![]()

Section 1

Overview

![]()

1

Introduction

Theresa Libby and Linda Thorne

In 1967, Becker presented the notion of “behavioural accounting” as the application of methods and approaches from the behavioural sciences in investigating the interface between accounting and human behaviour (Birnberg and Shields 1989). Today Behavioural Accounting Research (BAR) can be defined as the systematic observation of people creating, reporting and/or responding to accounting data. Behavioural accounting researchers evaluate behaviours, judgments, decisions, cognitive and physiological responses to accounting information and disclosures individually and in the aggregate.

The field and approaches relied upon by behavioural accounting researchers have expanded in the 50 years since its inception to include theories and techniques adapted from psychology, sociology, ethics as well as economics via behavioural economics. Although historically, the BAR methodology has been considered to be synonymous with the use of traditional psychological experiments, BAR has “moved beyond the lab” as it has evolved to encompass surveys, interviews, case studies, field studies and more recently neuroscientific approaches.

This volume provides a compilation of existing approaches that are used in BAR to provide an archive for experienced and budding researchers. The aim of this volume is to provide an overview of the theories, methodologies and data collection techniques relied upon in BAR. In so doing, we believe that this volume presents an invaluable resource for established researchers seeking a single repository on the current state of BAR methods, debates and relevant literature as well as for graduate students and scholars for their initial introduction and exploration of the array of theories, techniques and methodologies used in BAR.

Content and structure

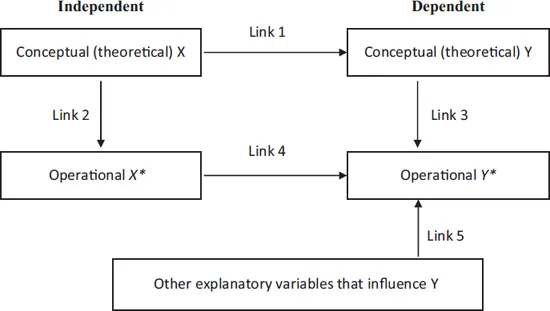

This volume contains 32 chapters, which are organized into seven thematic sections loosely based upon the structure of the predictive validity framework (fondly known by BAR researchers as “Libby boxes”) (See Figure 1.1). We have reprinted Chapter 1 of Libby (1981) (currently out-of-print) due to the prominence and widespread adoption of the ideas expressed in that chapter throughout the field. “Libby boxes” are not only a useful framework for the organization and evaluation of BAR research, but are valuable as an organizing framework for all types of empirical research.

Figure 1.1 The predictive validity framework (or “Libby boxes”)

The Libby framework identifies five key links as being critical to validity in Behavioural Accounting Research design (see Figure 1.1). Link 1 captures the role of theory as the foundation of rigorous research. Theory describes, a priori, the relationship between two variables or constructs: the independent variable that is the catalyst to a causal relationship, and the dependent variable that captures the impact or effect of the causal relationship. Link 2 evaluates the operationalization of the independent variable, which involves an evaluation of how well the measurement of the independent variable captures the theoretical constructs as described in the theory. Link 3 evaluates the operationalization of the dependent variable, which involves an evaluation of how well the measurement of the dependent variable captures the theoretical constructs as described in the theory. Link 4 evaluates the association between the dependent and independent variables and assesses the extent to which the operationalization of the association in the research captures the theoretical relationship as described in Link 1. Link 5 is the assessment of contextual variables and controls, which considers how context and other factors may be unique to a particular study.

This volume is organized consistent with the links in the predictive validity framework as follows. The first section of this volume includes three overview chapters. The first chapter is this Introduction. The second chapter is a particularly important contribution to this volume as it presents William Kinney’s framework on how to plan a study. Many of us have already been introduced to “Kinney’s three paragraphs” which he uses as an important organizational approach to the initiation of Behavioural Accounting Research. The third chapter is the reprint of the original Libby (1981) chapter as discussed above.

The second section of this volume focuses on Link 1 of the predictive validity framework by presenting an overview of five theoretical perspectives relied upon by behavioural accounting researchers. Chapter 4 describes the BAR literature specifically grounded in the judgment and decision-making (JDM) research based on a cognitive psychological perspective. Chapter 5 describes the foundation and the current state of social-psychological BAR research. Chapter 6 presents an overview of various theoretical frameworks in ethics, morality and philosophy as applied to BAR. Chapter 7 outlines the two dominant sociological theories used in BAR research: stakeholder and legitimacy theories. Chapter 8 describes the dominant economic theory, agency theory, as applied to BAR questions. All five theoretical perspectives have been used extensively in BAR research.

The third section of this volume focuses on Link 2 and Link 3 of the predictive validity framework by identifying how to operationalize the theoretical constructs, which applies to both the independent variable (Link 2) and the dependent variable (Link 3). There are three chapters in this section. Chapter 9 describes how to create valid and reliable measures of accounting constructs. Chapter 10 discusses the development and use of manipulation and attention checks in Behavioural Accounting Research. Chapter 11 examines the impact of and potential controls for social desirability in accounting measures.

Link 4 evaluates the extent to which the operationalization of the relation under study captures the theoretical relationship. It captures both methodological and data analysis choices. More specifically, Link 4 choices include the selection of a study design, choices made in the implementation of a study and data analysis. Accordingly, we have devoted three separate sections of this volume to the choices inherent in Link 4: (a) Link 4a are the study design choices that are considered in the fourth section of this volume; (b) Link 4b are study implementation choices that are considered in the fifth section of this volume and (c) Link 4c are data analysis choices that are considered in the sixth section of this volume.

The fourth section includes six chapters that focus on Link 4a, study design choices. Chapter 12 discusses the potential for diversity in methodological approaches to Behavioural Accounting Research. Chapter 13 examines judgment and decision-making (JDM) research methods and design choices. Chapter 14 illustrates how experimental economics theories and approaches can be applied to BAR. Chapter 15 introduces the complexities and necessities related to survey research. Chapter 16 presents an overview of field research techniques for behavioural accounting researchers, while Chapter 17 specifically discusses the techniques and importance of case study research for BAR. Chapter 18 presents new technologies that have only recently been adopted in BAR. These include MRI imaging, retinal scans and other physiological responses to the presentation of accounting information.

The fifth section includes four chapters that present important considerations for study implementation inherent in Link 4b. Chapter 19 considers ethical aspects of conducting BAR, which includes getting ethics approval, priming subjects and deception. Chapter 20 considers the use of student subjects and introduces Mechanical Turk (MTurk), which is Amazon’s computer workforce database that has been increasingly useful in BAR. Chapter 21 introduces the importance of sample size and the notion of power for BAR.

The sixth section addresses Link 4c in five chapters that consider the choices inherent in data analysis of BAR. Chapter 22 outlines preliminary data analysis and data cleansing techniques in BAR. Chapter 23 compares and contrasts the appropriateness of ANOVA as compared to regression in BAR, and considers simple effects analysis. Chapter 24 discusses tests for mediation and moderation, as well as mediated moderation, in BAR. Chapter 25 outlines structural equation analysis and its use in BAR. Chapter 26 presents specialized and emerging multivariate approaches in BAR including cluster analysis, Logit and Probit techniques.

The seventh section addresses contextual controls within Link 5, which considers how context and other factors that may be unique to a particular BAR study impacts validity of the data collected. We specifically include three chapters that consider distinctive contexts in BAR. Chapter 27 specifically considers BAR in the tax context. Chapter 28 presents an overview of specialized considerations for cross-cultural BAR research. Chapter 29 considers special aspects of risk management in BAR research.

The final and eighth section presents three chapters that address publication considerations. Chapter 30 presents a framework and an approach to writing a literature review. Chapter 31 outlines an approach and considerations in writing a BAR article review for a journal. Chapter 32 discusses the importance of replication in BAR. We truly hope the readers will find this volume comprehensive and helpful in their own Behavioural Accounting Research.

References

Birnberg, J. G. and Shields, J. F., 1989, ‘Three decades of behavioural accounting research: A search for order’, Behavioral Research in Accounting 1, 23–74.

Libby, R., 1981, Accounting and Human Information Processing: Theory and Applications, Prentice Hall, Upper Saddle River, NJ.

![]()

2

Planning for research success by answering three (universal) questions

William R. Kinney, Jr.

So, you have some possible insights about accounting – how the world works, what causes what, or how to fix what’s broken. How can you convince others – research consumers and your critics (editors/reviewers/competitors) – that you are right? What evidence must you obtain to convincingly “stress test” your ideas, and how should you write up what you did (and found) and why does it matter?

This chapter can help you as a student or new scholar address these questions using three structured paragraphs. Using the approach, you customize the content of three related paragraphs with defined objectives for efficiently and effectively communicating the essentials of your research. The pre-set objectives are almost universal in that they address questions your readers will be asking. Using the approach helps you plan what you do in conducting your own research while you also plan to be successful because you will preemptively identify and may resolve some issues likely to be raised by others when they read your work.

We’ll support the three paragraphs with a few basic statistical relationships (but omitting proofs and details) and add research concepts I’ve gleaned from others that can help build your intuition about how to structure and refine your own ideas.1 There is no rigorous review of philosophy of science or a generic research design template able to accommodate all types of empirical accounting-related research ideas (Kinney 1986, 1992). Also, there is nothing original here, save maybe the combination of the elements – all of which need not appear in every paper.

Instead, the approach is simply a way to help you articulate the intuition behind your implicit research plan, anticipate what others will ask you, and systematically evaluate and improve your chances for research success ex ante. The answers are based on the conceptual thinking underlying four types of operational variables and basic statistics for stress tests, plus five boxes to help you evaluate (and modify as needed) your own plan via a format for assessing research validity or “believability”.

You can apply the three-paragraph approach iteratively as your research progresses. Plus, your peers can help you and you can help them by presenting only three short and stru...