eBook - ePub

Applying MBA Knowledge and Skills to Healthcare

- 156 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Applying MBA Knowledge and Skills to Healthcare

About this book

Clinicians increasingly need a firm grasp of the fundamental principles of business management, finance and related subjects. Even so, business disciplines are still rarely taught during medical training, while busy practices and complicated accounting tasks mean that gaining business acumen 'on the job' is impractical for many. As a result, increasing numbers of clinicians learn the skills they need by taking an MBA (Masters in Business Administration). While an MBA may be the answer for some, the formidable costs and time commitment it demands leave many busy practitioners seeking more accessible options. This book provides a readable, tightly organised alternative - a primer on MBA principles and their practical application. Twelve compact, carefully structured modules cover the entire gamut of a business education, from basic finance and accounting principles, to strategic management methods and leadership theories. Unlike some similar texts, this book is designed to be light in tone, easy to read and digest, and thoroughly practical. Busy clinicians, academic surgeons, administrative physicians and other healthcare professionals will find this an invaluable resource in understanding the core principles of business management. Allied medical professionals, and nurses will also find it useful, as will interview candidates who increasingly face management questions as part of selection processes. 'An invaluable resource in understanding the core principles of business management, and in learning how to apply them. For busy clinicians, the value proposition is enormous in terms of the knowledge gained, versus the amount of reading required to capture what the authors have so capably managed to distill between the covers. The authors have done a remarkable task in capturing the latest concepts and thinking in the business management arena [and] the essence of an entire MBA education, and customise it for healthcare professionals. A delight.' From the Foreword by B Sonny Bal

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

MODULE 1

Accounting and finance

Finance may be considered as the heart of any organisation, which requires cash flow to circulate throughout it to provide other parts with resources to maintain their vitality. Understanding financial basics is crucial for any managerial role within an organisation. We shall explore basic terms and techniques used in finance and illustrate these with examples. So let’s start with the definitions, as there is often confusion between accounting and finance.

Accounting is basically the system of making records, verifications and reporting of the value of assets, liabilities, expenses and income in the account books. The transactions are posted chronologically to record changes in value of assets and liabilities. It is the process of collecting and recording data about the use of funds within an organisation. The clinical analogy is the collection of blood and biopsy to make diagnoses and how they are recorded in the clinical notes.

Accounting

There are two types accounting for an organisation.

- ➤ Financial accounting – focuses on information for people outside the firm. These may include creditors and outside investors, who are not part of the day-to-day management of the company. Government agencies and the general public are external users that may be interested in accounting information.

- ➤ Management accounting – focuses on information for internal decision makers, such hospital administrators.

Finance

Finance refers to the time, money and risk associated with a specific business. Finance differs because it works on the accounting information to predict future trends or to make decisions about the future. This is analogous to clinical medicine, where, through your history, examination and investigations, you make a clinical decision based on calculated risk to treat your patient. Finance is concerned with the raising of funds to meet the various cash flow needs of the organisation. Finance functions start from gathering the cash flow information from the accounting records and preparing projections of cash flow. Finance activities are concerned with preparing budgets, undertaking comparisons and finding variances. Finance activities therefore will encompass both the accounting and operations aspects of an organisation.

Company law requirements for financial accounts

Every UK Company registered under the Companies Act is required to prepare a set of accounts that give a true and fair view of its profit or loss for the year and of its state of affairs at the year-end.

Annual accounts for Companies Act purposes generally include the following.

- ➤ Directors’ report – Description by the directors of the performance of the business during the accounting period + various additional disclosures, particularly in relation to directors’ shareholdings, remuneration, etc.

- ➤ Balance sheet – Statement of assets and liabilities at the end of the accounting period (a ‘snapshot’) of the business.

- ➤ Profit and loss account – Describing the trading performance of the business over the accounting period.

- ➤ Statement of total recognised gains and losses.

- ➤ Cash flow statement – Describing the cash inflows and outflows during the accounting period.

- ➤ Audit report.

- ➤ Notes to the accounts – Additional details that have to be disclosed to comply with Accounting Standards and the Companies Act.

In England, the accounts of an NHS foundation trust must comply with International Financial Reporting Standards (IFRS) as adopted by the European Union. All private healthcare organisations have to comply by the company law requirements.

In the United States, companies can become limited liability companies, incorporated or corporations. The exact terminology used varies depending on the requirements and from state to state. The corporate business law also varies between different states. Limited liability companies tend to have less legal requirements and formalities than corporations.

The three main financial statements outlined in the above legal requirements are therefore:

- ➤ balance sheet

- ➤ profit and loss account

- ➤ cash flow statement.

We shall look at these individually and examine their components and composition. In order to illustrate these principles, we shall present a case study of a fictional company.

The accounting formula

The basis of accounting revolves around the formula shown in Figure 1.1.

This equation has three components, which are as follows.

Figure 1.1: The accounting formula

Assets

These are the rights and things that a company owns. They can be classified as either current or fixed assets. This is determined by the liquidity of the assets. Liquidity can be described as the ability to settle costs with cash or assets that can be promptly converted to cash. In this case, current assets are things that can be converted into cash within a year. Current assets include stock, cash and trade debtors (money owed to you). Fixed assets are intended for long-term or continuing use to allow the organisation to conduct its business. Fixed assets may be classified into tangible and intangible. Tangible fixed assets include land, property, machinery and vehicles. With time the value of these fixed assets will reduce – this is called depreciation. For instance, a hospital purchases a MRI scanner but the life span of this machine is limited. Over the life span of the scanner its value reduces. There are differing techniques to account for depreciation and seeking professional advice is recommended. Intangible fixed assets are things such as goodwill, patents, copyrights and brands an organisation may possess.

Equity

In order to acquire assets, an organisation needs to obtain cash from differing sources. Equity or capital is the cash invested into the company by its owners or shareholders.

Liabilities

Further cash is acquired from other sources such as bank loans. These are borrowings the company owes, which are referred to as liabilities. These can again be classified into current and long-term liabilities. The differentiation between the two depends on the duration over which the liability is owed. Short-term liabilities may include money owed to suppliers, short-term loans or taxes due. Therefore, if a company owes something within a year this is a current liability and beyond a year it becomes a long-term liability. Examples of long-term liabilities include bank loans and finance agreements due to be repaid after one year.

Now the components of the accounting formula have been defined, we can see how they make up the balance sheet.

Case study

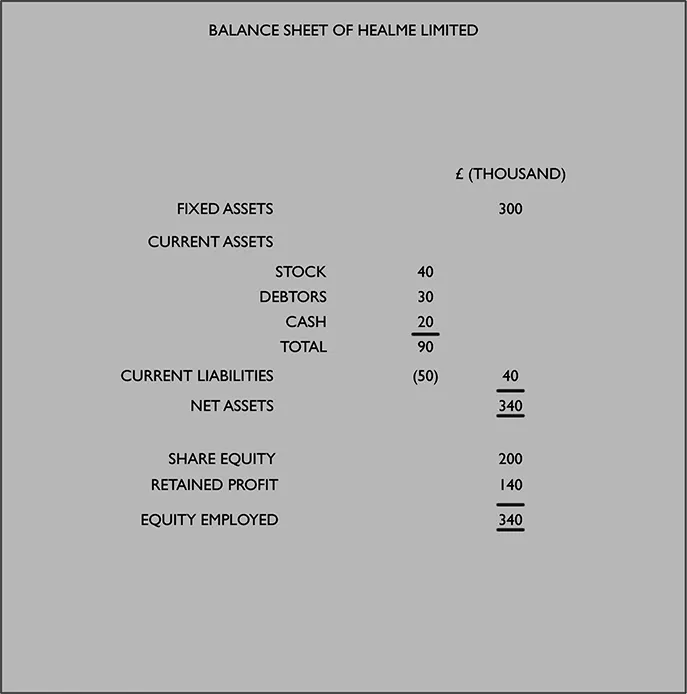

HealMe Limited was established almost a year ago and produces a medicinal preparation that when applied to a wound helps the healing process. The company was set up by a small group of friends who had invested a significant amount of their own money. They needed additional funding and approached their bank for a loan, which was granted. Using their initial investment they purchased a factory and machinery to produce their product.

Balance sheet

The balance sheet is a statement of an organisation’s assets, equity and liabilities at a particular date, which is usually the last date of the accounting period. This provides an overview of how the organisation is being funded and how the funds are being utilised (see Figure 1.2).

The balance sheet for HealMe Limited illustrates the main three components, which are assets, liabilities and equity. In this example, the fixed assets (such as property and machinery) are valued at £300 000. Current assets are also available totalling £90 000. The company has some current liabilities, which are deducted resulting in a net asset of £340 000. Equity comes from the investment by shares and also some retained profit. The value of this equity should, according to our equation, be equal to assets less liabilities. This statement therefore balances.

Figure 1.2: Balance sheet

Profit and loss account

This statement summarises the organisation’s trading transactions, which comprise income, sales and expenses. This statement is also based on an equation (see Figure 1.3). Profit should be one of the primary drivers for any organisation. The profit and loss account looks at transactions over a period of time, unlike the balance sheet that only provides a snapshot at a particular time.

Table of contents

- Cover

- Half Title

- Title Page

- Copyright

- Table of Contents

- Foreword

- About the authors

- List of abbreviations

- Introduction

- Module 1: Accounting and finance

- Module 2: Operations management

- Module 3: Marketing in healthcare

- Module 4: Strategic management for clinicians

- Module 5: Information technology (IT)

- Module 6: Human resource management

- Module 7: The clinical team

- Module 8: Clinical leaders

- Module 9: Managing clinicians’ performance

- Module 10: The learning and teaching clinician

- Module 11: Coping with change in the clinical environment

- Module 12: Innovation in medicine

- Glossary

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Applying MBA Knowledge and Skills to Healthcare by Reza Nassab,Vaikunthan Rajaratnam,Michael Loh in PDF and/or ePUB format, as well as other popular books in Medicine & Medical Theory, Practice & Reference. We have over 1.5 million books available in our catalogue for you to explore.