![]()

1 The Finance Department

What it does and how it fits into an airline’s organisation

Before explaining the details of the department, it is important to make clear that there is no one ideal way of organising an airline’s accounting and finance functions, as each airline will have its own preferences for the way its management is organised and responsibilities are allocated. Many airlines combine the accounting and finance operations into one department under the leadership of one person, typically titled Finance Director or Chief Financial Officer (CFO), who is usually, but not always, a member of the Board of Directors. A combined department, i.e., accounting and finance, is a popular option and, in this book, references to ‘Finance Department’ assume a combined department.

The role of the Finance Department

The Finance Department provides services to the whole airline. The basic services are recording and reporting financial information and managing the airline’s financial position. The financial information held by the Finance Department and the reports issued, both routine and ad hoc, help managers record progress towards meeting the airline’s objectives and to make decisions which are consistent with those objectives. Information is a resource. Imagine that the data sent to the Finance Department is its raw material and the reports they issue are its finished product. The real trick is for the reports to provide the right numbers accurately for managers, and this requires co-operation and communication between the Finance Department and all other departments. Within the airline there should be regular reviews of all routine reports, including those issued by the Finance Department. The review should cover whether the reports are still needed, and their content and layout, the frequency of issues and how quickly after a period end they are issued. Circumstances change, and it is important that all reports, not only financial reports, are relevant and help managers do their jobs. There isn’t a part of an airline that is not touched by finance. The financial information held in the Finance Department’s records is a resource for the whole airline.

Organisation and responsibilities of a Finance Department

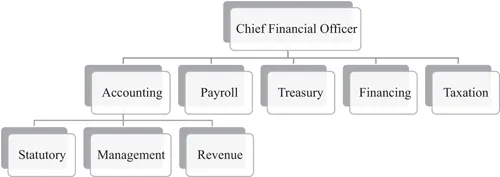

A Finance Department can be organised in different ways and the structure depends on the airline’s management approach (see Figure 1.1). A traditional organisation is to have a separate section for each of the major operations of the department; in this book, the most common titles of each section have been used, but they may differ by airline.

Figure 1.1 Finance Department’s functions

With this approach the responsibilities of the typical sections are:

- Statutory Accounting: production of the financial reports required by law; these are discussed in Chapter 8. Included under this heading is the keeping of a record of all the airline’s tangible and intangible assets, the original cost, the cost of any additions or modifications, an estimate of the assets’ useful life in the airline and its overall useful life, together with a periodic assessment of the current value and some means of identification. The estimates and assessments should be reviewed regularly.

- Management Accounting: producing reports for the airline’s management, budgets, forecasts and actual results; this is the area where most operating staff have contact with the department and are most likely to use the information provided.

- Revenue Accounting: recording the airline’s actual revenue; this work can be quite simple or very complex depending on the airline’s business model. The simplest records are for an airline that only operates within one country:

- with all its tickets sold on its own website

- passengers paying in advance

- does not make refunds if tickets are not used

- its tickets are only to be used on its own flights.

In this case, the records only need to identify the passenger, the flight and the amount paid. The amount received in advance will be recorded in an account named something like ‘Unearned Transportation Revenue’. When the passenger travels, the amount received from the passenger will be transferred from the ‘Unearned Transportation Revenue’ account to the airline’s ‘Profit and Loss’ account as revenue.

Generally, the more options and services an airline offers, the more complicated the revenue records become; if, for example, in addition to the services offered in the example above, the airline: - sells its tickets through its own offices, travel agencies in different countries, as well as through its own website

- issues tickets which may include flights on other airlines

- accepts another airline’s tickets on its flights

- permits refunds of unused tickets

- offers packages which include a flight and hotel stay, with or without tours.

The records become very complicated, more records are needed and there are calculations for such things as the proportion of a partly used ticket which should be refunded. The accounting effort required by the more complicated business model is significantly larger than for the ‘simple’ one.

The accounting for revenue can be further complicated if the airline has a Loyalty programme, particularly if the airline ‘sells’ miles to other service suppliers (e.g., car rental companies). The amounts involved in Loyalty programmes can be very substantial and many programmes have been transferred into separate operating companies.

Revenue records are usually kept on the airline’s computer records.

- Payroll: calculating and arranging payment of staff salaries; frequently this section is located in a separate area due to privacy concerns.

- Treasury: managing and forecasting the ‘cash-flow’, which is the money received and paid out. This is an important area because the company is required to be ‘solvent’; that is, able to pay its debts when they become due. Managing an airline’s cash-flow is an important topic involving many operations, including such matters as investing surplus funds overnight and, in the longer term, also handling the airline’s foreign currency position. This is discussed in Chapter 6.

- Financing: managing the airline’s financial position; that is, its borrowings and financial risks. These are discussed in detail in Chapter 4.

- Taxation, preparing all ‘tax returns’, i.e., the calculation of any taxes due to be paid or refunded; an airline’s tax position can be complicated if taxes are payable in many countries. The airline’s foreign tax position in a foreign country may be simplified if a Treaty for the Avoidance of Double Taxation, often referred to as ‘Double Tax Treaty/Agreement’ or ‘DTA’ exists between the two countries, but all foreign taxes need to be monitored.

These are the basics, and it may be that the Finance Department will be asked to take on other responsibilities, such as negotiating and dealing with insurance matters or issuing invoices for non-travel income, e.g., aircraft handling.

On the surface it may seem that some of these operations, like paying suppliers, would be better done within the various operating departments in the airline. In general, the reason for splitting the responsibility for some processes (e.g., making payments) between different departments is part of the company’s system of ‘checks and balances’ (i.e., splitting a responsibility reduces the chances of fraud). The operating department is responsible for reviewing, checking and approving each supplier’s invoice and the Finance Department will check that the invoice has been correctly approved before arranging payment.

Location of the finance staff

A Finance Department provides services to all parts of an organisation. The department may be ‘centralised’, i.e., all sections are located together, or ‘decentralised’, or a combination of both. A popular option is locating part of the finance team with the major operating departments. This has the advantages of improving communication and understanding between departments and the finance staff. A possible disadvantage is that the co-operation can reduce the effectiveness of the airline’s checks and balances. Also, the finance staff may feel isolated from the main Finance Department. The latter problem can be overcome by good communication between the departmental finance team and the corporate finance team. It is not unusual in the real world for the Finance Department’s staff to be partly decentralised to one or two large departments (e.g., Engineering) and partly centralised, depending on the preference of the operating department’s manager. Even if the department is decentralised completely or just to some extent, the staff are still part of the Finance Department, which remains responsible for the quality of work, discipline and remuneration.

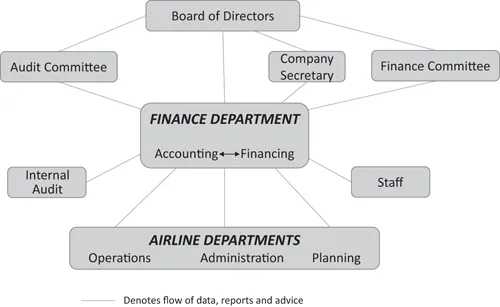

Operating structure

The Finance Department has dealings with many parts of an airline’s operation. Figure 1.2 presents a diagrammatic overview of these internal connections.

Figure 1.2 Connections inside the airline

The Finance Director or CFO usually reports to the Chief Executive Officer, or whatever the senior operating position in the company is titled, but in some cases they may report to an Executive Chairman. In addition, there are two sub-committees of the Board of Directors which influence the work of the Finance Department. These are the Audit Committee and Finance Committee.

Audit Committee

Although having an Audit Committee is not a legal requirement in every country, it is recommended as part of good ‘Corporate Governance’, which concerns the overall management of a company. If it is a legal requirement, the law will define the committee’s duties. If the airline’s shares are quoted on a stock exchange (i.e., it is a ‘Public Company’), it is almost certain that a stock exchange will require the company to have an Audit Committee. The Board of Directors has the power to allocate additional duties to this sub-committee as it sees fit. The usual duties of the Audit Committee are to:

- Establish that the company’s accounting policies are appropriate; these will be discussed in Chapter 8.

- Ensure the company’s financial reporting is complete and complies with current ‘Reporting Standards’; these are national (or international) accounting and reporting standards applicable to all companies.

- Monitor the airline’s ‘internal controls’, which are the systems designed to prevent fraud.

- Ensure compliance with the airline’s financial policies (e.g., regarding the treatment of Debtors and Creditors).

- Identify and monitor the ways the airline’s risks are managed.

- Choose and monitor the performance of the ‘External Auditors’, who are independent accountants employed to review and confirm the accuracy of the airline’s ‘Statutory Reports’ (i.e., the reports required by law; these are further discussed in Chapter 8).

- Monitor the performance, work plan and reports of the airline’s ‘Internal Audit Department’; this is a separate department responsible for checking the accuracy and efficiency of the company’s systems.

The members of the Audit Committee should all be ‘Independent Non-Executive Directors’ (i.e., directors whose only connection with the company is their directorship).

Finance Committee

A Finance Committee is not currently required by law, but most large companies and airlines have one to help manage the company’s financial position. Its duties are allocated and agreed by the Board of Directors. Hence...