Introduction

Questions are rarely set solely upon the rules relating to the formation of companies. However, in tackling questions on the consequences of incorporation, some appreciation of the rules of formation (and the different types of company) is appropriate. Factors which might influence the decision to incorporate, the effects of incorporation and ‘lifting the veil’ are common areas for questions. Questions involving ‘lifting the veil’ generally require some form of critical analysis rather than a mere recitation of decisions. Another, broader type of question regularly encountered involves advice about incorporation and running of companies and possible types of investment in a company either in general or for specified persons (e.g. a brilliant, but non-business minded, inventor). Material relating to formation should also be incorporated in questions relating to the different legal regime applicable to public and private (particularly quasi-partnership) companies and general questions about disclosure.

The law relating to promoters and pre-incorporation contracts can be regarded as part of the formation of a company. Questions on promoters may be linked with the liability of directors and a question could combine a pre-incorporation contract with a post-incorporation contract. However, the increasing use of ‘off-the-shelf’ companies for small private companies renders promoters and pre-incorporation contracts of diminishing importance. Some courses may require students to be familiar with methods of raising capital – such material is likely to form a small part of a problem or be examined by means of a simple essay which merely demands a competent recitation of facts; but, obviously, every question setter has their own hobbyhorse(s).

Checklist

Students should be familiar with:

- ■ how a company can be formed and the different types of company;

- ■ advantages and disadvantages of incorporation;

- ■ effects of incorporation;

- ■ circumstances in which the separate legal personality of a company can be disregarded, both at common law and by statute (particularly fraudulent and wrongful trading);

- ■ promoters, particularly their duties and rights;

- ■ liability for pre-incorporation contracts.

Students should be aware that related issues which could be linked to questions based on this area include:

- ■ the distribution of power within a company;

- ■ enforcement of the articles of association;

- ■ liability and/or protection of directors/investors, including disqualification of directors;

- ■ restructuring of share capital.

Answer

Incorporation of an existing or projected enterprise (not necessarily a business) can be achieved either by forming a company in compliance with the procedure laid down in the Companies Act (CA) 2006 or by buying a pre-existing company ‘off-the-shelf’ (the latter procedure accounts for about 60% of ‘formations’). In either case, to incorporate a company, s 9 CA 2006 requires the delivery, to the Registrar of Companies, of a memorandum of association (s 8 CA 2006), an application for registration (ss 9–12 CA 2006) and a statement of compliance (s 13 CA 2006). Articles of association are also required to be registered, by virtue of s 18 CA 2006. The content of the articles, which are the company’s internal rules, are determined by the founders of the company. If articles are not registered or the articles that are registered do not exclude or modify the ‘default’ articles of the Companies (Model Articles) Regulations 2008 for different types of companies, the default articles will apply (s 20 CA 2006).1 Previously, the default articles were Table A of the CA 1985, if the company was limited by shares. The advantage of purchasing an off-the-shelf company is that the company already exists and there is no delay between deciding to form a company and the company coming into existence through the registration process; there is merely a transfer of shareholding. This obviates the problem of pre-incorporation contracts and the possibility of having stationery printed bearing a name which, by the time the company is registered, has been taken by another company. However, an off-the-shelf company would not have been formed with the specific requirements of the promoters in mind and alterations of the articles might be required. For most people interested in forming (or buying) a company, the appropriate form of company will be a private company limited by shares (ss 3(1), 3(2) and 4(1) CA 2006).

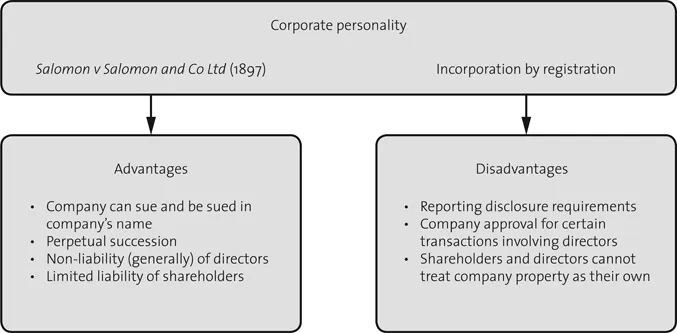

The UK has traditionally had more companies than other European countries of comparable size (there are more than two million limited companies registered in Great Britain and more than 300,000 new companies are incorporated each year). What are the attractions of incorporation? The principal advantage of incorporation, from which a variety of benefits flow, is that a company is a distinct legal entity with rights and duties independent of those possessed by its shareholders, directors and employees. In consequence, for example, business conducted in the name of a registered company is separate from the personal affairs of the human beings who act for the company, and separate also from the affairs of any other business that those human beings may conduct on behalf of another registered company. Corporate personality was created by statute in the first half of the nineteenth century, but the full significance of this provision was not appreciated until the famous case of Salomon v Salomon and Co Ltd in 1897.

In Salomon,2 S converted his existing, successful business into a limited company, of which he was the managing director. S valued his business at £39,000 (an honest but optimistic valuation) and received from the company, in discharge of this sum, a cash amount, a debenture (which is an acknowledgement of a debt) and 20,001 £1 shares out of an issued share capital of £20,007. S’s wife and five children each held one of the remaining issued shares (seven being the minimum number of shareholders at that date), probably as his nominee. The company went into insolvent liquidation within a year with no assets to pay off the unsecured creditors. The issue for the courts was whether S was liable for the company’s unpaid debts. The House of Lords, reversing the Court of Appeal, held that the company had been properly formed and was a legal person in its own right, separate from S, notwithstanding his dominant position within the company. The company was not S’s agent and, consequently, S’s liability was to be determined solely by reference to the CA 1862. The Act required a shareholder to contribute to the debts of a company only where he held shares in respect of which the full nominal value had not been paid. S had paid for his shares, in full, by transferring the business to the company, so he had no liability to the creditors of the company. Thus, the Salomon case established that legal personality would be recognised even where one shareholder effectively controlled the company and had fixed the value of the assets used to pay for those shares.3

The effects of separate legal personality are many and include the following:

- a company can sue and be sued in its own name;

- a company has perpetual succession. A company cannot die simply because all its shareholders are dead, although it can be wound up or struck off the register by the Registrar of Companies if it appears to be moribund. Because a company exists, unless and until it is wound up or deregistered, property, once transferred to the company, remains the property of the company, to do with as it pleases;

- the shareholders, directors and employees are not liable for criminal or tortious acts committed by the company, although they may incur personal liability concurrent with that of the company. For example, a company might, through the combined acts or omissions of several employees, establish and operate an unsafe system of work which caused the death of an employee. The company would be liable but an individual director or employee would not be liable unless he was personally negligent or the company was acting as an agent or employee of that individual;

- the shareholders, directors and employees are not liable on (nor can they enforce) contracts entered into by the company. As with criminal and tortious liability, an individual may incur personal liability concurrent with that of the company if he also enters into the contract. Furthermore, where the company acts as the agent of an individual, the individual is liable under the normal rules of agency;

- a company may be formed with limited liability (s 3(1) CA 2006). Limited liability allows the members of a company to limit their responsibility for a company’s debts. Liability may be limited to a predetermined sum, payable on winding up (a company limited by guarantee – s 3(3) CA 2006), or to the nominal value of the shares held, unless this sum has been paid by the current or a former shareholder (a company limited by shares – s 3(2) CA 2006). Since most shares are issued fully paid, shareholders have, effectively, no liability for the company’s debts;

- where a company has transferable shares, ownership of the company can be split or transferred without affecting the company itself;

- formation of a company may bring financial benefits. For example, a company can raise money to create floating charges and, perhaps, to minimise the tax liability of the shareholders.4

There are drawbacks to separate legal personality, in that the property of the company, not being that of the members, cannot be insured by a member and the company cannot claim on an insurance effected by a person on property which he then owned but subsequently transferred to the company (see Macaura v Northern Assurance (1925)). Moreover, the assets of the company are the property of the company and a shareholder, even a controlling shareholder, cannot simply help himself to the company’s cash. In addition, there is a limited number of situations where Parliament or the courts have decreed that corporate personality should be ignored, for example, where the directors have engaged in fraudulent or wrongful trading, they can incur personal liability under ss 213–214 of the Insolvency Act (IA) 1986. But what bureaucratic drawbacks are there to incorporation? In return for the advantages of incorporation, Parliament requires the observation of mandatory rules on the operation of a company. These rules are lengthy and complex and there can be no doubt that, in most companies, many administrative rules, for example on the conduct of meetings, are largely ignored. Perhaps in recognition of the widespread lack of use of some of the rules, the government reduced the administrative burden on companies, especially smaller companies, by the passing of the CA 2006. The CA 2006 permits a private company, for instance, to dispense with the holding of annual general meetings and to pass written resolutions by a bare or three-quarters majority.

Such reforms are small measures, and even with the passing of the Companies Act 2006 on certain administrative aspects of the formation and running of companies, there is still an immense amount of law imposing obligations upon companies, shareholders and directors which would not apply to a sole trader or to an ordinary partnership. These obligations fall into four broad groups:

- (a) Much of company administration is subject to statute (CA 2006) and there are rules relating to directors and the company secretary (ss 154–259 and ss 270–280 CA 2006, respectively, although a private company is no longer required to have a company secretary). The conduct of meetings of shareholders and directors...