Auditing has become an essential component in market societies and the need for auditing skills has risen in line with globalization. This textbook provides a comprehensive overview of the role of financial statement auditing in contemporary society, including the auditor's role in evaluating the financial reporting of an auditee—a topic of central concern in the recent comprehensive review of the auditing profession in the Brydon Report (2019).

The experienced authors provide insight into auditing research to help readers understand its function, regulation, and role in theory and practice. With focus on private sector financial statement auditing and its regulation, the book includes perspectives on social theory, history, and the importance of professional standards. The thought-provoking final chapter challenges students to consider the effectiveness of auditing in evaluating increasingly risky and complex accounting estimates involving assumptions about future events.

A fundamental approach to auditing theory, this textbook will be useful reading for advanced undergraduate and postgraduate students across business and accounting fields.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

HISTORY OF AUDITING, AUDIT RESEARCH, AND AUDIT THEORY

We begin by providing an overview in this chapter of auditing and its history, research, and theory. This is largely a summary of prior research but we also add some analysis and synthesis. In the first section we introduce the notion of accountability and how it historically gave rise to accounting and auditing. Section 1.2 briefly reviews the history of the modern audit profession. Section 1.3 reviews the evolution of audit and accounting standards and their relationship. Section 1.4 provides an overview of the most common areas of audit research, while section 1.5 provides an overview of audit theory.

1.1

A brief overview of the origins of auditing, accounting, and accountability

1.2

A brief history of the auditing profession

1.3

A brief history of changes in audit and accounting standards

1.4

Review of some prior audit research

1.5

Auditing theory

1.6

End-of-chapter question

1.1 A brief overview of the origins of auditing, accounting, and accountability

Auditing and accounting arise from the need for accountability. The roots of accounting and auditing go back to the earliest agrarian societies dating to some 10,000 years ago. The reason for this is that it is only in agrarian societies that an economic surplus was created and a major social issue was, and is, how to distribute this surplus. The concept of accountability arises in large part from giving an account of how resources are allocated as part of a process of making individuals answerable for the resources entrusted or promised (Wikipedia, “Accountability,” 1). There are two aspects to accountability: transparency and effective sanctions (Wyatt 2018). Transparency relates to the availability of understandable information which allows effective monitoring of the performance of the accountable parties. Effective sanctions or rewards, depending on the circumstances, provide the appropriate incentives for the accountable parties. The ultimate goal of accountability is to encourage trust in institutions and individuals.

Critical social research on accountability cautions about the limitations of giving a full account of a social relationship and its potential for abusive control (e.g., Roberts 2009; Messner 2009). When used appropriately, however, accountability arising from accounting record keeping has proven to play a key role in the economic development of ancient as well as modern societies and basic institutions such as money, property rights, markets, and the legal system (Basu et al. 2009, 896).

In the earliest agrarian societies new social problems arose concerning the best way to distribute a stable and dependable economic surplus (Nolan and Lenski 2006, 113). This problem had not existed in the preceding hunting and foraging stage of human development because there had not been a dependable economic surplus before. Instead, individuals in pre-agricultural societies had to cooperate in small groups for protection and in order to share the results of risky foraging and hunting activities. A single individual could not survive long with the technology available in pre-agricultural environments. The median size of a hunting and gathering society was 40 individuals, varying depending on the type of natural environment (ibid., 68). There was no stable group economic surplus in pre-agricultural societies. However, with the advent of the technology of static agriculture, a group surplus began to develop and with it the beginnings of full-time specialization of labor and a social hierarchy. Group sizes by this point had increased to a median size of 1,500 individuals in the simplest horticultural societies (no metal tools or weapons) to 5,250 individuals in advanced horticultural societies (use of copper tools) to over 100,000 individuals in advanced agrarian societies (use of bronze and iron tools, invention of plow and wheel with application to pulling carts and pottery production, literature, numbers, and the calendar). Historical examples of advanced agrarian societies include huge states such as the Han Dynasty, China (100 million people) and the Roman Empire (60 million people). These numbers are based on formal censuses that have been preserved, and illustrate the high degree of administrative organization of these states.

With the first economic surplus came social inequality in society with just a few favored individuals getting the majority of the surplus.

In all early civilizations a small privileged class appropriated, in ways that were socially acceptable, a disproportionate share of the available wealth … In most cases agricultural produce and manufactured goods were appropriated by the state in the form of taxes in kind, while surplus labor was appropriated by imposing corvee labor.

(Trigger 2003, 385)

The ideology that legitimized the centralization of state-like entities in the earliest civilizations around the world was based on religion (Nolan and Lenski 2006, 138). This role of religion is the first time that ideology is seen as playing a recognizable role in societal development (ibid., 130). Religion helped legitimize the role of the ruling elite by linking them to gods and divine powers. However, in most civilizations the most important religious leaders/priests were not the highest-ranked individuals in society. This was reserved for kings or other rulers. The concept of the “divine right of kings,” which legitimized absolute monarchies in which the king was the state, was not overturned in England until the 1600s and in France until the 1700s. Religion helped legitimize the rulers and the role of the ruling class in governing a state and a growing, stable economic surplus. A growth in the economic group surplus could be achieved by growing the size of the state, increased trading, and/or technological improvements.

In return for state protection, public works, and overall stability in a precarious life, farmers were prepared to have part of their economic surplus taken up by taxes. The agrarian states had 70–90% of labor devoted to food production (ibid., 313). The ruling elite consisting of 2–3% of the population was able to command a majority of the total surplus available. This amounted to as much as 70% of the total surplus and 20% of the total production by the society (Trigger 2003, 387). As societies evolved with the expansion of technology, trade, and the state through military force, there was an increasing need to track the complexity of the sources and uses of the surplus through an accounting system.

Over time the proportion of wealth accumulated by the ruling class increased, and better record keeping and development of a monetary system appear to be the main reason for the ruling elite improving their grasp of the amount of taxation that was sustainable.

Because of their low per capita productivity, early civilizations did not have the capacity to monitor and tax resources as is done today. The government of Old Kingdom Egypt appears to have gone farthest in keeping detailed registers of land ownership and rights to benefit from its produce, but there is no evidence of detailed reckonings of total revenue received by the central government.

(Trigger 2003, 386)

Accountability for taxes was not the only use of accounting in agrarian societies. From the earliest times there was also a need to keep records of how the taxes collected were used administratively to meet rulers’ needs and those of palace activities. There were allocations to priests and temples, nobles, military leaders, and others in the ruling elite who supported the leader administratively. There was a web of property rights in the ruling elite, a famous example of which can be found in the Domesday Book of William the Conqueror after his invasion of England in 1066.

With the increase in trade following the Crusades in the 11th to 12th centuries of the current era (ce), an increasing source of wealth for rulers was trade. Trade also encouraged technological development such as Arabic numerals and double-entry bookkeeping (1300 ce). Trade is what created the first capitalist economies in Northern Italy, which in turn fostered a flourishing of the arts and sciences in the Renaissance. Several writers have commented on this close connection between more sophisticated accounting, trade, and innovation in many fields including governance (Soll 2014, Ch. 1; Gleason-White 2013, Ch. 2).

Soll (2014, 2–3) notes that ancient accounting was limited to inventory accounting. The major purpose of ancient world accounting was for tax accountability, but once record keeping evolved it was also used to keep track of the increasingly diverse types of inventory, as documented in Basu and Waymire (2006).

A proprietary theory of the state evolved which continues in some countries to this day. “It is said of the Ptolemies of Egypt, for example, that they showed the first emperors of Rome how a country might be run on the lines of a profitable estate” (Nolan and Lenski 2006, 161). The proprietary approach to government was widespread in Europe throughout the Middle Ages and in the Russian Empire well into the 19th century when serfdom was abolished. Research in economic sociology shows that in the late 19th century in China the governing class’s average income was 50 times that of families not in the governing class. The English nobility had an average income 200 times that of field workers in 13th-century England.

Putting together the evidence from many sources, it appears that the combined income of the ruler and governing class in most advanced agrarian societies equaled not less than half the total national income, even though they numbered 2 percent or less of the population.

(ibid., 161)

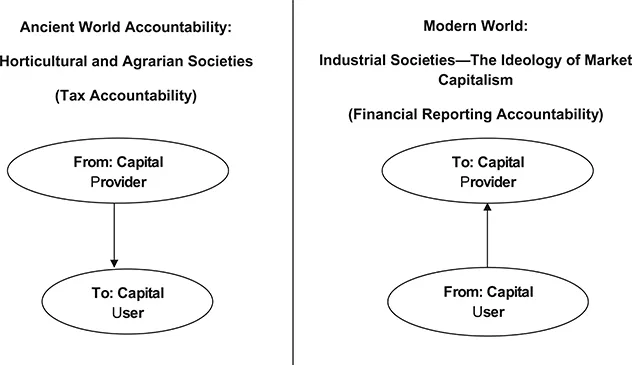

An increasingly sophisticated accounting system was necessary to maintain this type of control and wealth allocation with increasing population, trade, technological change, specialization in the division of labor, and complexity of institutions. “The basic philosophy of the governing class seems to have been to tax peasants to the limit of their ability to pay” (ibid., 153). And this type of accountability seems to be the main reason record keeping was maintained and refined over time, despite many other commercial uses of record keeping throughout history (e.g., see Basu and Waymire 2006 for an overview of the evolution of record-keeping technology). We will refer to this fundamental form of accountability from the ultimate providers of capital, i.e., the peasant, merchants, and artisans of the lower classes to the ruling elite representing 2% of the population, as the old world accountability.

This accountability is still important in all modern societies as it now represents each individual’s obligation to pay taxes in the modern world. This type of accountability is now studied primarily by tax scholars, but it reminds us of the importance of considering to what use these extensive resources are put. It is noteworthy that recent proposals to reduce inequality in the world’s most advanced economies typically involve modifying the tax system. This illustrates that old world accountability is still very relevant in the modern world (e.g., Tirole 2017, 57; Groenewegen et al. 2010, 130). It is also noteworthy that agency problems that auditing is in part designed to help address are predominantly another type of accountability. We will refer to this second kind of accountability in the rest of this book as modern world accountability.

Modern world accountability relates to the accountability of capital users to capital suppliers. This is the accountability of managers to the owners and other capital providers to a firm. Audits of financial statements are primarily concerned with this type of accountability, as well as financial reporting, internal controls, corporate governance, and regulation of capital markets, which all relate to strengthening modern world accountability. The auditor’s role in this type of accountability is the focus of most of this book.

To recap, old world accountability relates to the accountability of the capital supplier to the capital user, whereas modern world accountability relates to the accountability of the capital user to the capital provider. These two types of accountability are summarized in Figure 1.1. Essentially, in old world accountability individuals are held accountable to pay their share of taxes to the state. Obviously, this form of accountability still exists because we are still obligated to pay our share of taxes, and in many countries there is the concept of “tax freedom day” representing the part of the year in which our obligations to pay annual taxes are completed and for the remainder of the year one’s labor goes toward covering the other costs of living.

Figure 1.1 Two basic types of accountability as a result of the evolution of human societies: the Basu and Waymire 2006 discusses how this process got started with the need for record keeping

1.2 A brief history of the auditing profession

With the increasing complexity of accounting arose the need for ensuring its accuracy, and this in turn fostered the rise of the audit function. Modern auditing relates to the credibility or assurance of the second type of accountability. The exception is tax auditing which adds credibility to the first type of accountability. Tax auditing is the older form of auditing. It was extended in historical times to accountability of nobles or regional officials to the head of government, whether they were the chief nobles, kings, or an emperor. In these cases the subordinate official is not a provider of capital but is accountable for resources they have been delegated to administer. However, it can be viewed as the second type of accountability if the king is viewed as the provider of the resources to the administrator.

The second type of accountability can also arise in mercantile enterprises in which an entrepreneur provided with capital by others must give an account of how the capital was used.

The earliest examples of auditing seem to be from Ancient Egypt where the Pharaohs had two accountants maintain separate sets of records from the same sources of information. If the two independently created sets of records did not agree then the Pharaohs knew something was amiss. The first auditors were thus accountants who maintained an independent set of records of the same activities. If the two sets of records did not match, the penalties for the record-keeping accountants could be severe.

As the complexity of record keeping further increased, two sets of records became uneconomical and the second accountant increasingly independently monitored the work of the first accountant. When the first accountant reported (usually) orally the results of the record keeping, the second accountant “heard” this report and commented on its accuracy. So the term auditor comes from the Latin for “to hear” and this practice was continued from Ancient Persian times to the Middle Ages, through to today’s auditors when they attend the annual shareholder meetings.

By the time of Ancient Athens, accounting was being connected to political accountability in the first democracies. “In contrast to oligarchies—in which the powerful few ruled and there was no system of the 2nd type of accountability accountability—democratic Athens had the first such system of accountability” (Soll 2014, 3). Early in the Roman Empire there was a similar system of accountability also implemented by public accounting officers. Every public accounting officer had to submit a full accounting of funds received, including gifts.

Augustus was the first Roman emperor to make public the Empire’s financial assets along with his political achievements such as public works in the form of road building, free bread for Roman citizens, circuses, and expanding the Empire. This public accountability of the second type was limited to some degree by the toleration of fraud and bribery of public officials, especially by the Roman emperors. Interestingly, this type of toleration continues to the present day in the form of weaknesses in accounting and audit practice. With the fall of Rome and the advent of the Dark Ages in Europe, this second type of accountability disappeared and rulers were answerable only to deities, as in the earliest agrarian times.

After 1000 ce, with increased centralization of state power and the formation of modern nation states, revival of trade, and re-adoption of coinage, society looked to universal religion in the form of the Church and to Ancient Roman precedents for guidance. Thus auditing and accounting were revived initially primarily in terms of the first type of accountability, as illustrated by the Domesday Book.

However, where trade was the dominant source of economic activity such as the North Italian city states of Venice and Genoa, record keeping for the second type of accountability became increasingly important and developed rapidly. The independent merchants of these city states were interested in calculating the worth of their trade. Using new technology introduced from Asia such as the abacus, Arabic numerals, and advances in arithmetic, the double-entry system of accounting evolved. A major advantage of this system is that it provided an internal check for fraud. When combined with the printing press and writing in modern languages, the first formal theory of accounting and detailed description of the double-entry system was published in 1494 by Pacioli (Gleason-White 2013, 74–75 and ch. 4). The auditors who heard these reports also had to keep up with these changes in accounting practice. This was necessary to maintain accountability. Thus auditing and accounting are to some degree non-separable if the accountability is to be maintained. This will be an important theme to w...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Table of Contents

List of Illustrations

Introduction

1 History of Auditing, Audit Research, and Audit Theory

2 Social theory and auditing: role of social norms, culture, politics, institutions, and ideology

3 Professional Ethics and Reputation

4 Audit Regulation

5 Auditing Standards

6 Auditor Liability and Litigation Risk

7 Measurement of Audit Quality

8 Determination of Audit Fees

9 Research on the Impact of Audits

10 Audits of Compliance Reporting with GAAP

11 Audits of Fair Presentation Reporting

References

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Auditing and Society by Wally Smieliauskas,Minlei Ye,Ping Zhang in PDF and/or ePUB format, as well as other popular books in Business & Auditing. We have over 1.5 million books available in our catalogue for you to explore.