![]()

Chapter 1

Introduction

Airports are an essential part of the air transport system. They provide the entire infrastructure needed to enable passengers and freight to transfer from surface modes of transport to air modes of transport and to allow airlines to take off and land. The basic airport infrastructure consists of runways, taxiways, apron space, gates, passenger and freight terminals, and ground transport interchanges. Airports bring together a wide range of facilities and services to fulfil their role within the air transport industry. These services include air traffic control, security, fire and rescue in the airfield. Handling facilities are provided so that passengers, their baggage, and freight can be successfully transferred between aircraft and terminals, and processed within the terminal. Airports also offer a wide variety of commercial facilities ranging from shops and restaurants to hotels, conference services, and business parks.

Apart from playing a crucial role within the air transport sector, airports are of strategic importance to the regions they serve. In a number of countries they are increasingly becoming integrated within the overall transport system by establishing links to high-speed rail and key road networks. Airports can bring greater wealth, provide substantial employment opportunities and encourage economic development – these factors can be a lifeline to isolated communities. However, they do have a very significant effect, both on the environment in which they are located and on the quality of life of the residents living nearby. A growing awareness of general environmental issues has heightened the environmental concerns about airports.

The focus of this book is on management issues faced by airport operators. The performance of these operators varies considerably depending on their ownership, management structure and style, degree of autonomy and funding. Typically, the actual airport operators themselves provide only a small proportion of an airport’s facilities and services; airlines, handling agents, government bodies, concessionaires, and other specialist organizations undertake the rest of the activities. The way in which operators choose to provide the diverse range of airport facilities has a major impact on their economic and operational performance and on the relationship with their customers.

Thus airport operators will each have a unique identity – but all have to assume overall control and responsibility at the airport. Each airport operator faces the challenging task of co-ordinating all the services to enable the airport system to work efficiently. The service providers are just some of the airport stakeholders, which operators need to consider; others include shareholders, airport users, employees, local residents, environmental lobbyists, and government bodies. A complex situation exists with many of these groups having different interests and possibly holding conflicting views about the strategic role of the airport. All the stakeholder relationships are important but, clearly, the development of a good relationship with the airlines is critical, as ultimately this will largely determine the air services on offer at the airport.

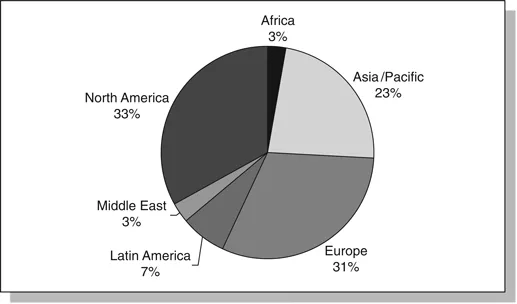

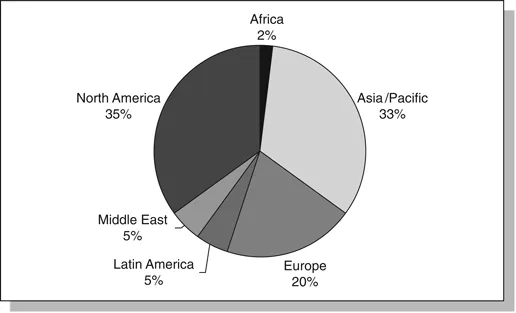

Globally, the airport industry is dominated by North America and Europe in terms of passenger numbers and North America and Asia Pacific in terms of cargo tonnes carried (Figure 1.1). According to the Airports Council International (ACI), North American airports handled 1579 million passengers in 2007, which represented 33 per cent of the total 4645 million passengers around the world. There were 1450 million passengers in Europe, accounting for a further 31 per cent of the total air traffic. As regards air cargo, North America is again the largest market with 32 million tonnes of the global 88 million tonnes representing a market share of 35 per cent (Figure 1.2). Asian Pacific airports have the second highest volume of air cargo with a global share of 33 per cent, reflecting the importance of this area in the global economy.

Figure 1.1

Airport passengers by world region, 2007

Source: ACI.

Figure 1.2

Airport cargo tonnes by world region, 2007

Source: ACI.

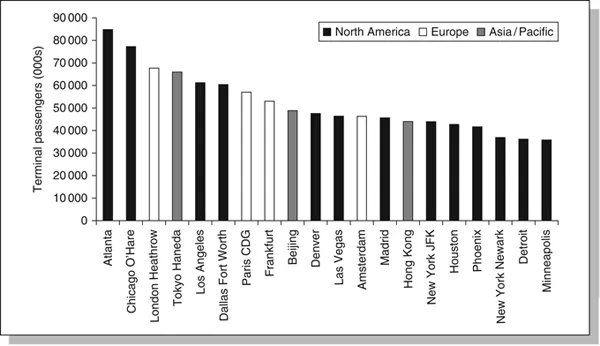

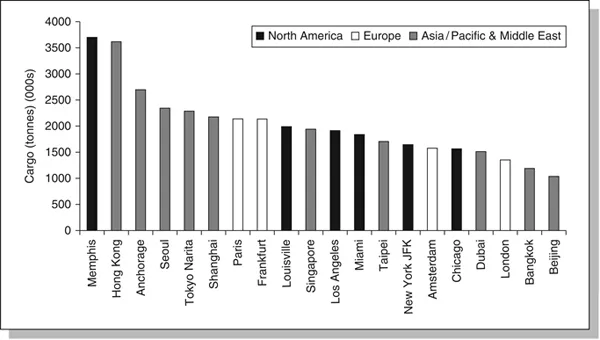

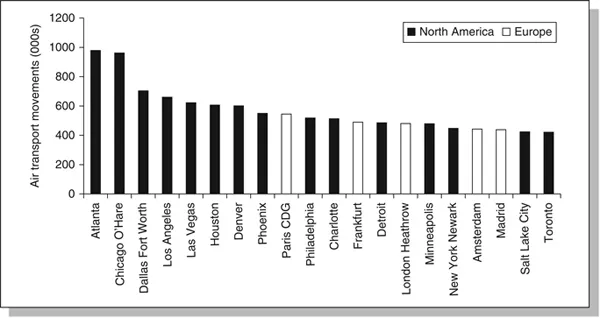

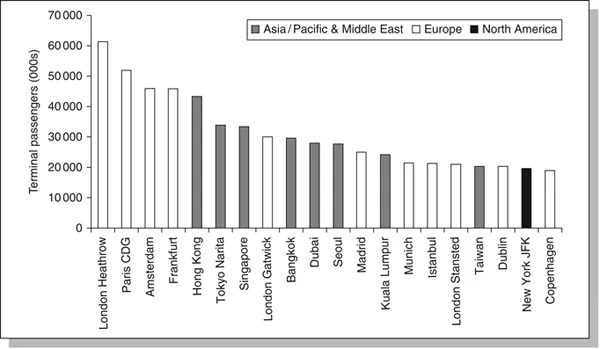

The importance of the North American region is reflected in the individual traffic figures of the various airports. For example, out of the 20 largest global airports, 13 are US airports in terms of passenger numbers, 6 in terms of cargo and 14 when air transport movements are being considered (Figures 1.3–1.5). North American airports tend to have a comparatively high number of air traffic movements since the average size of an aircraft tends to be smaller because of competitive pressures and the dominance of domestic traffic. However, when just international air traffic is being examined, the European region’s significance becomes much more important (Figure 1.6). Heathrow has the most international air traffic, whereas Atlanta and Chicago have the largest passenger throughput. The largest passenger airport in the Asia Pacific region is Tokyo Haneda, which is dominated by domestic traffic.

Figure 1.3

The world’s 20 largest airports by total passengers, 2006

Source: ACI.

Figure 1.4

The world’s 20 largest airports by cargo tonnes, 2006

Source: ACI.

Figure 1.5

The world’s 20 largest airports by aircraft movements, 2006

Source: ACI.

Figure 1.6

The world’s 20 largest airports by international terminal passengers, 2006

Source: ACI.

Not all the major cargo airports coincide with the major passenger airports. Memphis is the world’s largest cargo airport because Federal Express is based here. Similarly, UPS has its base at Louisville. The air cargo market is the largest in the Asia Pacific region where 9 out of the 20 largest cargo airports are situated. The larger than average aircraft size in Asia (from where the majority of orders for the new very large A380 aircraft are coming) means than none of the busiest airports in terms of movements are situated in this region. Dubai airport also makes it into the top 20 airports when cargo is being considered. All the other airports, whether measured in passengers or cargo, are in North America, Europe, or Asia Pacific with none in any other global region.

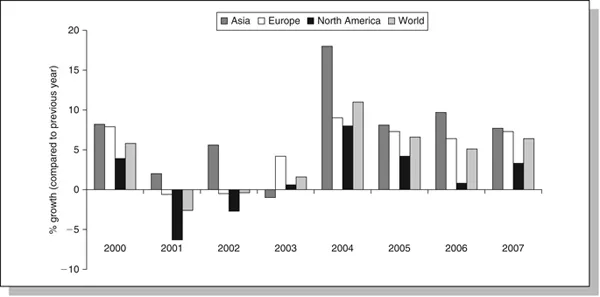

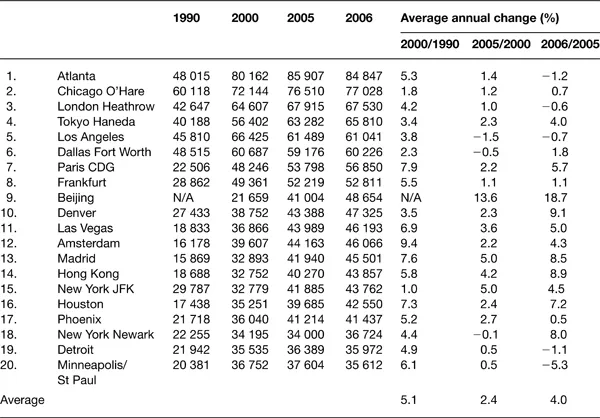

The aviation industry has been growing virtually continuously since the Second World War with periodic fluctuations because of economic recessions or other external factors such as the Gulf War in 1991. However this growth was dramatically halted recently due to the events of 9/11 combined with a global economic downturn. Since then the airport industry has experienced a number of volatile years with further events such as the Iraq war and the outbreaks of SARS in 2003. These events have had different impacts in different regions of the world as illustrated by Figure 1.7 which shows the devastating effect of 9/11 on North American airports and also the very significant influence which SARS had on Asian Pacific air traffic. Table 1.1 shows the growth of passenger number at the major airports of the world since 1990. The average annual growth was 5.1 per cent in the 1990s but was only 2.4 per cent between 2000 and 2005 as airports recovered from these various events. In recent years the market share of US airports has decreased whereas it has risen in the Asia Pacific. This increase in importance of the Asia Pacific region within the global aviation environment seems set to continue, with, for example, very much higher than average growth rates being experienced in India and China.

Figure 1.7

Airport passenger growth by main region, 2000–2007

Source: ACI.

Table 1.1 Growth in passenger numbers at the world’s 20 largest airports 1990–2006

The growth in demand for air transport has had very significant economic and environmental consequences for both the airline and the airport industries. Moreover, since the 1970s there have been major regulatory and structural developments, which have dramatically affected the way in which the two industries operate. Initially, most changes were experienced within the airline sector as a consequence of airline deregulation, privatization and globalization trends. The pace of change was slower in the airport industry, but now this sector, too, is developing into a fundamentally different business. The trend towards airline deregulation began in 1978 with the deregulation of the US domestic market. Many more markets have been subsequently liberalized or deregulated initially as the result of the adoption of more liberal bilateral air service agreements. In the European Union (EU), deregulation was achieved with a multilateral policy, which evolved over a number of years with the introduction of three deregulation packages, in 1987, 1990 and 1993. The 1993 package, which did not become fully operational until 1997, was the most significant package and has had the most far-reaching impact. This European deregulation has allowed a large low-cost airline industry to develop, which has had major consequences for many airports. This deregulation trend has continued in other parts of the world which in turn has encouraged more low-cost airline development. A very significant milestone here is likely to be the adoption of the EU-US open aviation area in 2008.

At the same time as the airline industry has been deregulated, airline ownership patterns have also changed. Most airlines, with the notable exception of those in the United States, were traditionally state owned and often subsidized by their government owners. However, this situation has substantially changed as an increasing number of governments have opted for partial or total private sector airline ownership, primarily to reduce the burden on public sector expenditure and to encourage greater operating efficiency. The other most significant development within the airline industry, partly due to deregulation and privatization trends, is the globalization of the industry and the emergence of transnational airlines. Three major alliance groupings, namely Star, oneworld, and Sky Team, have emerged with global networks. These alliance groupings are dominating the airline business – accounting for over half of all air traffic. Also airline mergers are occurring, for example, with Air France and KLM and with Lu...