International trade, and its financing, is now a key component of many undergraduate and postgraduate qualifications. For anyone involved in international sales, finance, shipping and administration, or for those studying for academic or professional qualifications in international trade, The Handbook of International Trade and Finance offers an extensive and topical explanation of the key finance areas. This essential reference resource provides the information necessary to help you to reduce risks and improve cash flow, identify the most competitive finance alternatives, structure the best payment terms, and minimize finance and transaction costs.

This fully revised and updated 4th edition of The Handbook of International Trade and Finance also describes the negotiating process from the perspectives of both the buyer and the seller, providing valuable insight into the complete financing process, and covering key topics such as: trade risks and risk assessment; structured trade finance; methods and terms of payment; currency risk management and bonds, guarantees and standby letters of credit.

The Handbook of International Trade and Finance provides a complete and thorough assessment of all the issues involved in constructing, financing and completing a cross-border transaction, as an indispensable guide for anyone dealing with international trade. The new edition also includes a section on risk management, which plays an increasingly important role in international trade from currency fluctuations to political risk and natural disasters.

N.B. This covers the principles of international trade and finance that are common across the globe and is relevant to anyone wanting to understand the subject, wherever they are located. Specific national issues (such as the UK's Brexit decision) do not affect the content. Online supporting resources include PowerPoint lecture slides.

eBook - ePub

The Handbook of International Trade and Finance

The Complete Guide for International Sales, Finance, Shipping and Administration

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Handbook of International Trade and Finance

The Complete Guide for International Sales, Finance, Shipping and Administration

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

02

Methods of payment

Different methods of payment

The method of payment determines how payment is going to be made, ie the obligations that rest with both buyer and seller in relation to monetary settlement. However, the method of payment also determines – directly or indirectly – the role the banks will have in that settlement.

Methods of payment and terms of payment

These two expressions are sometimes used synonymously, but in this book they have been kept separate.

‘Methods of payment’ represents the defined form of how the payment shall be made, ie on open account payment terms through a bank transfer, or through documentary collection or letter of credit.

‘Terms of payment’ defines the detailed obligations of both commercial parties in relation to the payment, not only the form of payment and when and where this payment shall be made by the buyer, but also the obligations of the seller: to deliver according to the contract and, for example, to arrange stipulated guarantees or other undertakings prior to or after delivery.

As this chapter mainly deals with the different methods of payment, this distinction should be kept in mind – terms of payment will be discussed in Chapter 8.

Methods of payment can be categorized in different ways, depending on the purpose. This is often based on the commercial aspect seen from the exporter’s perspective in terms of security. In security order, the basic methods of payment could then be listed as follows:

- cash in advance before delivery;

- letter of credit (L/C);

- documentary collection;

- bank transfer (based on open account trading terms);

- other payment or settlement procedures, such as barter or counter-trade.

However, as can be seen in the following text, the security aspect is usually not that simple to define in advance. In reality, there are many different variations and alternatives that will affect the order of such a listing; for example, if the open account is supported by a guarantee, a standby L/C or separate credit insurance, or how a barter or counter-trade is structured. Even the nature and wording of the letter of credit will eventually determine what level of security it offers the seller.

Seen from a more practical point of view of how the payment is actually executed, and the involvement of the commercial parties and the banks, there are, in principle, only four basic methods of payment that are used today in connection with monetary settlement of international trade (apart from e-commerce and barter and counter-trade transactions, which are described later on in this chapter). One of these methods is always the basis for the terms of payment:

- bank transfer (also often called bank remittance);

- cheque payment;

- documentary collection (also called bank collection);

- letter of credit (also called documentary credit).

Table 2.1 illustrates the most important aspects of the obligations that the buyer and seller have to fulfil in each case. In reality things are often a bit more complex, particularly when it comes to the documentary methods of payment, which have many different alternatives. For example, there is complexity in handling, speed in execution and level of costs and fees, but the most important factor is the difference in security they offer. This aspect is thoroughly dealt with in this chapter.

Table 2.1 Summary of the different payment methods

| The role of commercial parties | The role of banks | ||||

| Method of payment | Seller’s obligations | Buyer’s obligations | Money transfer | Document handling | Payment guarantee |

| Bank transfer1 | Sending an invoice to the buyer after delivery | Arranging for payment according to the invoice | X | ||

| Payment by cheque1 | Same as above | Arranging for a cheque to be sent to the seller | X | ||

| Documentary collection | After delivery, having the agreed documents sent to the buyer’s bank | Pay/accept at the bank against the documents presented | X | X | |

| Letter of credit | After delivery, presenting conforming documents to the bank | To have the letter of credit issued according to contract | X | X | X |

1 Bank transfers and bank cheques are often referred to as ‘clean payments’, in comparison with documentary payments (collections and letters of credit).

Bank charges and other costs

The costs of the different alternatives are mainly governed by what function the banks will have in connection with the execution of payment. Other forms of fees, which can have an indirect connection to the payment, do sometimes arise, such as different charges related to the creation of the underlying documents, for example consular fees and stamp duties. However, such fees are related more to the delivery than to the payment and are normally borne by the party that has to produce these documents according to the terms of delivery. Other costs, such as payment of duties and taxes, are also governed by the agreed terms of delivery.

Bank charges will arise not only in the seller’s but also in the buyer’s country; they can vary hugely between different countries, both in size and, more importantly, in structure. In some cases they are charged at a fixed rate, in others as a percentage of the transferred amount. Sometimes they are negotiable, sometimes not, and these differences occur not only between countries but also between banks.

The best solution for both parties is often to agree to pay the bank charges in their respective country, but whatever the agreement, it should be included in the sales contract. Such a deal would probably minimize the total costs of the transaction since each party would have a direct interest in negotiating these costs with their local bank. Bank charges in one’s own country are more easily calculated and, even if the difference between banks in the same country may be relatively small, they are often negotiable for larger amounts.

Bank charges are often divided into the following groups:

- standard fees for specified services – normally charged at a flat rate;

- payment charges – normally charged at a flat fee or in some cases as a percentage of the amount paid;

- handling charges, ie for checking of documents – normally charged as a percentage on the underlying value of the transaction;

- risk commissions, ie the issuing of guarantees and confirmation of letters of credit – normally charged as a percentage of the amount at a rate according to the estimated risk and the period of time.

Detailed fee schedules, applicable in each country and for each major bank, can easily be obtained directly from the banks or found on their websites, but as pointed out earlier, for larger transactions, fees, charges and commissions are often negotiable.

Bank transfer (bank remittance)

Most trade transactions, particularly in regional international trade, are based on so-called ‘open account’ payment terms. This means that the seller delivers goods or services to the buyer without receiving cash, a bill of exchange or any other legally binding and enforceable undertaking at the time of delivery, and the buyer is expected to pay according to the terms of the sales contract and the seller’s later invoice. Therefore the open account involves a form of short, but agreed, credit extended to the buyer, in most cases verified only by the invoice and the specified date of payment therein, together with copies of the relevant shipping or delivery document, verifying shipment and shipment date.

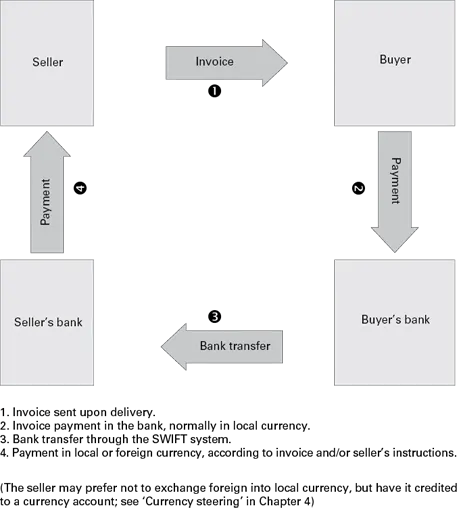

When the terms of payment are based on open account terms and the seller receives no additional security for the buyer’s payment obligations, the normal bank transfer is by far the simplest and most common form of payment. The buyer, having received the seller’s invoice, simply instructs their bank to transfer the amount, a few days before the due date, to a bank chosen by the seller. This can be done either directly to the seller’s account at a bank in their country (which is the most common) or to a separate collection account that the seller may have at a bank in the buyer’s country (see Figure 2.1.)

Figure 2.1 Bank transfer (bank remittance)

Payment structure follows the trade pattern

Bank transfers are a method of ‘clean payments’ (as compared with documentary payments, to be described later), which pr...

Table of contents

- Cover

- About this book

- Title Page

- Contents

- Preface

- Introduction

- 01 Trade risks and risk assessment

- 02 Methods of payment

- 03 Bonds, guarantees and standby letters of credit

- 04 Currency risk management

- 05 Export credit insurance

- 06 Trade finance

- 07 Structured trade finance

- 08 Terms of payment

- 09 The export quotation

- Appendix I: Electronic documents in international trade

- Appendix II: International transport documents

- Glossary of terms and abbreviations

- Index

- Copyright

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Handbook of International Trade and Finance by Anders Grath in PDF and/or ePUB format, as well as other popular books in Business & Insurance. We have over 1.5 million books available in our catalogue for you to explore.