The Currency Risk Management series offers readers, researchers, and financial professional a time-tested training tool for understanding and working in the increasingly complex currency markets. This series breaks new ground in simplicity, clarity, and ease of application in risk management practice.

International trade creates a need for buying, selling or borrowing foreign currencies. When, for example, an exporter in Japan sells goods to a customer in the US, the sale will be priced in yen, dollars, or perhaps a third currency such as sterling.

• If the sale is priced in yen, the customer will purchase yen with dollars in order to make the payment.

• If the sale price is in dollars, the Japanese supplier normally will wish to convert the receipts into his domestic currency, yen, and will sell dollars in exchange for yen.

• If the sale price is in a third currency, such as sterling, the customer will buy sterling in exchange for dollars to make the payment and the supplier will then sell the sterling in exchange for yen.

On occasion, international trade transactions do not result in the sale or purchase of foreign currency because companies either have foreign currency bank accounts for receipts and payments, or might pay for a purchase with a foreign currency bank loan.

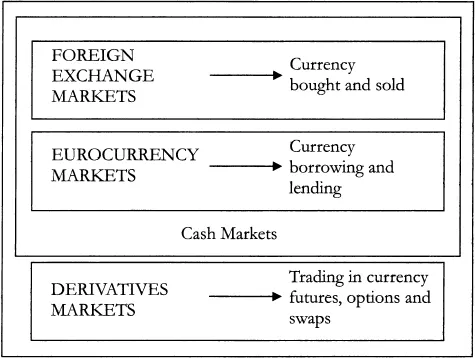

Buying and selling currencies, depositing foreign currency in a bank and currency borrowing and lending are all financial market activities that in turn support international trade.

Currency is bought and sold in foreign exchange markets that are commonly referred to as FX or y

Foreign currency lending and borrowing takes place in the eurocurrency markets. Together, the FX markets and the eurocurrency markets make up the foreign currency cash markets.

Currencies also are traded in other forms as derivative instruments, such as currency swaps, options and futures. These are more sophisticated instruments for trading in foreign currencies that are derived from an underlying foreign exchange market or eurocurrency market transaction, and were first devised during the 1970s.

The Currency Markets

Exchange Rates

The price at which one currency is traded in exchange for another in the FX markets is the exchange rate between the two currencies. In a free market these prices move up or down according to demand and supply, whereas in regulated markets exchange rates are controlled. FX markets for the major traded currencies are partially regulated to the extent that some governments try to stabilize the exchange rate for their domestic currency against other major currencies. For example, the government of a developing country might try to achieve a stable rate for its currency against the dollar.

To a large extent, however, the main FX markets are now fairly free from controls, and exchange rates between the major currencies, most notably the dollar, the yen and the euro, fluctuate freely according to demand and supply.

Currency Risk

Fluctuations or volatility in exchange rates cause currency risk.

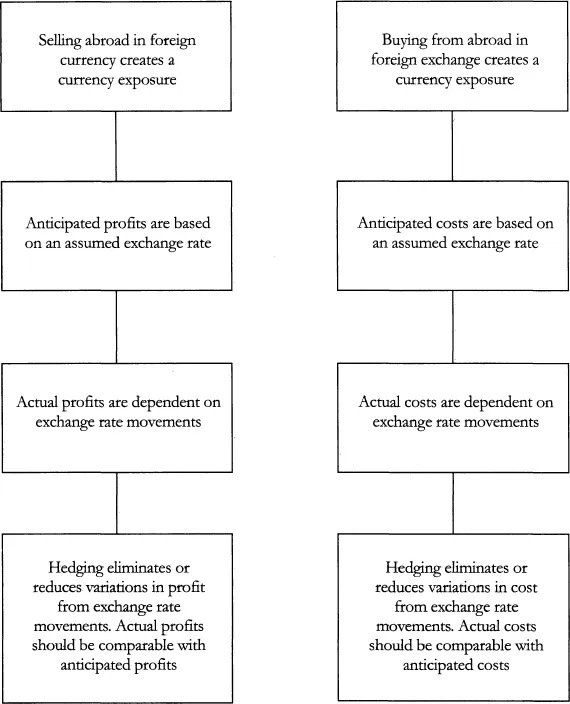

In brief, currency risk is the risk that adverse movements in exchange rates will reduce the anticipated income or increase the anticipated expenditure of any company that buys, sells, borrows or lends foreign currency. The size of a company’s exposure to currency risk depends on the volume of its income, expenditure, borrowing or lending in each currency.

For example, suppose that a UK company has spent £1 million on a contract to supply a US customer, and the contract price is

2 million. If the exchange rate is £1 =

1.60, the company can expect to sell its dollar receipts for £1.25 million and realize a profit of £250,000 on the contract when the customer eventually pays. Until payment is received, the company has an exposure of

2 million in receivables and it is at risk of a weakening of the dollar against sterling. When payment is received, the exchange rate might be £1 =

1.80, and the company’s income of

2 million would then be worth just £1.111 million. The anticipated profit of £250,000 will become a much lower profit of about £111,000.

The exchange rate could move favorably as well as adversely. If the exchange rate on receipt of the

2 million in this example were £1 =

1.50, the dollar revenue would be sold for £1.333 million to realize a profit on the contract of £333,000.

A key aspect of currency exposures is that although a company might wish to make a planned profit, or incur a certain cost, from its international selling or buying, currency exposures and exchange rate movements can put the plan at risk. Profits or losses can become more dependent on exchange rate changes than on the inherent profitability of the underlying trade in goods or services.

Currency risk is made much greater when exchange rate movements are potentially large and unpredictable. In other words, volatile exchange rates make currency risks more severe.

Hedging Currency Exposures

Exposures to currency risk can be reduced or even eliminated by hedging. The aim of hedging is to ensure, so far as is possible, that profits or costs are more predictable and thus less susceptible to exchange rate variability.

One commonly used instrument for hedging currency exposures is the forward exchange contract, a foreign exchange market transaction. The FX markets are not just a means of buying or selling currency, they also can be used to obtain protection against adverse future movements in exchange rates.

Currency Risk Management and Hedging

2

How FX Markets Are Structured

A foreign exchange transaction is a contract to buy or sell a quantity of one currency in exchange for another at a specified time for delivery and settlement, and at a specified price or rate of exchange. These transactions take place in the foreign exchange markets.

Origins of FX Markets

The origins of these markets lie in the execution of foreign exchange transactions for immediate value. Such transactions have taken place for several centuries, often with gold as an intermediary measure of value. Although the UK finally left the gold standard in 1931, the sterling/dollar rate remained fixed. An international system of fixed exchange rates with occasional realignments of currencies, known as the Bretton Woods Agreement, operated after World War II until 1971, when the US abandoned the gold standard. The pressures that forced the US action were also responsible for the progressive collapse of fixed exchange rates and the flotation of the major currencies in the early 1970s.

Once currencies were free to respond to changes in economic fundamentals by adjusting their relative values, a mechanism for executing large FX transactions became necessary. This was the creative stimulus behind the foreign exchange market that flourishes today.

Under the previous system of fixed rates with infrequent realignment of currencies, companies had few losses caused by an adverse currency movement. For example, a British company selling in the US in the 1950s knew that the dollar proceeds could be exchanged at a rate of about £1 =

4 when they were received weeks or months later. It was only when currencies started to float that losses due to adverse exchange rate movements became a problem that in turn demanded a solution.

The Market Place

Some financial markets have a physical center. Some futures markets, for example, have a trading floor where dealers meet to transact their trades. Most stock markets no longer have a trading floor, but they do have a hea...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Table of Contents

1 Introduction to the Foreign Exchange Markets

2 How FX Markets are Structured

3 Spot Transactions

4 Making a Spot Transaction

5 Practical Guidelines for Spot Transactions

6 Forward Exchange Contracts

7 Closeouts and Extensions

8 Swap Transactions and Short-dated Forward Transactions

9 Making a Forward Transaction

10 Practical Guidelines for Forward Transactions

Appendix: Currencies and their Liquidity

Glossary

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Foreign Exchange Markets by Alastair Graham in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.