![]()

PART 1

Forward Contracts and Futures Contracts

![]()

| CHAPTER 1 |

| SPOT, FORWARD, AND FUTURES CONTRACTING |

1.1 Three Ways to Buy and Sell Commodities

1.2 Spot Market Contracting (Motivation and Examples)

1.3 Forward Market Contracting (Motivation and Examples)

1.4 Problems with Forward Markets

1.5 Future Contracts as a Solution to Forward Market Problems (Motivation and Examples)

1.6 Futures Market Contracting

1.7 Mapping Out Spot, Forward, and Futures Prices

1.7.1 Present and Future Spot Prices

1.7.2 Forward Prices

1.7.3 Futures Prices

INTRODUCTION AND MOTIVATION

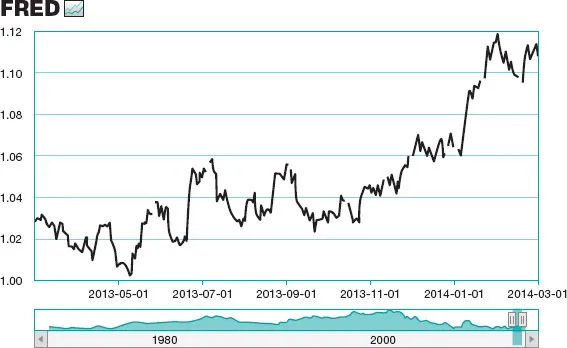

You will be traveling from your home country to Canada in a month and you know that you will need to obtain Canadian dollars to use while in Canada. To get an idea of the risk you face, you decide to look at the Canadian/US dollar exchange rate. Indeed, over the past year it has fluctuated with parity occurring around May 2013. The risk to you is that you may have to pay more for Canadian dollars in a month than you would pay today. Of course, it is possible that you could pay less in a month.

The problem is that you do not know today whether your currency will depreciate or appreciate relative to the Canadian dollar. You face currency (foreign exchange=FX) risk. Figure 1.1 indicates how many Canadian dollars were contained in 1 USD$ over the period March 2013–March 2014. This is what is meant by USD/CAD.

It is defined as USD$1/(US Dollar Value of 1$CAD), and describes how many Canadian dollars it takes to buy 1 US dollar, or how many Canadian dollars are ‘in’ 1 US dollar, or the Canadian dollar price of 1 US dollar.

For example, the CAD dollar price of 1 US dollar was approximately 1.1 Canadian dollars in March 2014. By solving USD$1/(US Dollar Value of 1$CAD)=1.1 for the denominator, this translates into the US dollar value of 1CAD$ of USD$ 0.90. You can see from this example that understanding the ‘quote mechanism’ is important. Are we quoting Canadian dollars in terms of US dollars, or are we quoting US dollars in terms of Canadian dollars? Understanding the quote mechanism is an essential prerequisite for being able to intelligently deal with derivatives and the instruments that underlie them.

One Canadian dollar was worth 0.90 US dollars in March 2014. A move upward (downward) in the USD/CAD ratio indicates that the Canadian dollar is depreciating (appreciating), because there are more (fewer) Canadian dollars in 1 US $. If it takes more Canadian dollars to purchase 1 US dollar, then the Canadian dollar is depreciating relative to the US dollar. Another way to put this is that if 1 US dollar buys more (fewer) Canadian dollars, then the Canadian currency is weakening (strengthening) relative to the US dollar. Alternatively, more USD in a single CAD dollar means that the CAD is appreciating relative to the USD dollar.

FIGURE 1.1 Canada/US Foreign Exchange Rate

Source: St. Louis Fed, reprinted with permission.

1.1 THREE WAYS TO BUY AND SELL COMMODITIES

What are your alternatives today to try and manage the foreign exchange risk you are certain to experience? To answer this important question we first examine the ways in which you can transact in a foreign currency. There are three main ways. You could transact:

1. In the spot (cash) market;

2. in the forward market, or;

3. in the futures market.

1.2 SPOT MARKET CONTRACTING (MOTIVATION AND EXAMPLES)

What does it mean to transact in the spot market? The easiest way to think about this is as a cash and carry transaction. You go out and buy something for immediate delivery and you pay the going price in the market. For example, you fill your car’s gas tank with gasoline. When you do so, you pay the (posted) spot price of gasoline even though the theoretical spot price determined in the spot market for gasoline keeps changing, based upon demand and supply conditions. Most of our purchases are of this form, but there are some notable exceptions.

Let’s formalize the idea of spot markets and spot transactions.

Spot (Cash) refers to the characteristic of being available for immediate or nearly immediate delivery. Other features are:

• No standardized contract;

• no organized exchange in which trading necessarily takes place;

• commodities underlying spot transactions may have different grades (quality levels);

• the terms of a spot agreement are tailor-made to suit the parties to the agreement.

These terms include:

a. Grade;

b. time of delivery. Financial instruments sold in the spot market usually have a 0-day to 3-day delivery window;

c. place of delivery;

d. other terms as suit the parties.

A spot transaction is one in which two (counter)parties engage in a transaction for immediate or nearly immediate delivery of some commodity.

The spot market is the (not necessarily organized) market in which spot transactions take place. It is an abstract entity. The spot market is just the set of all spot transactions.

The spot price of a commodity, at a point in time, is the price a...