Following the internationalisation, globalisation and deregulation of the financial market over the last few decades, the financial sector has evolved from a servicing industry into an initiating and leading sector in the international industrialised economy. The power of the financial sector, including Credit Rating Agencies, determines the creditworthiness of companies and countries. Today's financial sector dominates instead of serving the real economy, which puts substantial pres - sure on all the agencies involved, not least the banks, to make the profits that will drive economic growth. As a result of this pressure, moral conduct in the financial sector has been put under severe strain.

This book examines the experience of the recent financial crisis and argues that a firmer ethical grounding for the financial sector is required to prevent the crisis being repeated. The book offers a model for making judgements on financial markets, institutions and products. The model is built on seven major criteria which are examined in depth: Justice, Nature, Sustainability, Legality, Risk and Return, the Stakeholder model and Monism. This multidisciplinary approach integrates philosophy, economics and law to arrive at a new normative approach to financial ethics.

This book is a must-read for finance students at academic levels but also for professionals in the financial sector, who can be helped by implementing the model of NFE in solving financial dilemmas.

There are few sectors in the developed economies that have experienced so many changes over recent decades on technological, economic and legal grounds as the financial sector. Since the full convertibility of the dollar in August 1971 and the subsequent internationalisation, globalisation and deregulation of the financial market, the financial sector has evolved from a servicing industry into an initiating and leading sector in the international industrialised economy. In the last century, until approximately the 1980s, banks had the primary objective of arranging payments and facilitating the real economy through connecting savings and investments with each other. Nowadays, the trade in liquidity, securities, derivative financial instruments and debt securities of many forms has become a goal in itself. The power of the financial sector, including credit rating agencies, determines the creditworthiness of companies and countries. Today’s financial sector dominates the real economy rather than serving it. It is true that the ‘discipline’ of the financial markets during recent decades has streamlined many companies and countries, but globalisation has also excessively strengthened worldwide competition and interdependence among companies and financial institutions. As a result, the economic pressure on all agencies involved has grown substantially – not least on the banks themselves. Moral conduct generally is threatened if the institutions involved and/or individual employees are being squeezed themselves.

Durkheim argues that morality – also called ‘social facts’ by him – contains three important elements.1 First is the imperative character of moral rules. He stresses the constant quality of morality that permanently emanates from an ever-evolving society. A second aspect is the contents of moral actions that are always aimed at the social level of society. This could be the family, the association, the city or the country, but morality always opposes evil and is beneficial for humanity. The third crucial aspect of morality is the autonomy of the willpower of individuals who voluntarily chose to do the right thing for society. Applying the above morality concept to modern financial markets and institutions, it is readily concluded that global financial capitalism does not fit correct economic and moral standards. The debt crisis of the Latin American countries in the late 1970s and early 1980s, the wave of foreclosures of American savings banks in the 1980s, the Japanese crisis in the 1990s, the global internet bubble of 1997–2000 and, of course, the American and European debt crisis of 2007, are silent witnesses to existential tension in global financial capitalism. The current crises of excessive state debt in Europe – and not to mention in America – strengthen the feeling of moral tension. The American central bank (FED) attacked the debt problem in 2011 and 2012 by massively buying up public debt. In Europe this was not allowed at that time, but Mario Draghi – director of the European Central Bank (ECB) – changed this policy in January 2015. In order to fight deflation and recession, a programme of 1140 billion euros of quantitative easing was launched by the ECB for European banks to sell their low-rated public debt. This programme offered banks from early 2012 the opportunity to sell and buy, almost without limited, 3-year loans through which ailing banks would not be forced to sell the loss-making state debt of weak European countries. This programme was even intensified in March 2016. Against this background of balancing above a steep financial ravine, this book analyses the fundamental problems in the financial sector and searches for associated solutions.

Introduction

After half a century of neoliberal financial and macro-economic growth, including a substantial widening of unequal income distribution, there seems to be – as in a dialectic process – at the end of the 20th and the beginning of the twenty-first century a growing interest in the moral quality of human life. Ethics is en vogue, as one might say. Echoing the growing international interest in economics and the environment, there will also be more focus on the moral quality of human behaviour in the economic and financial literature. In economic theory, there is a growing interest in business ethics, the stakeholder model, behavioural economics and stewardship relationships, replacing the traditional stockholder paradigm and agency model. Corporate social responsibility (CSR), sustainable investing, crowd funding and shadow banking thrives in this environment. This book will elaborate extensively on all these aspects.

Also in daily economic practice, the discussion on ethics in recent years has acquired a permanent place. Reputation management has become core business. Examples include the sustainability thinking of enterprises – CSR-reputation – the development of ethical codes, the discussion on the (lack of) success of sustainable investment funds and the upheaval, which, for example, arises upon uncovering insider trade and financial fraud. An important explanation for this is that nongovernmental organisations (NGOs) have gained strong momentum in modern society. Consumer organisations also take their place more vigorously in order to protect the consumer against (alleged) abuse of the financial power of companies. Not only does ethics play a role in the above process, but also ‘armoured’ ethics in the form of potential compensation claims and reputation damage. Therefore companies are challenged not solely in dealing with the interests of shareholders, but also to become more sensitive to the interests of other stakeholders in the company.

A contribution to a very broad and normative topic such as financial ethics is somewhat akin to writing about the quality of football. Almost everyone has their own experiences with morality and their own – often deeply entrenched – opinions. Because emotions are closely linked to opinions, objectivity in a discipline like this is an impossible task for us humans. New financial ethics (NFE) takes a normative stand and maintains that it is a human responsibility to create welfare with a heart by means of fair financial market processes. New financial ethics can conceptually be considered as an ideology that clusters in a cloud of financial knowledge – no, not a secured iCloud – in a shower of actions that are theoretically accessible to everyone. Financially ethical knowledge is not knowledge in the mind of one person, group of persons, the law, or knowledge stored on a stand-alone hard drive – or in a book. Financial ethics is dynamic, engrosses situations and conditions, personifies people and produces new knowledge which then precipitates in the conducts of financial institutes, establishments, cultures and individuals. New financial ethics has the intention to engross human behaviour in society – in whatever shape – and for that very reason deserves explicit academic and practical attention.

This book contains four parts, each emphasising different aspects of the very same elephant: NFE. After this introductory chapter, Part I concentrates on ethics, philosophy and law. The why of moral behaviour is founded there, embedded in theoretical ethics (Chapter 2) and including the role of law (Chapter 3).

In Part II we concentrate on the practice of financial markets (Chapter 4), financial institutions and the role of companies (Chapter 5). Important traditional economic theories and views are discussed here against the background of perceived ethical behaviour. Part III then is the core of the book. In Chapter 6 the fundamentals of NFE are derived and given content. By applying that model, most dilemmas can be properly analysed and brought to a well-founded conclusion. The book concludes in part IV with some extensive examples of how to apply the NFE model. Chapter 7 presents both cases and possible solutions and shows how to apply NFE in practice. Most of the other chapters include at least one real-life moral problem, but here the solutions are left to the reader. These cases are presented in specific numbered boxes within each chapter.

CHAPTER TOPICS

PART I

1-3

Introduction New Financial Ethics (NFE) New Financial Ethics & Law

PART II

4-5

Financial Markets & NFE Companies & NFE

PART III

6

Fundamentals of NFE

PART IV

7

Applications of NFE

Figure 1.1Organisation of the book

This introductory chapter continues by accentuating certain relevant premises behind the normative concept of NFE. The next section of this chapter begins with the role of responsibility. Responsibility in various types, forms and levels is considered crucial in a sound moral development of economic behaviour. As opposed to the premise of the ‘homo economicus’ of traditional economics, a market economy where individuals and stakeholders do not take responsibility for society at large is morally diverted and retarded. The final two sections describe two more premises that are explicitly defined as a normative point of departure for the concept of NFE.

Responsibility

Taking responsibility for both your own life and society is the starting point of new financial ethics. Responsibility of the organisation for society is not primarily a political and/or legal matter – it’s a personal matter. This concerns all stakeholders and participants in society. This introductory chapter starts off with the conventional – relatively new – but already rich literature in the areas of social, moral and economic responsibility of the company. The research field of corporate social responsibility (CSR) has developed in a short period of time in line with required management practice. The result is that some focus of management has shifted to specific elements of CSR and the initial premise – moral responsibility – has almost fallen into oblivion. What is ‘right’ was no longer determined by ethical values and moral accountability, but more by the degree of acceptance of certain social standards by companies themselves. The consequence is that in recent years, several scandals have occurred in organisations where CSR policies were explicitly anchored. It shows that although CSR initiatives were useful, they are not sufficiently effective to keep companies morally responsible for their behaviour. In the business practice of recent years, the strange situation has developed that ‘socially responsible’ is not necessarily similar to ‘morally responsible’, let alone ‘liable’. Cultural differences between companies and societies imply complex interpretations of what is a ‘right’ or ‘just’ action. To emphasise the crucial role of responsibilities at different levels, the following subsections discuss three main types of responsibility in the literature.

Social responsibility

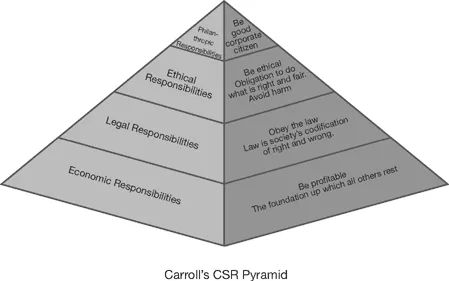

The best-known traditional definition of social responsibility is that of Carroll. More specifically he refers to the ‘social responsiveness’ of business, as a method to respond to social pressure. The four-part definition2 of Carroll states:

The social responsibility of business encompasses the economic, legal, ethical and discretionary expectations that society has of organizations at a given point in time.

Carroll, 1979, p. 500

Carroll’s vision from 1979, based on his previous publications, provided a thorough definition of corporate social responsibility in four categories of corporate performance. Please note that there is an overlap between the different categories. He distinguishes:

• Economic responsibilities: above all, a company has the responsibility to profitably sell goods and services needed by society.

• Legal responsibilities: society expects from a company that they will not only take economical responsibility, but will also respect the legal environment as established in the region wherein they operate.

• Ethical responsibilities: in addition to legal and statutory responsibilities, there are also rules, norms and values less clearly established or not established at all. Because these principles are broadly defined, they are the most difficult area for the company. However, this is often expected from its prejudice.

• Discretionary responsibilities: these responsibilities are not set at all; they are voluntary and open to review in the hands of the company itself. Though it can be asserted that these responsibilities are therefore not responsibilities at all, society does have its moral expectations of companies (Carroll, 1979, p. 500).

In a later work published in 1983, Carroll replaced discretionary responsibilities by social responsibilities. By this, he meant the voluntary or philanthropic actions of an enterprise consisting of donations of money, time and talent to the society in which it operates (Carroll, 1983, p. 604; Carroll, 1999, p. 286). In 1991 he included his four-part definition of social responsibility in a CSR pyramid, as shown in Figure 1.2.

This model was further developed with the views and cooperation of Mark S. Schwartz on social responsibility at the beginning of this century. Because of the voluntary and discretionary nature of philanthropic responsibilities, both authors had decided that this category is no longer an element of social responsibility (Schwartz and Carroll, 2003, p. 505). Instead, this category is considered now as an economic and/or ethical responsibility. The first motivation is that it is difficult to distinguish between philanthropic and ethical responsibilities. Second, philanthropic responsibilities could simply be based on economic interests (Schwartz and Carroll, 2003, p. 506). Another reason for the pyramid not always being reliable is the fact that responsibilities are not (for example) purely economic or purely legal – there could easily be overlap involved. Hence the new CSR approach consisted of a Venn diagram showing the different categories only partially overlapping each other. This no longer gives the impression that one class is more important than another.

Figure 1.2The four-part definition o...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Table of Contents

List of figures

List of tables

List of boxes

Foreword

Preface

Part I Introduction

Part II Economic playing field

Part III The new financial ethics model

Part IV Applications

References

Author index

Subject index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access New Financial Ethics by Aloy Soppe in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.