eBook - ePub

Accounting Irregularities in Financial Statements

A Definitive Guide for Litigators, Auditors and Fraud Investigators

- 232 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Accounting Irregularities in Financial Statements

A Definitive Guide for Litigators, Auditors and Fraud Investigators

About this book

Accounting irregularities are at the heart of those kinds of frauds that hit financial statements and include misstatement, misclassification as well as misrepresentation. In essence, they involve manipulation of accounting data, description or disclosure in order to distort the true financial picture of the organization in question. This book provides an in-depth practical reference, designed for litigators, investigators, auditors, accountants and other professionals who need to understand and combat accounting irregularities and to uphold the integrity of financial statements. Regulators will find this book an essential source of ideas and references when considering reforms. Educators and students will see this book as an alternative, inspiring way of understanding accounting and how to stay alert for accounting irregularities. The first two chapters introduce the basics of accounting irregularities in the context of the financial reporting environments, and generally accepted accounting principles in the UK and Hong Kong. Perpetrators often seek ways to creating financial illusions in four common directions - selling more, costing less, owning more and owing less as discussed in Chapters 3 to 6. The seventh chapter considers various ways that perpetrators manipulate the classification and disclosure of financial statements. Chapter 8 explores three scenarios of accounting irregularities - tax evasion, theft and commercial dispute. The concluding chapter sets out the deterrents to accounting irregularities in two dimensions. At the micro-level, deterrents are implemented within the authority of the organization in question, whilst the macro-level deterrents refer to the external environment beyond the controls of any individual organization.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

Overview of Financial Reporting Environments

Accounting, or more specifically financial reporting, is not a subject that can be gauged with complete precision. Financial reporting is not scientific and objective in the sense that science and engineering can be. No matter how intelligent and educated they might be, accountants cannot measure the financial performance of an organization in the same way that engineers can measure the weight of a piece of metal since there are not the same undisputed measurement criteria in accounting as there are in the case of engineering.

Accounting is founded on the basis of a business environment which, as we all know, is ever changing. Accounting is often known as the common language for business in translating the transactions and events into numbers and in communicating the financial performance to the outside world.

Financial statements are the summary of the accounting for a financial year prepared within an applicable financial reporting environment. There are no ‘correct’ financial statements as such. It is a balancing act between various factors on the basis of the availability of relevant records and the transactions and events that an organization might have undertaken.

From Chapters 3 to 8, we shall consider how accounting irregularities may exist in three main aspects of the financial statements which are:

• the profit and loss account (P&L)

• the balance sheet (B/S)

• notes to the financial statements (Notes).

There are other aspects (or components) of financial statements, such as cash flow statements, as governed by the jurisdiction to which an organization is subject. However, P&L, B/S and Notes are by far the dominant features attracting the most attention of readers of financial statements.

The term ‘organization’ is used throughout this book to include companies, partnerships, trusts, charities, sole proprietorship and other forms of entities requiring the preparation of financial statements in making economic decisions. In other words, financial reporting is driven by the information needs of the readers of financial statements. Typically, readers of financial statements include providers of finance, shareholders, employees, customers, vendors and governments.

The P&L is a statement in which revenues and expenditure are matched to arrive at a figure of profit or loss. Most organizations distinguish between a gross profit earned on trading and a net profit after other revenue and expenses. The P&L is arguably the most significant single indicator of an organization’s success or failure. It is very important to ensure that it is not presented in such a way as to be misleading. This could happen either through an inconsistency within an organization or between different organizations; or it could arise as a result of deliberate manipulation of accounting figures.

The B/S is a statement of the assets, liabilities and capital of an organization at a given moment in time. It is like a ‘snapshot’ photograph, since it captures on paper a still image, frozen at a single moment in time, of something which is dynamic and continuously changing. Like any photograph, it can be taken from different angles and standpoints. The B/S gives an indication of what the business is worth at the end of the financial year, given a set of assumptions that are detailed in the Notes. The B/S is important to an organization because it is used to determine things such as the creditworthiness, cost of funding and attractiveness to potential investors.

Notes are in narrative format and tend to be the largest part of the financial statements. They show the accounting policies used in the preparation of the financial statements and the basis of how all the numbers in the financial statements have been calculated. Understanding of the Notes is essential in detecting accounting irregularities.

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES – GAAP

Generally accepted accounting principles (GAAP) is a term representing rules from all authoritative sources governing accounting. The primary sources of these rules are:

• statutory requirements of the jurisdiction to which the organization’s financial statements are subject;

• accounting standards of the jurisdiction to which the organization’s financial statements are subject;

• stock exchange requirements (for listed organizations).

In addition to the above sources, the basis of GAAP for individual jurisdictions may hinge on certain non-mandatory sources, such as:

• international accounting standards;

• statutory requirements in other jurisdictions (e.g. the influence from the US).

‘Financial reporting environment’ is a high-level umbrella term, covering a number of variables and components, such as GAAP, the frequency and distribution of financial statements, and the composition and function of the board of directors. Many of the key components of the financial reporting environment form an essential part of corporate governance. Corporate governance is a concept considered in Chapter 9 as a deterrent to accounting irregularities.

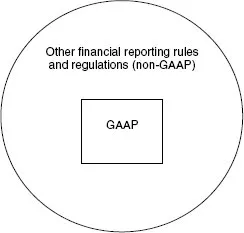

The ambit of the financial reporting environment can be drawn as a circle as shown in Figure 1.1. GAAP is at the centre, surrounded by other financial reporting rules and regulations, setting out the boundary in which the financial statements of organizations are being reported to their readers.

Figure 1.1 Circle of financial reporting environment and GAAP

In the US, the financial statements are required as ‘fair presentation in accordance with GAAP’ (which is equivalent to the ‘true and fair view’ in Hong Kong and the UK). GAAP are defined as those principles which have ‘substantial authoritative support’. Therefore, financial statements prepared in accordance with accounting principles for which there is not substantial authoritative support are presumed to be misleading or inaccurate.

Although the term GAAP is widely used throughout this book, it is important to bear in mind that even as generally accepted, GAAP may not be relevant to all kinds of organizations in all circumstances. Any accounting practice which is appropriate in a particular circumstance should be regarded as GAAP. Whether or not such a practice has been generally adopted or commonly used is not necessarily the overriding consideration. In addition, the term ‘generally accepted’ in GAAP implies a high degree of practical application of a particular accounting practice. However, there are newly introduced GAAP and new areas of accounting which have not, as yet, been generally applied. There are frequently different accounting treatments for similar items, and they are all generally accepted.

The general views shared in Hong Kong and the UK are that, as evidenced by the constantly changing legislations, accounting standards and stock exchange listing requirements, GAAP is a dynamic concept constantly being reviewed and adapted in response to changing business priorities and economic environments. As circumstances change, different accounting practices are adopted accordingly. GAAP goes far beyond rigid rules and principles, and anticipates emerging contemporary accounting practices. A conceptual framework is established by the accounting profession in Hong Kong and the UK1 as well as the US. Applying a conceptual framework in financial reporting is an attempt to codify and test the consistency of existing GAAP and to assist the development of future standards.2

FINANCIAL REPORTING ENVIRONMENT IN HONG KONG

In Hong Kong, the financial reporting environment is based on three principal sources:

• Companies Ordinance – Chapter 32

• Accounting standards, or more specifically the Statements of Standard Accounting Practices (SSAP) – all SSAP are being changed and renamed as the Hong Kong Accounting Standards (HKAS), which themselves are to be phased out gradually and replaced by the Hong Kong Financial Reporting Statements (HKFRS) as from 1 January 2005

• Listing rules.

Hong Kong, a British colony until 1997, has a common law jurisdiction. An outline of the financial reporting requirements is set out in the Companies Ordinance. Accounting rules and more specific details are developed by the self-regulated private sector through accounting standards and listing rules.

COMPANIES ORDINANCE

In Hong Kong, companies incorporated under the Companies Ordinance are required to maintain proper books of account, so as to show at any time a true and fair view of the state of the company’s affairs and to explain its transactions.3

Such books must include details of receipts and payments, sales and purchases of goods, and the assets and liabilities of the company.4 The books of account must be kept at the registered office of the company or at another location chosen by the directors, provided that, if the books are kept outside Hong Kong, sufficient information is maintained in Hong Kong to disclose with reasonable accuracy the financial position of the company at any time.5 The books of account must also be kept for seven years from the end of the financial year to which they relate.6

Every company registered under the Companies Ordinance is also required to prepare:

• a B/S which gives a true and fair view of the state of affairs of the company as at the end of its financial year; and

• a P&L which gives a true and fair view of the profit or loss of the company for the financial year.7.

The requirement for a true and fair view overrides all other accounting requirements of the Companies Ordinance, accounting standards or listing rules. For example, if the financial statements drawn up in compliance with the detailed requirements of the Companies Ordinance do not give sufficient information to present a true and fair view, then the necessary additional information should be given in the financial statements.

The financial statements must be approved by the board of directors and signed on their behalf by two directors on the face of the B/S.8 A copy of the financial statements, together with the auditors’ report and directors’ report on those financial statements, must be sent to every member and debenture holder not less than 21 days before the date of the annual general meeting.9 The audited financial statements of a company must be presented to the shareholders of the company at the annual general meeting and the financial statements should be made up to a date falling not more than six months before the date of the annual general meeting.10 The directors of a company, other than a private company, must include a copy of the audited annual financial statements, auditors’ report and directors’ report in the company’s annual return to the Registrar of Companies within 42 days following the annual general meeting.11

While the main body of the Companies Ordinance dictates when and which companies must prepare financial statements, the Tenth Schedule is primarily concerned with the specific disclosure requirements in their financial statements. The financial reporting information required by the Tenth Schedule includes:

• the basis on which the amount of Hong Kong profits tax is calculated;

• the basis on which turnover for the year is arrived at;

• details on finance costs;

• auditors’ remuneration;

• details of land leases held;

• details on other investments, distinguishing between listed and unlisted portions, and related outstanding indebtedness;

• details on capital commitments, whether authorized or contracted for;

• aggregate amount of loans to trustees or employees; and

• details on debentures, loans and bank overdrafts, including details of secured liabilities.

ACCOUNTING STANDARDS

The Hong Kong Institute of Certified Public Accountants (HKICPA) (previously known as the Hong Kong Society of Accountants until September 2004) is the only statutory body (constituted under the Professional Accountants Ordinance) to license and regulate professional accountants in Hong Kong. The HKICPA may, in relation to the practice of accountancy, issue or specify any standards of accounting practices required to be observed, maintained or otherwise applied by its members.

The HKICPA has been developing accounting standards to achieve convergence with the International Financial Reporting Standards (IFRS) issued by the Internation...

Table of contents

- Cover

- Half Title

- Title Page

- Copyright Page

- Table of Contents

- List of Cases

- List of Tables

- List of Figures Preface

- Preface

- Acknowledgements

- 1 Overview of Financial Reporting Environments

- 2 Basics of Accounting Irregularities

- 3 Selling More

- 4 Costing Less

- 5 Owning More

- 6 Owing Less

- 7 Presenting It Better

- 8 Other Types of Accounting Irregularities

- 9 Deterrents to Accounting Irregularities

- Glossary

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Accounting Irregularities in Financial Statements by Benny K.B. Kwok in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.