As change sweeps across the public sector, a huge range of accounting and financial management challenges are created. This textbook analyses the reforms that are being introduced to deal with these challenges and their global impact on the public sector.

Readers are provided with an international overview of government accounting, reporting, management control, cost accounting, budgeting and auditing. In explaining how innovative financial management tools are utilized in the public sector, the authors address a number of emerging issues:

Harmonization trends in public financial management and International Public Sector Accounting Standards (IPSASs)

Financial reporting and consolidated financial statements in the public sector

Public sector management accounting and control methods

Financial and performance auditing in the public sector

This concise and accessible textbook will be core reading for public sector accounting and financial management students and will also be required reading for students of public management and administration more generally. Managers, accountants, consultants and auditors working in the public sector will also find the book a useful reference.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

1 The conditions for and the users of public sector accounting

Torbjörn Tagesson

DOI: 10.4324/9781315848389-1

Learning objectives

To be aware of the specific conditions that apply to public sector accounting entities as a result of their legal and institutional prerequisites.

To have knowledge about potential and primary users of governmental financial reporting.

Key words

The accruals assumption

Externalities

Public goods

Stakeholder

1.1 Introduction

The emergence of accounting and bookkeeping is often associated with Fra Luca Pacioli and the emerging trade in Italy during the fifteenth century. However, the history of accounting dates back thousands of years. This is a fact that also applies to public sector accounting. Already Alexander the Great used accounting and bookkeeping in order to control and manage his client kings. The development of accounting goes hand in hand with social and economic development in society. In the same way as the separation of ownership and control had a major impact on the development of private sector accounting, public sector accounting has affected but has also been influenced by the development of democracy. According to the famous sociologist C. Wright Mills, ‘democracy implies that those who bear the consequences of decisions have enough knowledge – not to speak of power – to hold the decision-makers accountable’ (Mills, 1957: 325).

Although institutional, contextual and legal prerequisites vary among different sectors of society and between different countries, the starting point for accounting is basically the same. Accounting is about recording, recognizing, measuring and reporting economic events and transactions. Double-entry bookkeeping is the usual method used for recording accounting transactions such as purchase or sale, respectively, money received or paid. Recognizing is about determination of when revenues and costs are earned or incurred. This separation between recording and recognition is known as the accruals assumption.1 The accruals assumption requires that one can measure the value of economic events and transactions. This measurement problem is one of the most fundamental but also most difficult questions in accounting theory. An unequivocal answer cannot be given to this question, but one way to start is to discuss and determine/identify the users and their information needs. The users and their information needs are, of course, also crucial regarding form and content of the financial reporting that is based on the recording, recognition and measurement of economic events and transactions. Thus, based on the users and their information needs, one can deduce the purpose of financial reporting, taking into account the specific conditions that apply to the accounting entity as a result of its legal and institutional prerequisites.

1.2 Specific conditions for public sector entities

Before discussing the users and their information needs, we will highlight some of the most important aspects that characterize public sector entities. Although prerequisites may be partly different between different levels of public sector and different public sector entities, there are some unique characteristics that apply to the entire public sector and must be considered regarding its accounting and financial reporting.

Governmental organizations such as local and central government entities use common and public resources to provide public goods and services to citizens and users. According to Barton (1999), the existence of externalities and market failure form the basis for government provision of goods and services. By externalities, ‘we mean situations where consumption benefits are shared and cannot be limited to particular consumers, or where economic activity results in social costs which are not paid for by the producer or the consumer who causes them’ (Musgrave and Musgrave, 1988: 42). The first type of externality, i.e. the sharing of consumption benefits, means that the use of a service or facility by one consumer does not mean that others are excluded from using and taking advantage of the benefits provided. Hence, in situations when a good or service is required, but the free-rider problem makes it unprofitable for private operators to provide the product or service, we need the government to provide it. Barton refers to these goods and services as ‘pure public goods’. He exemplifies with citizens’ access to the system of law, order and defence, broadcasting, street lighting, roads, public parks and so on. The situation where production of goods and services results in social costs that are not paid for by the producer or the consumer who causes them, e.g. pollution of water and air, is an example of impure or mixed public goods with a negative externality. In these situations government can try to use regulation, e.g. ‘green taxes’, in order to realign the private and social costs, or they can choose to provide the good itself using a pricing structure that ensures the ability to recover some of the social costs (Barton, 1999). There are also situations where social benefits exceed private costs. Also in these situations government can choose to provide the service or goods themselves or to subsidize private provision of the good. Education and health services are such examples (Barton, 1999). In some cases governments also choose to regulate or provide private goods and services, when they are considered to be essential for the community. In rural areas this may include services relating to, for example, pharmacy, vehicle inspection, mail distribution and so on. However, in many cases it concerns natural monopolies in the infrastructure and utilities sector such as railway, water and sewage, gas distribution, waste management, etc. As pointed out by Barton (1999), many of these operations also involve significant externalities. Thus, in practice, it is not always easy to make a clear-cut distinction between private goods and public goods. What goods and services the governmental sector chooses to provide to its citizens vary between different countries and political systems.

The powers of government and range of government activities are ultimately matters of political choice which may take many factors into consideration in addition to narrowly-defined economic ones.

(Barton, 1999: 23)

Whether the services are provided by the public sector because they are unlikely to be provided by other entities or because it is not considered appropriate for them to be provided through competitive market mechanisms on public policy grounds, it means that government services and goods in many cases are provided in a non-competitive environment (e.g. IPSASB, 2011) by using production means that have the character of public utilities that are not saleable on an open market.

The primary objective of public sector organizations is not to make a profit or generate return on capital, but to meet different political policy objectives and provide goods and services to citizens. In some countries, like Sweden, it is even forbidden for public organizations without specific statutory regulation to engage in businesses for profit. The right to levy taxes secures the obligations and commitments of public sector organizations. Besides revenues from tax, public sector activities are also financed by fees and grants, which are not retrieved from a free market, but are guaranteed by political decisions and regulation.

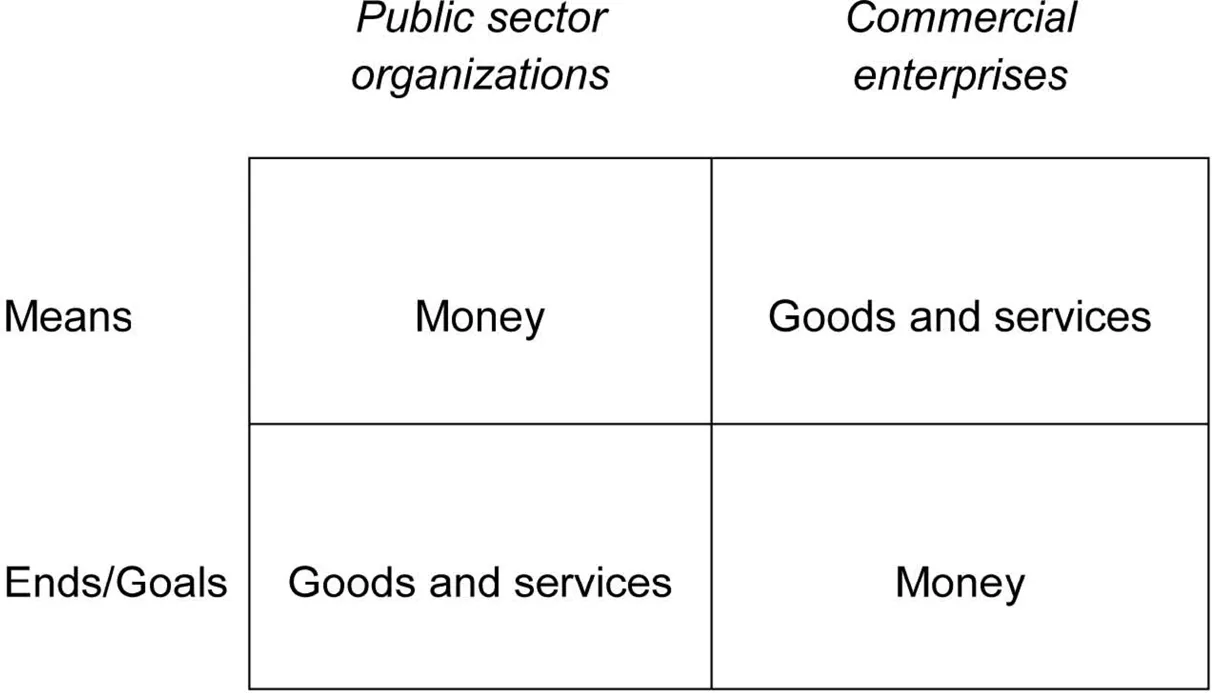

In relation to commercial enterprises, the structure in terms of means and ends are reversed to public sector organizations: while commercial enterprises run operations in order to generate resources and make a profit, public sector organizations receive resources in order to run operations and activities (see Figure 1.1).

Figure1.1 Ends and means in public and private sector organizations

Source: Rådet för kommunal redovisning, 2011: 12

Thus, in contrast to private sector entities, the capital and revenue of which must rely on exchange transactions that are entered into voluntarily by its stakeholders (e.g. IPSASB, 2011), public sector organizations have the character of mandatory associations, meaning that the relationship between the organization and its users is not always of a voluntary nature. Under public property rights, ownership cannot be concentrated or capitalized as in a limited company. One citizenship means one vote. This vote is personal and cannot be sold or purchased, at least not in a functioning democracy. This also means that there is no owner who can decide on dividends or withdrawals of capital. The meaning of equity is therefore different in the public sector compared to the private sector. There are no owners who are the residual risk takers; instead, it is the economic and political freedom of action of future taxpayers and citizens that is at stake.

Considering the fact that governmental entities have no explicit owners and thus no current or potential investors, the objective of financial reporting in public sector entities is not to provide investors with information useful for forward-looking economic decision making. In the public sector the more future-oriented information is communicated through the budget. In many jurisdictions the budget is statutory and has a special legal significance. It is usually the basis for setting taxation levels and is a part of the process of obtaining legislative approval for spending and resource allocation (IPSASB, 2011), and decisions on the budget are key elements in the political management of governments. Hence, it is through the budget that the politicians communicate and articulate ideologies and future-oriented information to external stakeholders. In the light of the budget’s significance and specific role, ex-post accounting provides important accountability information and serves as an important tool in following up and evaluating if the public sector entities have met the financial objectives that were defined and set in the budget. Thus, the link between budget and financial reporting provides conditions for voters and other stakeholders to obtain knowledge in order to hold politicians responsible and accountable for their decisions.

1.3 Users

An organization can have many different stakeholders and consequently a wide range of users or potential users of financial reporting. To produce financial reports tailored to each individual stakeholder would not be economically viable or even possible. Legislators and standard setters have the task of ensuring a minimum level and balance various stakeholders’ interests. Thus, financial reporting must meet the general and common information needs of potential external users who cannot demand reports tailored to meet their specific information needs. For public sector entities, this range of potential users can be wide – almost every person or company has some kind of relation or exchange with some public sector entity. Governments and public sector entities raise resources from taxpayers, subscribers, lenders and other public sector entities for their use of the provision of services and goods to citizens and other service recipients. In their consultation paper regarding the Conceptual Framework for General Purpose Financial Reports (GPFR) by Public Sector Entities (2008), the International Public Sector Accounting Standards Board (IPSASB) identifies three major groups of potential users:

Recipients of services or their representatives.

Providers of resources or their representatives.

Other parties, including special interest groups and their representatives.

The IPSASB particularly emphasizes that the legislature, which acts in the interests of members of the community, is a major user of GPFRs. Besides citizens, who both receive services from and provide resources to the public sector entities, there are a number of other potential users, for example subscribers, creditors, statisticians, the media, suppliers, other governmental entities and other organizations that rely on compensation or compete with governmental entities, etc. By providing a financial report of high quality, governmental entities can also satisfy some of the information needs of organizations and users that have the authority to require reports tailored to meet their own specific information needs – e.g. politicians, officials, auditors, regulators and oversight bodies, subcommittees of the legislature or other governing bodies. The wide range of potential users and the broad definition reflects the diversity and heterogeneity of the stakeholders. To accommodate all potential users would involve extensive and almost impenetrable accounting and reporting. Thus, in their exposure draft from 2010, Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities (phase 1), the IPSASB identifies citizens as primary users of GPFRs. Also this clarification and definition of prima...

Table of contents

Cover Page

Frontmatter Page

Half Title Page

Title Page

Copyright Page

Table of Contents

List of illustrations

List of contributors

Preface

Acknowledgements

List of abbreviations

1 The conditions for and the users of public sector accounting—TORBJÖRN TAGESSON

2 Accounting reforms, standard setting and compliance—TORBJÖRN TAGESSON

3 International Public Sector Accounting Standards (IPSAS)—JOHAN CHRISTIAENS AND SIMON NEYT

4 Consolidated financial statements in the public sector—GIUSEPPE GROSSI

5 Public sector management control tools—TJERK BUDDING

6 Public sector management accounting—TJERK BUDDING AND MARTIJN SCHOUTE

7 Public sector budgeting—TJERK BUDDING AND GIUSEPPE GROSSI

8 Financial audit in the public sector—FILIP CASSEL

9 Performance auditing in the public sector—PETER ÖHMAN

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Public Sector Accounting by Tjerk Budding, Giuseppe Grossi, Torbjörn Tagesson, Tjerk Budding,Giuseppe Grossi,Torbjörn Tagesson in PDF and/or ePUB format, as well as other popular books in Business & Accounting Standards. We have over 1.5 million books available in our catalogue for you to explore.