- 328 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The World of Private Banking

About this book

This is a full and authoritative account of the history of private banking, beginning with its development in conjunction with the world markets served by and centred on a few European cities, notably Amsterdam and London. These banks were usually partnerships, a form of organization which persisted as the role of private banking changed in response to the political and economic transformations of the late 18th and early 19th centuries. It was in this period, and the succeeding Golden Age of private banking from 1815 to the 1870s, that many of the great names this book treats rose to fame: Baring, Rothschild, Mallet and Hottinger became synonymous with wealth and economic power, as German, French and the remarkably long-lasting Geneva banks flourished and expanded. The last parts of this study detail the way in which private banking adapted to the age of the corporate economy from the 1870s to the 1930s, the decline during and after the Great Depression and the post-war renaissance. It concludes with an appraisal of the causes and consequences of the modern expansion of private banking: no longer the exclusive preserve of partnerships, the management of investment portfolios of wealthy individuals and institutions is now a major concern of international joint-stock banks.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

The Rise of the Rothschilds: the Family Firm as Multinational1

This chapter attempts to explain the rapid rise of the Rothschild bank to a position of supremacy in international finance between around 1810 and 1836. The first section describes the size of the bank, which, for most of the nineteenth century, was the biggest bank in the world in terms of capital. The second section discusses the business the Rothschilds did, in particular their development of the international bond market. The third section discusses the structure of the partnership. The fourth section shows how intermarriage helped ensure that capital remained in the family. Finally, an attempt is made to identify the Rothschilds’ distinctive business methods. These, it is suggested, provide the best explanation for the Rothschilds’ astonishing success.

Between around 1810 and 1836, the five sons of Mayer Amschel Rothschild rose from the obscurity of the Frankfurt Judengasse to attain a position of unequalled power in international finance. Despite numerous economic and political crises and the efforts of their competitors to match them, they still occupied that position when the youngest of them died in 1868; and even after that their dominance was only slowly eroded. So extraordinary did this achievement seem to contemporaries that they often sought to explain it in mystical terms. According to one account dating from the 1830s, the Rothschilds owed their fortune to the possession of a mysterious ‘Hebrew talisman’. It was this which enabled Nathan Rothschild, the founder of the London house, to become ‘the leviathan of the money markets of Europe’.2 Similar stories were being told in the Russian Pale as late as the 1890s.3 They form part of a complex web of fantasy which has been – and continues to be – woven around the name Rothschild.

This chapter, however, is not concerned with the Rothschild myth but with the reality of their rise as bankers. For reasons of space, it mainly concentrates on the period prior to Nathan Rothschild’s death in 1836. This was in fact the period when the Rothschilds made their most important contribution to ‘the making of modern capitalism’. In part, their contribution was a matter of scale: as the first section of the chapter shows, there had never been a larger concentration of capital than that accumulated by the Rothschild brothers. The second section discusses the various types of business they did, attaching special importance to their development of the international bond market, but also considering their role in the markets for commercial bills, commodities, bullion and insurance. The third section discusses the structure of the partnership. The fourth section shows how exceptionally frequent intermarriage complemented the partnership system by ensuring that capital remained in the family. In the fifth and final section, an attempt is made to characterize the Rothschilds’ distinctive business ethos and to identify a set of Rothschild business rules. These, it is suggested, provide the best explanation for the Rothschilds’ astonishing success.

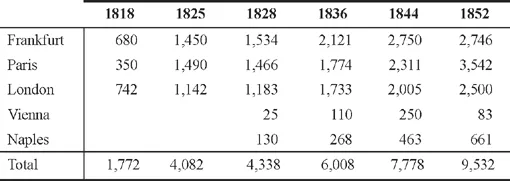

Previous attempts to analyse the surviving accounts of the five ‘houses’ have been hampered by the inaccessibility of archives in London and Moscow.4 These have now been opened. Analysis, however, is less easy than might be imagined, for two reasons. First, the Rothschilds did not keep accounts in a modern way; indeed, to begin with they hardly kept them at all. The system of partnership contracts (described below) necessitated the drawing up of balance sheets, but at irregular intervals. Nevertheless, it is possible to reconstruct from these documents a fairly satisfactory series for the capital of the combined Rothschild houses. Table 1.1 summarizes the available figures for the combined capital of the various houses in the period 1818–52:

Table 1.1 Combined Rothschild capital, 1818–1852 (thousands of £)

Sources: CPHDCM, 637/1/3/1–11; 1/6/5; 1/6/7/7–14; 1/6/32; 1/6/44–45; 1/7/48–69; 1/7/115–120; 1/8/1–7; 1/9/1–4; RAL, RFamFD/3, B/1; Archives Nationales, 132 AQ 1, 2, 3, 5, 6, 7, 9, 10, 13, 15, 16, 17, 19; B. Gille, La Maison Rothschild, vol. II, pp. 568–72.

Surviving figures for the individual houses are patchy, especially before 1830. For the London house, no comprehensive accounts have survived before 1828, though there is a complete series of profit-and-loss accounts beginning the following year. The accounts are simple: on one side all the year’s sales of commodities, stocks and shares are listed; on the other, all the year’s purchases and other costs; the difference is recorded as the annual profit or loss. Table 1.2 gives the ‘bottom line’ data for the period up until 1844.

Table 1.2 Profits and capital at N.M. Rothschild & Sons, 1829–1844 (£)

| Profit/Loss | Capital at end of year | Profit as percentage of capital | |

| 1829 | 1,123,897 | ||

| 1830 | −56,361 | 1,067,536 | −5.0 |

| 1831 | 56,324 | 1,123,860 | 5.3 |

| 1832 | 58,919 | 1,182,779 | 5.2 |

| 1833 | 75,294 | 1,258,073 | 6.4 |

| 1834 | 303,939 | 1,562,011 | 24.2 |

| 1835 | 69,732 | 1,733,404 | 4.5 |

| 1836 | −72,018 | 1,661,386 | −4.2 |

| 1837 | 87353 | 1,747,169 | 5.3 |

| 1838 | 83,124 | 1,820,706 | 4.8 |

| 1839 | 52,845 | 1,773,941 | 3.1 |

| 1840 | 30,937 | 1,804,878 | 1.7 |

| 1841 | −49,769 | 1,755,109 | −2.8 |

| 1842 | 40,451 | 1,795,560 | 2.3 |

| 1843 | 23,766 | 1,819,326 | 1.3 |

| 1844 | 170,977 | 1,990,303 | 9.4 |

Source: RAL, RFamFD/13F.

Plainly, there were substantial fluctuations in performance, ranging from the very successful (1834), when profits were close to a quarter of capital, to the disappointing (1830, 1836 and 1841). Averaged out, however, profits were rather unremarkable in relation to capital compared with figures for other banks, though this may reflect the fact that all expenses – including the partners’ interest on their capital shares – were deducted before net profits were calculated. Thus the figure for profits (or losses) shown here was simply added to (or deducted from) the previous year’s capital.5

The other house for which detailed accounts survive is the much smaller Naples house. Considering its size, the Naples house was singularly profitable, especially in the first decade of its existence. Its average annual profits were more than £30,000 between 1825 and 1829, at a time when its capital was little more than £130,000; and throughout the 1830s and 1840s its profits averaged around £20,000.6 Unlike the London Paris house, it appears never to have recorded a loss prior to 1848, despite the financial crises of 1825, 1830 and 1836.

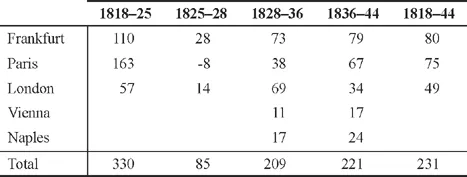

There are, unfortunately, no complete data for the profits of the Paris, Frankfurt or Vienna houses in this period. In the French case, the only surviving figures are for the years 1824–8, and they simply tell us the extent of the damage done to James’s position by the crisis of 1825 (when his losses totalled no less than £356,000) and the speed with which he recovered from the setback.7 However, it is possible to infer average annual profits for all the houses from the combined capital accounts (table 1.3), though the irregular periods which elapsed between agreements make these a rather rough guide to performance. These suggest – rather unexpectedly – that the London house was in fact the least economically successful of the three principal Rothschild houses: average annual profits were significantly higher at both Frankfurt and Paris for the period 1818–44.

Table 1.3 Average annual profits, five Rothschild houses, 1818–1844 (£thousands)

Source: As table 1.1.

The question, of course, is whether it is legitimate to make such comparisons when the houses were regarded by the partners as inseparably linked – as, indeed, a single ‘general joint concern’. The balance sheets of the Naples house reveal how inextricable the activities of the five houses were: between 1825 and 1850, the share of its assets which were monies owed to it by the other Rothschild houses was rarely less than 18 per cent and sometimes as much as 30 per cent.8 This seems to have been the case for all the houses. In 1828, credits to the other house amounted to 31 per cent of the assets of the Paris house.9

The most striking point of all is the sheer size of the Rothschilds’ bank. In 1815, the combined capital of the Rothschild houses in Frankfurt and London was at most £500,000. In 1818, the figure was £1,772,000, in 1825 £4,082,000 and in 1828 £4,330,333. The equivalent figures for the Rothschilds’ nearest rival, Baring Brothers, were £374,365, £429,318, £452,654 and £309,803.10 To take a single year – 1825 – their combined resources were nine times greater than the capital of Baring Brothers and eleven times larger than the capital of James’s principal rival in Paris, Laffitte. They even exceeded the capital of the Banque de France (around £3 million at this time).11 Nor did the Rothschilds lose momentum in the succeeding years. In 1836 – the next time the partners met to settle accounts and renew their contractual agreement – the capital had increased again to £6,007,707. Barings’ capital in that year was £776,650. Eight years later, the Rothschilds had increased their capital to £7,778,200; Barings’ had shrunk to £501,944. The main explanation for this dramatic disparity is not just that the Rothschilds made b...

Table of contents

- Cover

- Half title

- Title page

- Copyright Page

- Table of Contents

- List of Figures

- List of Tables

- Notes on Contributors

- Introduction

- 1 The Rise of the Rothschilds: the Family Firm as Multinational1

- 2 The Rothschild Archive

- 3 Private Banks and the Onset of the Corporate Economy

- 4 London’s First ‘Big Bang’? Institutional Change in the City, 1855–83

- 5 Banking and Family Archives

- 6 The Anglo-American Houses in the Nineteenth Century

- 7 The Parisian ‘Haute Banque’ and the International Economy in the Nineteenth and Early Twentieth Centuries

- 8 Private Banks and International Finance in the Light of the Archives of Baring Brothers

- 9 German Private Banks and German Industry, 1830–1938

- 10 Private Bankers and Italian Industrialisation

- 11 Private Banks and Industry in the Light of the Archives of Bank Sal. Oppenheim jr. & Cie., Cologne

- 12 Jewish Private Banks

- 13 Protestant Banking

- 14 Private Bankers and Philanthropy: the City of London, 1880s–1920s

- 15 Hereditary Calling, Inherited Refinement: the Private Bankers of the City of London, 1914–86

- Bibliography

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The World of Private Banking by Youssef Cassis,Philip Cottrell,Iain L. Fraser in PDF and/or ePUB format, as well as other popular books in History & World History. We have over 1.5 million books available in our catalogue for you to explore.