Originally published in 1906, this volume presents a commercial review of the conditions and prospects of the iron and steel trades of Great Britain and its foreign competitors at the turn of the twentieth century. This title will be of interest to students of business and economics, as well as economic historians.

IT is impossible to do more than give a perfunctory and imperfect summary of the vast ironmaking resources and magnificent development of the United States. The subject has been referred to elsewhere in the present volume in relation to various cardinal and controlling aspects of the trade; but a few additional particulars seem to be called for here.

It would be little short of ridiculous, however, to attempt to give even the outlines of the history of the development of the American iron industry. Every branch of that great organisation has a record of engrossing interest, whether regarded as a series of struggles against what seemed to be unfavourable conditions, or as a consequent series of triumphs over mechanical and financial difficulties, geographical and topographical conditions that were not suited to the requirements of the time, the imperfect organisation and education of labour, and isolation from the great markets of the world at a period when it took fifty to sixty days to cross the Atlantic.

In the year 1854 the total production of pig iron throughout the world was about 6,000,000 tons.1 Of that quantity 3,000,000 tons were produced in Great Britain and only 750,000 tons in the United States, which latter country consequently produced only 12

per cent. of the whole. In the period 1871–85, the average annual production of pig iron by the United States had risen to 18·7 per cent. of that of the world generally. In the period 1886–96 the proportion had increased to 30·9 per cent., and during the last three years the United States have provided about 46 per cent. of the world’s total supply.

This remarkable progress has been due to a variety of circumstances, some natural, some adventitious, of which the most commanding have been the vast coal and iron-ore resources of the Republic, the exceptional resourcefulness of the Americans in invention and in the capacity to excel, the accommodating character of American labour, and last, but not least, the encouragement given to industrial enterprise by the Customs tariff. The exceptionally great distances which Nature has interposed between the ore of Lake Superior and the coal of Pennsylvania have been overcome by methods of transportation that have set an example to the rest of the world, and have eclipsed all previous records in economy. The organisation of industry in iron-ore mines and cokeries, at blast furnaces, and in steelworks, has been carried out on a scale of magnitude never before approached. In the mechanical handling of materials, results have been achieved which for many years were regarded with incredulity by the slower-moving people of Europe. Finally, America has become more or less the academy to which all other ironmaking nations have resorted for both precept and example not to be elsewhere secured.

For the first hundred years of its career, however, the American iron trade moved but slowly. That was a natural result of a sparse and limited population, a vast domain, much of which was a wilderness, attempts at repression and discouragement by the mother country, an imperfect acquaintance with the technique of the ironmaking arts, and a firmly grounded belief that agriculture alone was to maintain the country in a condition of high prosperity. From this unfavourable situation the railway and the steamship gradually relieved the trade. The railway demands that began to assume considerable proportions between 1860 and 1875, led to a notable increase of enterprise. In the period 1871–85 the total quantity of pig iron made in the United States was 46,000,000 tons, and in the next ten years the output had grown to 86·4 million tons; but the upward movement culminated with an output of over 18,000,000 tons in 1903 alone.

The principal factor in enabling this progress to be achieved was the discovery and development of the iron ores of the Lake Superior ranges and of the coking coal of the Connellsville region in Western Pennsylvania. Not, however, that these were the only sources of supply. Indeed, the returns for 1902 show that in that year hard ores were mined in seventeen, and soft ones in twenty-two, states and territories. But four-fifths of the total is now produced on Lake Superior from 133 mines, of which forty-eight on the Mesabi Range contribute well on to one-half. The resources of this region have been computed as equal to the maintenance of the present rate of consumption for more than sixty years.

The coke supplies of the United States are mainly obtained from the Connellsville district, about an average of fifty miles from Pittsburg. The coke is produced at considerably less than any similar product in Europe, and the freight to the blast furnaces in or around Pittsburg is about 4s. a ton. In some years a large part of this coke was sold at about a dollar a ton at the ovens, when similar coke in South Durham was costing 8s. to 12s. at ovens. The average price is, however, nearer 7s. per ton at the ovens in West Pennsylvania. The coke supply there is ample for many years to come.

As late as 1810 there were produced in the whole country only 917 tons of steel, Pennsylvania’s share being 531 tons, or more than half of the whole. It is remarkable that the Keystone State still makes about the same relative percentage. Even in 1831 the production of steel was only 1,600 tons, an amount which was said then to equal the whole quantity imported, so that the market for steel was divided equally with the foreigner seventy years ago. But this steel was made chiefly by cementation; crucible steel was to come later. From 1831 until as late as 1860 very little progress was made in developing the manufacture of steel. The total product in 1850 was only 6,000 tons. In 1840 Isaac Jones and William Coleman began its manufacture in Pittsburg, and succeeded. Singer, Nimick, & Co., in 1853, produced successfully the usual grades of cast steel for saws, machinery, etc., and for kindred purposes. Hussey, Wells, & Co., in 1850, made the first crucible steel of first quality as a regular product obtained from American iron, and in 1862 came Park Brothers & Co., with the biggest steel plant of all up to that time. Several hundred English workmen were imported by this firm to ensure success. All these concerns were in Pittsburg.

In 1873 the United States produced 198,796 tons of steel; Great Britain, their chief competitor, 653,500 tons, more than three times as much. Twenty-six years later, 1899, the United States production was more than double that of Great Britain, the figures being 10,639,957 and 5,000,000 tons respectively, an eight-fold increase for Britain and fifty-three-fold for the United States.

The present centre of U.S. steel is the square made by a line drawn from Pittsburg to Wheeling, northward to Lorain, eastward to Cleveland, and south again to Pittsburg. In this territory most of the steel is made. Allegheny County alone (Pittsburg) in 1899 produced nearly one-quarter of all the pig iron in the United States, almost half of the open-hearth steel, and about 39 per cent. of the total production of all kinds of steel. As late as the middle of the last century the Eastern States upon the Atlantic constituted the home of steel manufacture. Even in Pennsylvania one-half of all the steel was made east of the Alleghany Mountains. Since then the trend has been constant and rapid to the region known as the Central West, which has Pittsburg as its metropolis.

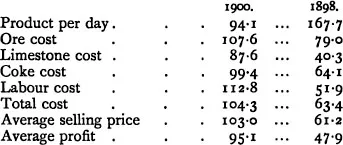

The remarkable changes that have been accomplished in the pig-iron-making conditions of the United States have been put by Mr. C. Kirchhoff, of New York, in his Presidential Address to the American Institute of Mining Engineers in a statistical form which brings them readily home. These figures are summarised in the following short table, taking the year 1889 as 100, all expressed in percentages of that figure:—

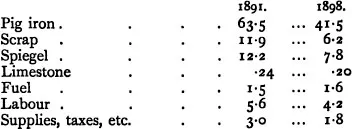

The comparative cost of steel ingots as between 1891 and 1898, fell as shown in the following figures, taking the year 1889 as 100, expressed in percentages of that figure:

The main cause, apart from exceptional natural resources, of the vast progress achieved by the iron and steel industries of the United States is the enormous extent of the home market. The American consumption of steel per capita has gone up from 20 lb. to 500 lb. within less than half a century. The cheapening of the product has stimulated the demand for steel to an extent that would not have been deemed possible only a quarter of a century ago. New sources of demand have opened up in every direction, and with amazing rapidity. While railway demands have naturally all along been the most considerable in a country that has a total extent of railway lines fully equalling that of the whole of Europe, the requirements of agriculture—fencing, implements, etc.—and of every other interest, have called for continually increasing supplies. Within five years the demand for rolling stock alone has risen from almost a minus quantity to nearly 800,000 tons a year. Within ten years the demands of the tin-plate industry have advanced from less than 5,000 tons to about 500,000 tons annually. Within the same short interval building demands have more than trebled, and there are now but few structures that do not make use of steel skeletons.

The most prominent commercial features of the American steel industry during the last fifteen years may be thus specified:—

1. An enormous expansion of output in every direction, culminating in the doubling or more of the production of both pig iron and steel and the various products thereof.

2. A constant increase in the relative proportions of pig iron and steel, leading to the proportion of crude steel to the pig-iron product being advanced from 46 per cent. in 1890 to about 80 per cent. at the present time.

3. An increase of 200 per cent. to 300 per cent. in the amount of product obtained from a given plant within a given time, alike at blast furnaces and in steelworks.

BLOOMING MILL AT THE DIFFERDINGEN WORKS, GERMANY

4. A remarkable reduction in the cost of labour per unit of product all over the country.

5. An unprecedented reduction in the cost of producing both pig-iron and steel products, whereby both costs and selling prices in the United States were for the first time brought below those of Europe.

6. A long period of depression under the influence of which these results were made possible by the strictest economy and mechanical and economic advances all along the line. (This period lasted from 1891 to 1898.)

7. A succeeding period of inflation, during which trusts and syndicates were established in every branch of the trade, culminating in the United States Steel Corporation—a merger of most of the great iron and steel producing concerns in the country with its capital of £280,000,000 sterling and its 170,000 operatives.

8. A strong and strenuous rivalry between the Steel Corporation and independent firms, which is still in progress, and of which the end is yet far to seek.

9. A notable appreciation in the value and the costs of raw materials, which appears likely to be maintained, due to the realisation of the fact that while the demand for steel may be indefinitely extended, the available supplies of iron ore and coking coal are fixed quantities, incapable of replacement or substitution.

10. A keen and watchful rivalry on the part of the leading manufacturing interests to keep in the front of mechanical advances and up-to-date conditions all round, leading to the attainment of much more remarkable results than have been attained in any other country.

On some of the more recent characteristics of the American steel trade I shall have occasion to speak later on.

GERMANY

While the manufactures of both iron and steel had been carried on in Germany during the Middle Ages, from the end of the Crusades to the beginning of the Thirty Years’ War, yet the industry on an important scale is very modern—so much so, indeed, that the output of iron ores has increased nearly five-fold within the last thirty years. Fifty years ago the empire of to-day did not produce half a million tons of pig iron annually, while in 1904 the output was nearly ten and a half million tons, or more than twenty times as much. The output of steel has made still more remarkable strides. In 1850 the total German output of steel was less than 12,000 tons, whereas in 1904 it was close on 8,500,000 tons, or 700 times as much.

This remarkable growth has been mainly accomplished during the last ten years, and it is still proceeding at a pace which guarantees the attainment of much greater dimensions in the near future.

Germany has more abundant and valuable sources of domestic iron ores than any other European (continental) country except Spain, and probably even Spain has not the same volume of ores as that known to exist in the provinces of Alsace and Lorraine. Germany has also a great abundance of good coal, especially in Westphalia. So far her natural resources are excellent. But the ore and the fuel are more than a hundred and fifty miles apart, and can only be connected by the payment of railway rates to the tune of about 7s. per ton of material carried in either direction. The small coal-field of the Saar is nearer to Alsace than Westphalia, but it does not provide such good coke, nor in sufficient quantity.

Germany has five principal iron-mining centres, severally tabulated as Bonn, Breslau, Clausthal, Luxembourg, and Lorraine. Of these five, two alone—Luxembourg and Lorraine—produce 80 per cent. of the total iron-ore output of the country, which in 1903 was about twenty million tons, and is officially computed as of an average value of 3·6 marks per ton, the average value of the ores of the two principal districts being only about 2·5 marks (2s. 6d.) per ton at the place of production. In the district of Bonn, however, more than two million tons are still produced of a higher quality of ore; the average value is stated at 10s. 6d. to 13s per ton; and in the districts of Breslau and Clausthal the average value of the output—less than a million tons for both—is from 4s. 3d. to 6s. 3d. per ton. The average yearly output of iron ore per miner employed in Luxembourg and Alsace-Lorraine ranges from 440 to 460 tons a year.

Germany, like England, has of late years required to supplement her own iron-ore output by constantly increasing imports from other countries. In 1870 those imports amounted to only about 300,000 tons; in 1880 they wer...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Original Copyright Page

Table of Contents

INTRODUCTION AND OUTLINE

I. A SHORT HISTORICAL RETROSPECT

II. SUPPLIES OF RAW MATERIAL

III. THE IRONMAKING DISTRICTS OF GREAT BRITAIN

IV. BRITISH PIG-IRON-MAKING CONDITIONS

V. THE MANUFACTURE OF FINISHED IRON

VI. THE BESSEMER STEEL INDUSTRY

VII. THE OPEN-HEARTH STEEL INDUSTRY

VIII. THE BASIC AND CRUCIBLE STEEL INDUSTRY

IX. THE CHIEF FOREIGN IRONMAKING COUNTRIES

X. SOME PROMINENT CONDITIONS OF THE BRITISH IRON TRADE

XI. TRANSPORTATION OF MATERIALS

XII. LABOUR CONDITIONS AND REMUNERATION

XIII. HOME MARKETS AND SOURCES OF DEMAND

XIV. BRITISH COLONIAL MARKETS

XV. BRITAIN’S FOREIGN TRADE

XVI. DUMPING CONDITIONS AND INTERNATIONAL COMPETITION

XVII. PRICES AND PROFITS IN THE IRON INDUSTRY

XVIII. THE RANGE AND REGULATION OF PRICES

XIX. TRUSTS, CARTELS, AND SYNDICATES

XX. INFLUENCE OF CUSTOMS TARIFFS

XXI. THE COMMERCIAL OUTLOOK

APPENDIX

INDEX

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Iron Trade of Great Britain by J. Stephen Jeans in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.