- 400 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Strategic Human Capital Management

About this book

Strategic human capital management (HCM) is not just a measurement focused approach to human resource management (HRM). It is certainly not a decision science in which people can be managed as a result of quantitative analysis and financial valuation. In fact, it is probably more of an art than a science and is a way of leading people to unlock great business performance. Strategic HCM focuses all people management and development practices on maximizing the capability and engagement of the people working for an organization to create valuable intangible capability, human capital, which enables the organisation to take full advantage of potential business opportunities. Unlike HRM which focuses on getting closer and closer to the business, strategic HCM draws its energy from people, from their individual strengths, interests and motivations, which, aligned with long-term business strategy, can increasingly provide the main basis for differentiation and competitive advantage. However, the perspective also recognizes that measurement is important, and the book outlines an approach to measurement which recognizes the importance of knowledge, complexity, best fit and intangibility. Pulling together seemingly disparate strands of thinking, the book calls for a paradigm change in which people really are seen as an organisation's most important asset, and are managed in a way that reflects this fact. The text includes case studies from leading private and public sector organizations and commentary from HR practitioners and academics.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Part 1

Creating Value in HCM

1

Accounting for People

Introduction

Reader: ‘Why are you starting the book with Accounting for People, particularly if, given your points in the Preface, you don’t think the taskforce really dealt with ‘HCM’?’

Author: ‘I think I had to really. Accounting for People has played a key role in shaping the HCM agenda within the UK, and it deals with issues that are being discussed within other countries too. So I think, whether or not you are from the UK, that you may need a short recap or reminder of the work of the taskforce, in order to understand the context of some of the comments which are made later on. However, I certainly don’t dwell on this, and avoid entering the whole debate on Accounting for People versus the Operating and Financial Review (OFR) versus the Business Review. Not that I don’t have views on this, but I think that time has moved on.

The other reason for starting with Accounting for People is that it does open up an interesting discussion about the nature of value in HCM and the way this value can best be measured and described. Most of the chapter focuses on this…’

The other reason for starting with Accounting for People is that it does open up an interesting discussion about the nature of value in HCM and the way this value can best be measured and described. Most of the chapter focuses on this…’

The Accounting for People Taskforce

The UK’s Accounting for People taskforce was asked to recommend ways in which organizations could measure and report on the quality and effectiveness of their HCM practices and to identify the most helpful performance measures to include in HCM reports. One of the obvious opportunities for reporting was expected to be the updated Operating and Financial Review (OFR) that had been announced in the white paper Modernizing Company Law (Department of Trade and Industry, 2002). This white paper addressed the need to improve company reporting, recognizing that increasing complexity means that financial statements no longer provide the strategic information that investors need. The white paper stated that:

The Government agrees that companies should provide more qualitative and forward-looking reporting … It recognizes that companies are increasingly reliant on intangible assets such as: the skills and knowledge of their employees, their business relationships and their reputation. Information about future plans, opportunities, risks and strategies is just as important to users of financial reports as a historical view of performance.

Denise Kingsmill (2003a), who chaired the Accounting for People taskforce, described the problem she had set out to solve:

If talented workers –– which a company spends time and money employing and training –– are not managed properly, they will leave. Often falling straight into the welcoming arms of the competition, with potentially devastating effects. Organizations then have to spend further time and money on recruiting replacements. As an investor, the chances are you will not be aware that this has happened. You won’t have any means of judging the impact, good or bad, that the business’s human capital management has had on performance.

The taskforce’s definition of human capital was ‘the relevant knowledge, skills, experience and learning capacity of the people available to the organization’. It defined the management of this human capital, HCM, as ‘a strategic approach to people management that focuses on the issues that are critical to an organization’s success’. It also emphasized that ‘HCM is a performance, not a social, issue … that treats human capital as a positive –– and active –– asset to be developed, not a passive cost.’

I agree with all of this but am still not clear whether the taskforce ever really understood what they meant by it. Much of what the taskforce produced did not seem particularly strategic. For example, at the launch of the taskforce’s consultation process, Kingsmill described how the group would look at whether firms should be compelled to publicly justify their pay policy for the whole workforce, as well as top executives. Kingsmill asked:

How can you have a productive, well-motivated workforce if they’re not being fairly paid? You have to have a fair pay system which is as transparent as possible. (Stewart, 2003)

While an important topic, this is also clearly an issue of compliance or operational rather than strategic significance.

The taskforce also referred to the importance of measurement, stating that HCM, ‘seeks systematically to analyse, measure and evaluate how people policies and practices contribute to value creation’ (Kingsmill, 2003b). Once again, as long as systematic measurement takes a back seat to the strategic management of a people, I can easily agree with this.

The taskforce provided a number of sample ‘HCM’ reports but the lack of a clear definition of HCM resulted in a very diverse selection of samples. Some of these demonstrated a fairly traditional, operational approach to the management of people. Other sample reports, particularly the RAC’s, focused on the measurement rather than the management of people. Unilever’s report described a more strategic approach to people management and RBS’s emphasized the need for both a strategic approach and the measurement of that approach.

I think the taskforce’s half-hearted emphasis on ‘a strategic approach to people management’, together with a fairly strong focus on measurement, and the mixed group of sample have reports have contributed towards some people perceiving HCM as a measurement-focused approach to HRM. However, as well as wanting to see reporting of standard measures that would allow comparisons to be made across organizations, the taskforce did recognize the need to give companies the discretion to focus on their own strategy and to determine their own model of HCM. The difficulty was in balancing these two needs. Kingsmill summarized the issue well at the start of the taskforce’s consultation period, saying, ‘We don’t want prescription and box-ticking, but we don’t want a lot of clichéd rubbish either’ (Stewart, 2003).

Kingsmill’s taskforce recommended that all UK organizations producing voluntary or mandatory OFRs (where the latter have now been replaced with business reviews) should include within them information on HCM or explain why this is not material. HCM reports should have a strategic focus and be based upon the aspects of people management that a company’s Board believes are key to its performance. However, although Kingsmill argued that, short term at least, it would be impossible for common standards to be set, the taskforce did state that reporting should be based on sound and objective data.

Value Reporting

In fact, the paradoxical need for both strategic and standardized reporting had already been addressed elsewhere. The global professional services firm, PricewaterhouseCoopers (PwC), owners of benchmarking firm Saratoga, has emphasized the need to balance the reporting of hard, standardized and financial metrics with more discretionary and strategic information. Calling for a ‘value reporting revolution’, the firm has reported on research finding that only 19 per cent of investors and 27 per cent of analysts ‘found financial reports very useful in communicating the true value of companies’ (Eccles et al., 2001).

One particularly interesting piece of PwC’s research was conducted in collaboration with Schroders Asset Management. A control group of analysts at Schroders was given an annual report for the Danish company Coloplast that was regarded as an example of good practice in non-financial reporting. A second group was given an edited version of the report which omitted all the contextual information and non-financial data. Compared to the control group, the second group came up with generally higher earnings estimates for the company, but across a very broad range. Whereas 60 per cent of the control group issued a ‘buy’ recommendation, 80 per cent of the second group strongly recommended selling the company’s shares (Thomas, 2003).

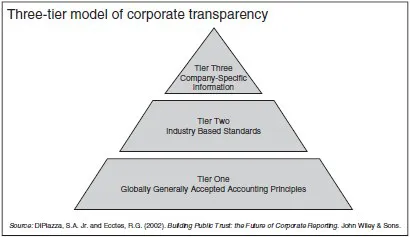

PwC recommends, that more information about intangibles be communicated to investors by including broader financial and non-financial key performance measures in reports. To explain this need, PwC provides a three-tier model of corporate transparency (Figure 1.1), emphasizing that reporting needs to address all three tiers (DiPiazza and Eccles, 2002).

PwC’s triangle does need updating for our purposes. The firm calls the bottom tier in their model Globally Generally Accepted Accounting Principles, or Global GAAP. In fact, the firm’s desire to have a globally agreed set of accounting principles is rapidly becoming a reality as international financial reporting standards gain momentum worldwide. However, changing the focus of this level to people management rather than accounting makes it look a lot more daunting. There is a long way to go to before we have a common set of generic standards for people management data.

The next tier in PwC’s model consists of standards that are ‘industry-specific, consistently applied, and developed by the industries themselves’ and the top tier includes guidelines for ‘company-specific information such as strategy, plans, risk management practices, compensation policies, corporate governance, and performance measures unique to the company’ (DiPiazza and Eccles, 2002).

Although I think PwC’s insights on reporting are largely correct, I believe an even more important point lies behind them. This is about how the nature of information changes at each level in the triangle and the value this provides to understanding. So I suggest updating the model for HCM to emphasize this hierarchy of information and renaming the three levels as data, information and knowledge. As T.H. Davenport and Prusak (1998) stress in their book, Working Knowledge, organizations need to understand the different requirements and benefits of these three levels:

Figure 1.1 Three-tier model of corporate transparency

Data, information and knowledge are not interchangeable concepts. Organizational success and failure can often depend on knowing which of them you need, which you have, and what you can and can’t do with each. Understanding what those three things are and how you get from one to another is essential to doing knowledge work successfully.

Data

Data is the most basic level of information and is used in what I call metrics: factual, objective, quantitative and especially financial measurements and statistics that provide reliability and comparability over time. Metrics can help gain the attention of CEOs and CFOs who are traditionally more interested in issues that have numbers attached to them, believing that ‘if you can measure it [meaning objectively and quantitatively], you can manage it’. However, metrics alone are not going to enable the comparability across organizations that analysts and investors require in order to make buy or sell decisions. This requires the use of standards or key performance indicators (KPIs) that are based on commonly accepted terms and definitions. Clearly some sets of measures already exist and these could form the basis for global GAAP-like standards.

One example is the Sustainability Reporting Guidelines from the Global Reporting Initiative (GRI) which are used in many Corporate Responsibility reports. These standards are now into their third generation and are used by more the 600 companies worldwide. Organizations can choose which parts of the standards to use depending on their size, sector and other factors. The standards contain 12 core performance indicators relating to employment issues, one of which is a measure of ‘average hours of training per year per employee by category of employee’.

However, there is no similar standard specifically focused on people management. Referring to approaches developed by Mercer (see Chapter 2), Watson Wyatt (Chapter 3) and Penna (that are developed within this book), employment relations journalist Stephen Overell (2004) describes his view that it should be possible to develop a core set of standards:

It is true that there are many diverse approaches to HCM. A quick survey of Watson Wyatt’s Human Capital Index (which purports to link HR practices to financial performance), Penna Consulting’s ‘strategic measures’ (things like employee motivation levels and leadership abilities), and Mercer Human Resource Consulting’s ‘internal labour market analysis’ (a bid to track patterns in employee behaviour statistically) is enough to prove the point. But that is not to say you can’t have common standards around which a debate can mature.

I largely agree with this perspective and was quoted by Richard Donkin in the Financial Times suggesting that Saratoga’s benchmarks would be the obvious base for this development:

In the meantime, he believes companies are in a position to reach some consensus on standard external measures. An industry standard, he says, may eventually settle on sets of existing measures, such as those pioneered by EP-First and Saratoga Institute, the human capital arm of PricewaterhouseCoopers that runs an index of more than 100 performance indicators across the HR field. (Donkin, 2004)

Despite this potential opportunity, Accounting for People realized that it would not be possible to pick on one of the competing sets of standards and felt that there was not enough demand to specify a new set of standards during the period of their review. They therefore proposed that the way forward was through an ‘evolutionary approach’ in which the momentum created by the taskforce would encourage more reporting and an increasing opportunity to s...

Table of contents

- Cover Page

- Half Title page

- Title Page

- Copyright Page

- Contents

- Foreword

- Preface

- Acknowledgements

- Part 1 Creating Value in HCM

- Part 2 The Strategic HCM Planning Cycle

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Strategic Human Capital Management by Jon Ingham in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.