People Risk Management provides unique depth to a topic that has garnered intense interest in recent years. Based on the latest thinking in corporate governance, behavioural economics, human resources and operational risk, people risk can be defined as the risk that people do not follow the organization's procedures, practices and/or rules, thus deviating from expected behaviour in a way that could damage the business's performance and reputation. From fraud to bad business decisions, illegal activity to lax corporate governance, people risk - often called conduct risk - presents a growing challenge in today's complex, dispersed business organizations.

Framed by corporate events and challenges and including case studies from the LIBOR rate scandal, the BP oil spill, Lehman Brothers, Royal Bank of Scotland and Enron, People Risk Management provides best-practice guidance to managing risks associated with the behaviour of both employees and those outside a company. It offers practical tools, real-world examples, solutions and insights into how to implement an effective people risk management framework within an organization.

eBook - ePub

People Risk Management

A Practical Approach to Managing the Human Factors That Could Harm Your Business

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

People Risk Management

A Practical Approach to Managing the Human Factors That Could Harm Your Business

About this book

04

Case studies in People Risk

A few lucky gambles can crown a reckless leader with a halo of prescience and boldness. DANIEL KAHNEMAN1

KEY MESSAGES

- People Risk events occur within organizations at multiple levels with varying likelihood of occurrence and unpredictable consequences when they do.

- People Risk events occur because of bad decisions arising from individual and group biases and conflicts of interest.

- People Risks are apparent at every level from a simple incident/accident to a whole industry.

- People use common rationalizations to explain their actions and mistakes.

4.1 Summary of cases

The cases described in this chapter are many but nonetheless are only a fraction of those that could be covered in this book. These cases were chosen because they cut across industries, countries and organizational types, although all involve large corporations. The losses run from the almost risible, such as the reputational damage in the HBOS statement case, to untold misery following the Global Financial Crisis. But they have one thing in common – they were caused by people, not natural events. They occurred on the frontline, such as in the BP Gulf of Mexico oil spill, and in the boardroom, such as the failure of RBS or the disastrous business strategies of Tesco and Lehman Brothers.

The cases also illustrate the fickleness of human nature, as corporate heroes are showered with praise one day only to be castigated as fools the next. But as Professor Barry Turner2 noted perceptively, disasters are rarely caused by one person no matter how senior, but instead are caused by the biases and inaction of many, who should have known and done better. The failure of one firm at one time may be passed off as merely due to bad management or, if generous, bad luck. However, massive losses in or even the collapse of so many hitherto successful organizations must raise the question, are there common factors in these cases and if so what are they? The answers lie deep within each one of us, particularly in our inability to see ourselves as being less than perfect. Humility not hubris is the key to averting such disasters.

Table 4.1 summarizes the cases discussed in this chapter using the 4Is Model described in section 4.1 below. It summarizes the losses incurred and describes the main rationalizations discussed in Chapter 3.

TABLE 4.1 People Risk – summary of case studies

| Case | Description | Losses | Rationalizations |

| INCIDENTS | |||

| HBOS – mistaken bank statement | Delivery of 75,000 statements | Reputation – embarrassment | Mistake – unknown operator |

| Air New Zealand – Flight 901 | Fatal air crash | 257 deaths | Miscommunication and lack of situational awareness |

| Medical fatality – Elaine Bromiley | Medical emergency | One death | Experts’ blind spots, and lack of situational awareness |

| INDIVIDUALS | |||

| Bank fraud – Ms Rajina Subramaniam | Fraud | AUD $40 million | Just Desserts – revenge for perceived abuse |

| Rogue trading – Barings, AIB, etc | Fraud | Various | Temporary Use – covering up for losses |

| Medical fatalities – Dr Harold Shipman | Patient murders | > 215 deaths | Unknown – possible addictive personality |

| Fraud – JPMorgan and Bernie Madoff | Failure to report fraud | US $2 billion fine | Distrust of Law |

| HBOS – banking fraud | Fraud | Unknown > £35 million | Economic Necessity, Just Desserts |

| Insider trading – Goldman Sachs | Fraud | £118 million | Distrust of Law and Victimless Crime |

| INSTITUTIONS | |||

| Royal Bank of Scotland | Strategic overreach | Acquired by UK Government | Ubiquity, Distrust of Law |

| Enron | Fraud – corporate | Bankruptcy | Distrust of Law, Victimless Crime |

| WorldCom | Fraud – corporate | Bankruptcy | Temporary Use, Distrust of Law |

| Washington Mutual | Bad lending | Bankruptcy | Ubiquity, Distrust of Law |

| HBOS | Bad lending | Acquired by Lloyds Bank | Ubiquity, Economic Necessity |

| Co-operative Bank | Strategic overreach | Acquired by Private Investors | Economic Necessity |

| JPMorgan – The Whale | Trading losses | US $6 billion | Economic Necessity, Distrust of Law |

| HSBC | Money laundering | US $1.9 billion fine | Ubiquity, Distrust of Law |

| Eli Lilly | Misselling drugs | US $1.4 billion fine | Distrust of Law, Victimless Crime |

| BAE Systems | Bribery | £280 million fine | Distrust of Law |

| Siemens AG | Bribery | US $1.3 billion fine | Distrust of Law |

| NHS – Mid Staffordshire | Excess deaths (unknown number) | Forced administration | Economic Necessity, Distrust of Law |

| RIM – Blackberry | Strategic overreach | Forced acquisition | Economic Necessity |

| Tesco plc | Strategic overreach | > £1 billion | Economic Necessity |

| Lehman Brothers | Strategic overreach | Bankruptcy | Economic Necessity, Ubiquity |

| BP – Gulf of Mexico oil spill | Death and pollution | US $4 billion ++ | Economic Necessity, Ubiquity, Distrust of Law |

| Fukushima nuclear plant | Nuclear accident | Unknown | Economic Necessity, Distrust of Law |

| INDUSTRY | |||

| Big Tobacco | Unsuitable products | Unknown | Ubiquity and Distrust of Law |

| New Zealand tax | Tax avoidance | NZ $2.5 billion | Ubiquity, Distrust of Law, Victimless Crime |

| PPI | Misselling products | £18 billion | Ubiquity, Distrust of Law, Victimless Crime |

| IRHP | Misselling products | £2.5 billion | Ubiquity Distrust of Law, Victimless Crime |

| Auto parts | Price fixing | US $2.5 billion fines | Ubiquity, Economic Necessity, Victimless Crime |

| LIBOR | Market manipulation | > US $4 billion fines | Ubiquity, Distrust of Law, Victimless Crime |

| Global Financial Crisis (GFC) | Misselling | US $6–14 trillion | Ubiquity, Distrust of Law, Victimless Crime |

4.2 The 4Is Model

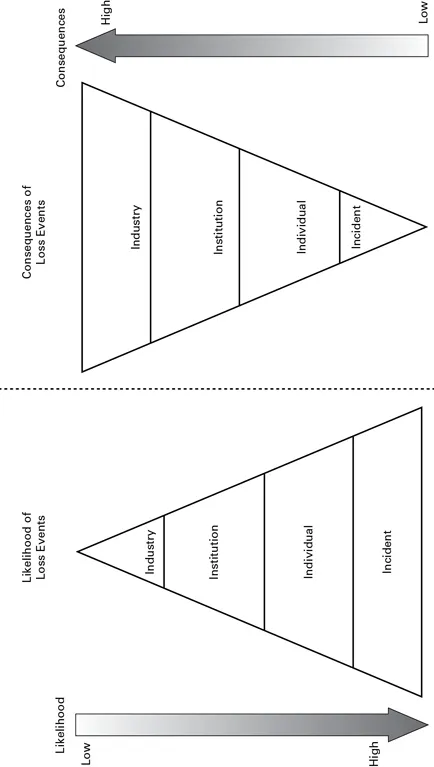

In considering fraud or errors, especially those that lead to serious losses, researchers tend to look to the organization or the system as the primary cause for disasters. It is not that they ignore the role of the individual but argue that on their own it is difficult for one individual or even a small group of individuals to cause a major loss or create a major disaster. While difficult, it is not, however, impossible and the higher and more entrenched an individual or small group of individuals are in an organization the greater the potential damage can be. It is true that there have to be pre-existing latent conditions3 that provide the opportunity for creating large losses. But in order to create a significant disaster it takes the power of thousands of individuals in multiple organizations or institutions across an industry. Figure 4.1 shows the 4Is model4 that juxtaposes the likelihood of losses occurring against the consequences if they do, at four different levels:

- Incident: in every business situation there will be many incidents that, as Frank Bird and others showed, are mainly ‘near-misses’ but can sometimes produce losses, including fatalities.

- Individual: in every business there may be many individuals who may perpetrate a fraud or make a serious error, but in general, management and financial controls in an organization/system and follow-up prosecution will tend to minimize but, unfortunately, not eliminate resulting losses.

- Institution: most institutions/firms will make losses from time to time but every now and then an institution will fail with disastrous consequence for shareholders, as with Enron, and even for the global economy as in the case of Lehman Brothers.

- Industry: it is at the level of an industry that the consequences of People Risk can be greatest, such as, for example, the costs to the shareholders of banks as a result of the PPI scandal in the UK.

FIGURE 4.1 The 4Is Model

In the 4Is model, it is at the level of an Industry that the greatest losses do occur. For example, US economists Tim Curry and Lynn Shibut,5 have estimated that the Savings and Loan (S&L) crisis of the 1980s cost the US taxpayer at least $150 billion. The term S&L refers to the many thousands of small banks that provided basic lending and savings services to local customers and dominated the US banking system until massive consolidation of the system in the 1990s as a result of this S&L crisis. Before and just after the Second World War, S&Ls were an integral part of life in the United States as typified by the fictitious Bailey Building and Loan Association in the classic film6 It’s a Wonderful Life, which showed what could happen if such a trusted institution were to fail. The S&L crisis was precipitated by changes in the late 1970s in the laws that deregulated the so-called ‘thrift’ industry, in effect giving S&Ls the same privileges as banks but without the same levels of regulation.

In terms of Turner’s model, introduced in Chapter 2, the ‘Precipitating Event’ for the S&L disaster was a series of interest rate rises engineered by the US Federal Reserve to dampen inflation in the US economy. These rises meant that S&Ls, which tended to give out fixed rate mortgages, were suddenly faced with increased funding requirements. In effect, like several banks that failed in the GFC, their assets did not match their liabilities and many S&Ls failed. But the losses were compounded by the fact that, freed by the new regulations, the boards of several large S&Ls had been lending recklessly, chasing profits and, for some, personal gain whereas previously they had sought safety and security. In some S&Ls there had also been rampant fraud, particularly control frauds where creative accounting was used by individuals to deceive shareholders into believing that an S&L was solvent when, in fact, it wasn’t.

In the same way that Bird, Cressey, Perrow and Turner argued, as described in Chapter 2, that one must look beyond individuals to organizations as the source of mistakes, errors and frauds, one must also look beyond Institutions to the Industry as the source of potentially even larger losses. This chapter is organized in line with the 4Is model and describes case studies of loss events at each level starting from the bottom – Incidents. Many, but not all of the cases are taken from the financial services industry, which is the one in which major financial losses have occurred in the last decade. Importantly, unlike other private corporations, firms in the financial services industry are highly regulated and therefore exceptional events tend to be the subject of intensive inquiry, analysis and opportunities for learning. It should also be noted that within each section the cases are o...

Table of contents

- Cover page

- Title page

- Imprint

- Table of contents

- Figures and tables list

- Dedication

- 01 People Risk in context

- 02 Definition and models of People Risk

- 03 The human dimension of People Risk

- 04 Case studies in People Risk

- 05 People Risk Management Framework

- 06 People Risk in the boardroom

- 07 The influence of organizational culture

- 08 Roles and responsibilities

- 09 Improving decision-making

- 10 Personal responsibility

- 11 Conclusion

- Glossary of terms and abbreviations

- References

- Index

- Full imprint

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access People Risk Management by Keith Blacker,Patrick McConnell in PDF and/or ePUB format, as well as other popular books in Business & Insurance. We have over 1.5 million books available in our catalogue for you to explore.