Since the financial crisis of 2008-09, central bankers around the world have been forced to abandon conventional monetary policy tools in favour of unconventional policies such as quantitative easing, forward guidance, lowering the interest rate paid on bank reserves into negative territory, and pushing up prices of government bonds. Having faced a crisis in its banking sector nearly a decade earlier, Japan was a pioneer in the use of many of these tools.

Unconventional Monetary Policy and Financial Stability critically assesses the measures used by Japan and examines what they have meant for the theory and practice of economic policy. The book shows how in practice unconventional monetary policy has worked through its impact on the financial markets. The text aims to generate an understanding of why such measures were introduced and how the Japanese system has subsequently changed regarding aspects such as governance and corporate balance sheets. It provides a comprehensive study of developments in Japanese money markets with the intent to understand the impact of policy on the debt structures that appear to have caused Japan's deflation. The topics covered range from central bank communication and policymaking to international financial markets and bank balance sheets.

This text is of great interest to students and scholars of banking, international finance, financial markets, political economy, and the Japanese economy.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

1 The Japan Premium and the first stage of the monetary transmission mechanism

Alexis Stenfors

1 Introduction

Japan has taken unconventional monetary policy and financial stability measures to the extreme – ultimately with the aim to recover the dynamism of the Japanese economy. In order to understand the logic underpinning these measures, it is necessary to study the history and process which resulted in them being adopted. Put differently, why were conventional policy measures inadequate?

This chapter focuses on the interest rate channel and the first stage of the monetary transmission mechanism, which is central to the traditional view of central banking. Namely, if the central bank changes the official interest rate, banks will adjust their interest rates accordingly. Coupled with the expectations of future central bank interest rate changes, and a host of other factors influencing markets, interest rates with longer maturities are also to be affected. Ultimately, the central bank monetary policy decision should have an impact on banks, businesses, households and variables in the economy as a whole – such as inflation, employment and output. Central banks do not determine at which interest rate banks lend to each other, or, indeed, to other agents in the economy. The first stage of the monetary transmission mechanism is therefore crucial, as it involves the immediate response to a central bank decision by banks and other financial market participants.

A breakdown of the first stage of the monetary transmission mechanism is serious, as it seriously undermines the ability of central banks to conduct monetary policy or even influence expectations by market participants. Consequently, variables and indicators used to measure and decompose risks in the interbank market are crucial for central bankers. For Japan, this became evident during the Japanese banking crisis – when the strains in the interbank market triggered the so-called Japan Premium. The market turmoil that started in August 2007 came to have a similar effect, albeit on an international scale. Both episodes resulted in significant central bank and government intervention to rescue the financial system – in other words, to restore the functioning of the first stage of the monetary transmission mechanism.

This chapter studies the evolution of Japanese money market risk premia during the last two decades. It shows that traditional ways to measure the functioning of the first stage of the monetary transmission mechanism no longer tell a consistent story. Using money market benchmarks and the covered interest rate parity as a lens, the chapter critically examines a string of distinct, but closely interconnected, assumptions and misperceptions underpinning theoretical assumptions. By doing so, it not only sheds some fresh light on current financial market ‘puzzles’ but also on the Japan Premium during the 1990s.

The chapter is structured as follows. Section 2 gives a historical background of money market risk premia from the emergence of the Japan Premium until today. Section 3 studies the market micro-foundations of the short-term money markets, and their implications. Section 4 concludes.

2 Money market risk premia and the covered interest rate parity

2.1 The Japan Premium era

The monetary transmission mechanism is the process by which central banks, through their monetary policy decisions, influence market interest rates and expectations – and ultimately credit and price formation in the economy as a whole. Seen from a different perspective, the process is also the key channel through which a money market interest rate, such as the interbank deposit rate, is generated. On the one hand, the level is affected by the official central bank rate. On the other hand, it is influenced by the borrowing and lending activity of market participants – and their expectations.

The London Interbank Offered Rate (LIBOR) and equivalent benchmarks tend to be used as market indicators for at which interest rate interbank deposits are traded. If LIBOR deviates substantially and systematically from the risk-free rate derived from the official central bank rate, it signals that the monetary transmission mechanism is severely impaired. From this viewpoint, the mechanism appears to have worked reasonably well until the outbreak of the financial crisis of 2007–08. LIBOR tended to track official central bank interest rates, and the expectations of future changes in them, very closely. In other words, LIBOR could be relied upon as a benchmark in models for monetary policy decisions.

One major exception to this was the Japanese banking crisis in the 1990s. Up until August 1995, when Hyogo Bank defaulted, Japanese authorities had intervened by arranging the merger of an insolvent bank with a solvent acquiring bank. The first commercial bank failure in Japan resulted in the so-called Japan Premium, which highlighted the increasing inability of Japanese banks to access unsecured funds in foreign currencies. Before the Hyogo collapse, the Japanese government had intervened when needed to prevent potential failures of financial institutions, by arranging a merger of the insolvent bank with a solvent bank. With such a policy framework, Japanese banks had, therefore, been perceived to be solvent and safe by financial market participants. When the authorities failed to save Hyogo Bank, however, this perception radically changed – resulting in a premium on Japanese banks’ borrowing costs. Indeed, as Spiegel (2001) notes, the trigger for this premium to emerge was a change in government policy.

The Japan Premium was reflected in two financial market indicators in particular: the TIBOR-LIBOR spread and the CRS spread.

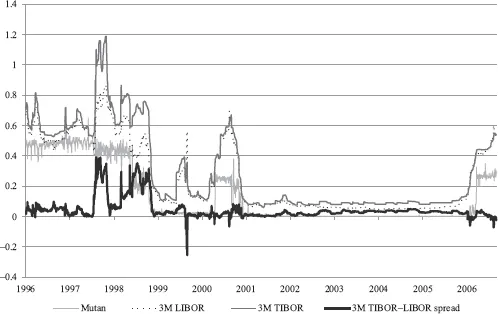

The LIBOR is a benchmark for the short-term interbank money market in which large banks can borrow from each other in major currencies. The TIBOR (Tokyo Interbank Offered Rate) is a similar benchmark set in Tokyo. The Japanese yen LIBOR and TIBOR are interbank money market benchmarks for yen deposits. They should theoretically reflect not only the current and expected future official rate of the Bank of Japan, but also incorporate credit and liquidity risk (Stenfors, 2013). The TIBOR panel mainly consisted of Japanese banks, whereas the London-based LIBOR mainly included European and American banks. Hence, a higher TIBOR could be seen as a reflection of the increased funding cost (i.e. perceived creditworthiness and ability to access liquidity) of Japanese banks compared to that of their foreign peers. The individual LIBOR submissions by the few large Japanese banks that were part of the panel in London were consistently higher and thus mostly omitted from the calculation of the LIBOR average. This left the Japanese yen LIBOR fixing largely in the hands of non-Japanese banks without funding issues. Figure 1.1 shows the 3-month Japanese yen LIBOR and TIBOR, the TIBOR-LIBOR spread and Mutan (the uncollateralised overnight call rate) from 1 May 1996 to 29 December 2006. As can be seen, the TIBOR-LIBOR spread for Japanese yen widened sharply during the crisis period. Hence, the jump in the TIBOR-LIBOR spread could be said to have originated in higher perceived credit risk directly leading to funding liquidity risk that the benchmarks were supposed to express.

However, overall market liquidity in Japanese yen was not affected in the same way. Transactions in yen between non-Japanese banks continued normally, and despite becoming considerably more volatile, market illiquidity did not force foreign banks to liquidate yen-denominated assets on a large scale. As such, market indicators did not point towards a ‘Japanese yen crisis’, but a ‘Japanese banking crisis’.

The Japan Premium was also noticed in the foreign exchange swap and cross-currency swap markets. According to the covered interest rate parity (CIP), interest rate differentials between two currencies should be perfectly reflected in the foreign exchange swap price. Otherwise, arbitrage would be possible. In terms of Japanese yen against US dollars, this can be expressed as:

(1)

where is the continuously compounded US interest rate (typically expressed in the US dollar LIBOR), and the yen interest rate (such as yen LIBOR) for maturity t. and represent the FX spot and forward rates between the currencies respectively.

In log-terms, the continuously compounded forward premium,, is equal to the interest rate differential between Japanese yen and US dollars:

(2)

This particular kind of arbitrage, it was assumed, had ensured that the deviation from the CIP had tended to be close to zero. Following the market convention, interbank foreign exchange swaps are generally quoted against US dollars. Deviations from the CIP are therefore normally measured as the difference between the implied interest rate (using the US dollar interest rate and the foreign exchange transactions) and the benchmark interest rate for the counter currency.

Although Japanese banks were offered ample liquidity in yen from domestic sources (notably the Bank of Japan), they needed foreign currency funding as a result of large-scale investments made abroad during previous boom years. Since the Bank of Japan could not offer US dollar reserves, and the Eurocurrency markets dried up for the Japanese banks (being perceived as less creditworthy), they had to turn to the FX swap markets. In this way, they could use their yen liquidity to swap them into US dollars, which they required. When Japanese banks headed for this last funding avenue, the CIP-deviations became more substantial, indicating that, for traders holding Japanese yen, swapping them to US dollars (or other foreign currencies through dollars) would be much more expensive than stated in the Eurodollar market.

Equation (1) can be rearranged to depict the difference between the implied interest rate (via the base currency interest rate and the FX market) and the direct interest rate in the counter currency – typically referred to as the ‘cross-currency basis’.

In terms of Japanese yen against US dollars, the continuously compounded cross-currency basis,, can be seen as the CIP-deviation between the two currencies for maturity t:

(3)

In logs, the cross-currency basis is expressed as:

(4)

This expression is useful when studying the cross-currency basis swap (CRS) market, which is ...

Table of contents

Cover

Half Title

Series

Title

Copyright

Contents

Preface

Acknowledgements

List of contributors

List of figures

List of tables

Abbreviations

Introduction

1 The Japan Premium and the first stage of the monetary transmission mechanism

2 The foreign currency swap market: A perspective from policymakers

3 The effectiveness of unconventional monetary policy on Japanese bank lending

4 Japanese banks in the international money markets

5 The Japanese balance sheet recession 20 years on: Abenomics – economic revival or corporate financialisation?

6 An analysis of the impact of the Bank of Japan’s monetary policy on Japanese government bonds’ low nominal yields

7 Unconventional monetary policy announcements and Japanese bank stocks

8 Bank of Japan and the ETF market

9 Quantitative and qualitative monetary easing, negative interest rates and the stability of the financial system in Japan

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Unconventional Monetary Policy and Financial Stability by Alexis Stenfors, Jan Toporowski, Alexis Stenfors,Jan Toporowski in PDF and/or ePUB format, as well as other popular books in Economics & Finance. We have over 1.5 million books available in our catalogue for you to explore.