![]()

p.1

1

THE PAST, PRESENT, AND FUTURE FOR INTELLECTUAL CAPITAL RESEARCH

An overview

John Dumay, James Guthrie, Federica Ricceri, and Christian Nielsen

Introduction

When we started this project three years ago, we started with the aim “to provide an overview of Intellectual Capital (IC) in practice and beyond. It will focus on the role of IC in organizations and between organizations, institutions and beyond”. The Routledge Companions are similar to what some publishers call ‘handbooks’, being prestige reference works providing an overview of a whole subject area or sub-discipline, which survey the state of the discipline including emerging and cutting edge areas. The Routledge Companions produce a comprehensive, up to date, definitive reference that are usually cited as an authoritative source on the subject. Our goal in undertaking this project is to provide a collection of essays that address cross-cutting IC issues. We believe we have achieved our aims and our collected works should be of interest to people who want to understand IC from a variety of perspectives with a view that readers may or may not have background knowledge, as well as students who are learning to work with a particular aspect of IC and the management of knowledge. The material in this Routledge Companion relates not only to theory, but also to practice and case studies.

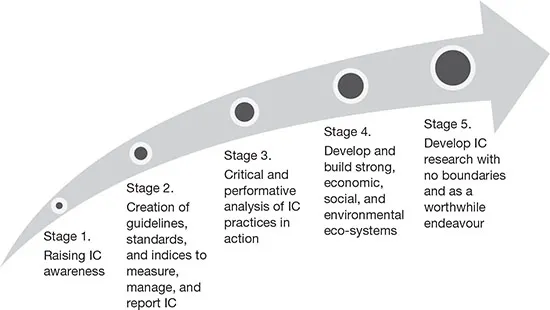

We are proud that this book features leading academic, policy, and practitioner articles examining the latest developments in the field of IC. The contents are organized thematically into sections that reflect the five stages of IC research developments (Dumay et al., 2017). We believe no one stage is more important than another – the themes and stages provide a useful framework with which to present the 30 chapters, written by a variety of authors and covering a wide range of subject areas.

Frontiers of research, practice, and knowledge

Intellectual capital, intangible assets, and even intangible liabilities. These terms are most likely familiar to readers of this book. It is probable that what attracts you to this collection is that the chapters herein offer state-of-the-art thinking about IC practice and research. We believe we will not let down readers familiar with these terms as we provide new understandings into how established and new authors from research and practice outline their insights, critique, and ways forward for creating value for all organizations. Additionally, the chapters in this book also offer readers who are relatively new to the IC and intangible assets field access to contemporary research that allows them to quickly position themselves and take the journey that we have taken with many others.

p.2

To ensure we capture the progress being made in contemporary IC research, we include chapters by the seminal IC authors, or as Leif Edvinsson likes to call some of them, the ‘grandfathers’ of IC. Thus, we include chapters by James Guthrie, Robin Roslender, Leif Edvinsson, John Holland, Ulf Johanson, Henrik Dane-Nielsen, Karl-Erik Sveiby, Aino Kianto, and Göran Roos. A virtual who’s who of the early days of IC research and many of whom have their roots in practice. In adding to contemporary IC practice, we also have the pleasure of including active IC practitioners such as Mary Adams (US), and Manfred Bornemann (Austria and Germany). Similarly, we also include some of the young(er) ‘guns’, who have since the mid 2000s been blazing a new trail, such as John Dumay, Jim Rooney, Grant Samkin, Gunnar Rimmel, Maria Serena Chiucchi, Emidia Vagnoni, Suresh Cuganesan, Christian Nielsen, Marco Giuliani, and Tatiana Garanina. Then there is the new blood in the likes of Henri Hussinksi, Paavo Ritala, and Marco Montemari. Thus, the authors of chapters in this book are inclusive of many of the best that have served IC research and practice well, along with those who will serve it well into the next generations of IC research.

Arguably, IC is having a resurgence because a new reporting framework, Integrated Reporting (<IR>), makes use of IC as part of its six capitals framework (International Integrated Reporting Council (IIRC), 2013). As Dumay (2016, p. 175) outlines:

The latter fact that IC in <IR> equates to structural capital in the traditional tripartite model of IC as human, relational, and structural capital (Petty and Guthrie, 2000), is an important point of departure for future IC and intangible assets research because, as noted, the terms are often used interchangeably (Eccles and Krzus, 2010), and in different contexts. For example, in European and North American business parlance, the term ‘intangible assets’ is used more often than ‘intellectual capital’ (Cuozzo et al., 2017). So, while we see an initial resurgence in IC, we need to be clear about what it is as several authors discuss it in their chapters.

Another issue we need to be explicit about is that of ‘value’ or ‘value creation’, two terms frequently used without being adequately defined (see Bowman and Ambrosini, 1998). The meaning of value creation has evolved from Thomas Stewart’s (1997, p. x) initial definition of IC whereby value creation is associated with the ability for IC to ‘create wealth’, more in line with Bowman and Ambrosini’s (1998, p. 1) construct of “value capture” than ‘value creation’. In contemporary IC research, Dumay (2016, p. 169) critically redefines “value in four ways: monetary, utility, social, and sustainable value”, which is more in keeping with the contemporary emphasis on third stage performative IC (Guthrie et al., 2012) and the fourth stage ecosystem approach (Dumay and Garanina, 2013). Several chapters in this book use this contemporary conceptualization of value creation, and Chapter 2 goes beyond and discusses the worth, rather than the value of IC (Dumay et al., 2017).

What something is worth differs from its value, whether it be tangible or intangible. As a result, Dumay et al. (2017) outline the need for the fifth stage of IC research, to reframe the general research question of “What is IC worth to investors, customers, society and the environment?” to “Is managing IC a worthwhile endeavour?” Arguably, asking the latter question removes boundaries so that all manners of worth are included and recognizes that IC is a substantial part of what impacts everyone on a daily basis. There are still researchers who hold the view that IC and intangible assets are purely for creating wealth for investors and shareholders (Lev and Gu, 2016), while there is an opposite worldview that defines value creation as more encompassing and involving more stakeholders. Therefore, there is arguably a need to reconcile “the worth of IC to different people in different contexts and respecting that there will always be differences and that one view should not always prevail” (Dumay et al., 2017, p. xx).

p.3

Introduction to IC as per the chapters

In this section we will describe how we frame IC for the purpose of presenting the chapters in this book. For those unfamiliar with the different stages of IC research, we recommend that you begin reading some of the seminal articles that will help you understand the evolution of IC. These would include works such as Petty and Guthrie (2000) for first and second stage research, Guthrie et al. (2012) for third stage research, and Dumay and Garanina (2013) for third and fouth stage research. Finally Dumay et al. (2017) in this book, for the first time, introduce the fifth stage of IC research (see Figure 1.1). Additionally, the latter chapter gives a comprehensive chronological outline of the path IC research has taken since the early 1990s, which is key to understanding how IC has emerged from an interesting idea, to a more comprehensive field of research and practice. As such, we lead with this chapter to introduce a comprehensive view of IC, especially for readers unfamiliar with IC research, to allow them to quickly grasp what IC is, why IC is important, and its trajectory to the time we took on this project. Consequently, we then work backwards from fifth to first stage chapters, noting a dominance of chapters addressing third stage practice-based IC research.

p.4

Fifth stage chapters

In the first chapter of this section Dumay, Guthrie, and Rooney (2017) examine the path that critical IC research has followed from its conception until today and reflect on the possible future path for critical IC research. From the foundation of the four previously identified stages of research, the authors thus build a fifth, critical, research path for IC. In this fifth stage of IC research, IC researchers need to move beyond the boundaries of traditional, rather narrow, IC definitions, and instead of asking what IC is worth to various stakeholders, investors, customers, society, and the environment, instead ask whether managing IC is a worthwhile endeavour at all? Focusing on this big question helps recognize that IC is a substantial part of what impacts us on a day-to-day basis. In developing the fifth stage of research, there needs to be more research that focuses specifically on understanding how IC (or the various elements) helps improve value beyond organizational boundaries and, furthermore, that going beyond organizational boundaries also requires IC researchers to broaden their idea of IC.

The authors observe that the terms intangibles and IC are used synonymously, yet the term intangible assets is much broader than those assets that create an accounting financial value because it includes everything that is not tangible and put to use to ‘create value’. The authors argue that in all forms value creation somehow relies on interaction with tangible assets. Dumay et al. (2017) then explore the key strengths of the <IR> approach, which includes financial, physical, and natural capital in its value creation model (IIRC, 2013), something that many IC researchers are only just coming to apply. They argue that it is time to take down the boundaries to IC research and work towards reconciling the worth of IC to different people in different contexts, respecting that there will always be differences and that one view should not always prevail.

Similarly, Roslender and Monk (2017), in the chapter “Accounting for people”, go beyond recognized IC boundaries and address the consequences of progressing the challenge of accounting for people, a project that long predates the recognition of the significance of IC as an element within, but one which had largely become captured in past decades. Realizing the naivety of identifying a single aspect of the IC field as being the most significant, this chapter is founded on the premise of ‘taking people into account’, and links to fifth stage IC research by asking what IC is worth to various stakeholders, recognizing the importance of devoting further resources to the continued exploration of the IC field. First, this chapter provides an overview of the history of accounting for people, from its identification as a major challenge to the accountancy profession almost a century ago, through a series of general approaches to the task, and concluding with a discussion of human capital accounting. Second, the chapter provides a number of insights on three pathways that IC researchers interested in progressing accounting for people might pursue: employee health and wellbeing; a broader range of human rights issues; and the role for human capital self-accounting.

The authors argue that taking people into account has two different meanings. First, from an accounting perspective, it brings to mind the search for some means to incorporate people within accounts, most obviously by putting people on the balance sheet. The second meaning is of a much more practical nature, at least to anyone with an interest in people and what they bring to the workplace. This meaning for taking people into account translates into a commitment to demonstrate the scale and scope of what people gift to society, including as employees. This chapter argues that human capital is, by definition, the source of IC, as a consequence of which it demands to be taken into account more than ever, to ensure that its contribution to society is the most it can be, at all times and in all spaces.

p.5

Fourth stage chapters

Leif Edvinsson (2017) a founding father of IC in his chapter “Seven dimensions to address for intellectual capital and intangible assets navigation” provides an overview of the emerging global approaches to revealing the hidden value of both nations and enterprises, to the benefit of future generations, by identifying seven steps to address IC and intangible assets navigation. He argues that IC is about visibility, understanding, flow, networking of brain capacity, the velocity of the transformation of intangible human capital into more sustainability drivers of structural capital. The chapter contributes to the fourth stage of IC research. It is a paradigm in search of the drivers of value creation and reports to various stakeholders. In advanced economies, 75 per cent of GDP is related to IC. This chapter discusses the ELSS-Model that groups more than 60 countries over 15 years and covers the four traditional major pillars of national IC – human capital, relational capital, structural organizational capital, and renewal capital or innovation capital. It may also be refined to incorporate social capital and environmental capital dimensions.

Schiuma and Lerro (2017) in their chapter state that IC is playing a fundamental role in the development dynamics of regional economies. This chapter argues that there are two main issues. The first issue concerns the difficulty of identifying and measuring IC within regional systems. Despite the wide acknowledgement of IC as a key driver, there is still a lack of a coherent and shared framework for identifying, managing, assessing, and reporting IC at the regional level. Although there is quality and available data on different aspects of regional development, the second issue is that there is a lack of homogeneous and significant data about the use of IC. Their chapter contributes to the fourth stage of IC research, with its contribution in the way it addresses two issues. First, it analyses the role of IC and related components for regional development dynamics. Second, concerning territorial strategic resources, it presents the Knoware Tree, a framework to identify and classify territorial IC and the Knoware Dashboard, a framework driving the design of potential indicators and metrics to assess territorial IC.

Next the focus changes to IC and the public sector with Samkin and Schneider (2017) as their chapter reviews and critiques IC research undertaken in New Zealand. The identified research is positioned within the four stages of IC literature in order to answer the question: what has been the focus of IC research in a New Zealand context to date? The answer is that, despite New Zealand being heralded as a leader in public sector management following the reforms of the 1980s and 1990s, the extent and depth of research into how IC can be useful to the public sector to create public value is surprisingly limited. The majority of papers adopt a content analysis method using a disclosure index to determine the level of IC reporting in the annual reports of a sample set of organizations.

The authors state that the majority of the research identified has not moved beyond stage two IC research, which is concerned with guidelines and IC frameworks. In order to extend the frontiers of IC research beyond ‘what is’ into stage three research investigating IC in practice from a critical and performative perspective, and stage four research influenced by critical social and environmental accounting, a number of future research avenues are explored within the New Zealand public sector. Given a general acceptance of IC, understanding how the public sector views IC will become increasingly important. Additionally, how the public sector can leverage its IC in order to create value by providing better and more effective services provides several fruitful avenues of research.

The focus on the public sector continues with Vagnoni (2017) in her chapter “Intellectual capital in the context of healthcare organizations: Does it matter?” in which she states that healthcare organizations differ from others because of their fundamental mission to guarantee health protection to citizens and, therefore, their management process is driven by different criteria. Her point is that while many studies examine IC and management, regarding healthcare organizations IC is still a ‘black box’. Costs and financial results are identified, but how IC interacts to share knowledge and create innovation and value, is not known or monitored. Despite efforts to mobilize knowledge and innovation to legitimize healthcare organizations’ strategic role in society, the literature has devoted surprisingly limited attention to these IC dimensions. The chapter aims to fill this gap.

p.6

Vagnoni (2017) explores the literature and several examples to highlight that healthcare organizations are complex and IC has a particular role to play in their strategic management. In identifying IC variables, their relationships, and how to mobilize them, the chapter identifies the potential for IC to contribute to achieving financial goals as well as clinical outcomes and administration, thus contributing to the fourth stage of IC research. She states that medical journals have widely studied the IC framework and its operationalization in different dimensions, as well as criticizing the lack of methods and approaches to using IC for management and strategy effectively. Clinicians have emphasized the role of knowledge and IC for healthcare management, while directors of healthcare organizations are under pressure to manage budget constraints.

In conclusion, she argues that IC accounting scholars can play a vital role in bridging the gap...