impact on both businesses and public-sector organizations.

Figure 1.2 Impacts of global warming

Source: Stern Review on the Economics of Climate Change (2006), Crown Copyright

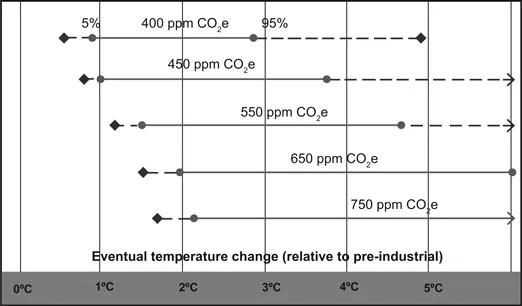

The concentration of greenhouse gases in the atmosphere is widely accepted as a key factor in determining average global temperatures, and these gases are currently rapidly becoming more concentrated. Indeed, they are fast approaching levels of concentration that have a very high risk of leading to irreversible negative climate change, as set out in Figure 1.3. This increasing concentration is due to annual greenhouse gas emissions from human activities – such as industry, transport and agriculture – far exceeding the Earth’s finite capacity to absorb and convert these gases. To reduce the significant risks to economic, social and environmental sustainability from climate change, it is therefore necessary to significantly reduce current levels of annual greenhouse gas emissions – of the order of an 80 per cent reduction on 1990 levels by 2050 within developed nations. Achieving this scale of change will require unprecedented technological advances, as well as fundamental changes in the global economic model. Actions to reduce emissions of greenhouse gases are therefore urgently required from all organizations if we are to better ensure a viable long-term natural environment in which companies can thrive economically. Furthermore, as Lord Stern (2009) eloquently argues, making the transition to a low-emissions society will present many economically attractive opportunities that will have the connected impact of enhancing economic, social and environmental sustainability.

Figure 1.3 Concentrations of carbon dioxide equivalent (CO2e) and associated predicted temperature rises

Source: Stern Review on the Economics of Climate Change (2006), Crown Copyright

The Role and Significance of Sustainability for Organizations

Drawing on the interconnected sustainability impacts discussed earlier in this chapter, the motivation for organizations to operate in a sustainable manner should be twofold. First, leaders of every organization need to recognize that they have ethical responsibilities to contribute to the creation of a sustainable society and not to harm others. Thus, they should seek to minimize the negative impacts on environmental and social sustainability from their operations and maximize the positive impacts. Second, in addition to this recognition that tackling their organization’s negative impact on environmental and social sustainability is a moral necessity, business leaders increasingly need to recognize that it is in the company’s own economic self-interest to operate in an environmentally and socially sustainable manner.

Acting Responsibly

In governmental policy on sustainable development, some governments (e.g. the UK) regard sustainability in the environmental and social spheres as key outcomes to be targeted by government policy, with a sustainable economy being one of three key enablers for social and environmental sustainability (the other two enablers being responsible use of scientific research and good governance). From this governmental policy perspective, social and environmental sustainability has a higher weighting and priority than economic development in decisions about balancing impacts across the three spheres of environmental, social and economic sustainable development.

However, at the individual organizational level, especially in the private sector, the balancing of impacts across the three spheres will be informed by slightly different considerations to those at governmental level. In weighing all of these impacts, it is important to identify not only the potential positive and negative impacts in each sphere, but also the significance, or materiality, of each impact, both to society and to the organization itself. This is a highly complex process, as every action taken by an individual, a business or a public-sector organization can have numerous and often conflicting impacts within each of the economic, environmental and social spheres, as well as between these spheres (as illustrated in Figure 1.1).

For example, the construction industry has many well-known negative environmental impacts. This is partially due to the high level of greenhouse gases emitted in manufacturing many building products, especially concrete, and in transporting and assembling these products for construction projects. But it is important to weigh many other factors against this negative environmental impact, including:

- social benefits from the ...