III The Money Supply Process and the Use of Monetary Instruments, 1963–74

The BCEAO area is open to trade and payments, which sets obvious limits on how far it can have an independent monetary policy because the balance of payments outcome is almost exogenously determined by production and prices of exports. This is evident from the factors affecting the money supply.

Growth in the Money Supply

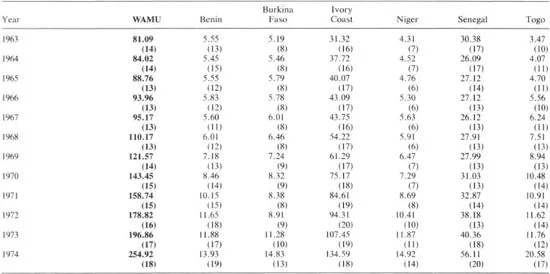

Data on money supply growth in the BCEAO area, as well as in individual member countries, between 1963 and 1974 shows that for the area as a whole the average annual rate of growth (in simple arithmetic terms) was 29 percent (Table 2). Senegal had the lowest relative growth (17 percent) and Togo the highest (54 percent), but in absolute terms the growth in the money supply of Ivory Coast contributed most—nearly 60 percent—of the increase in the money supply in the area, followed by Senegal (15 percent).

Table 2. WAMU and Members: Money Supply, 1963–74

(Quarterly averages: in billions of CFA francs)

Note: The money supply is defined as currency plus demand deposits. Figures in parentheses are ratios of the money supply lo GDP.

Source: International Monetary Fund, International Financial Statistics (Washington: IMF).

The relatively high rate of increase of the money supply in Ivory Coast reflects its rapid GDP growth in the post-independence period. It may also reflect a relatively faster monetization, since the ratio of its nonmonetary to monetary GDP declined from 22 percent in I960 to 13 percent in 1974. Although the absolute level of the money supply was about the same in Ivory Coast and Senegal at the beginning of the period, by 1974 the level in Ivory Coast was more than twice that in Senegal. In Togo, on the other hand, the money supply grew fast from a small base. For the area as a whole, the ratio of the money supply to GDP declined somewhat between 1963 and 1968, to increase between 1969 and 1974. In Ivory Coast, however, the ratio continued to increase until 1972 and declined in the later two years, while in Senegal it generally declined until 1972 and increased in the later two years.

The rate of growth in the money supply accelerated considerably during 1974 in all the countries in the Union. In the area as a whole, the average annual rate of growth reached nearly 30 percent—more than twice the average annual rate of 14 percent between 1963 and 1973. There were similar trends in each member country. As will be discussed in Section IV, the sharp acceleration in the money supply during 1974 had some important implications for the adequacy of the old statutes of the BCEAO for the conduct of monetary policy. The following analysis, which isolated the different contributions made to money supply growth of components of the money multiplier and the money base, found that the sharply higher money supply growth was primarily due to higher liabilities.

Analysis

The money supply consists of a money multiplier and a base (Frost, 1977). Although the latter can be defined in different ways, depending upon the degree of financial sophistication in a country, a simple definition—currency plus public and bank reserves—is appropriate in the case of the BCEAO countries. Between 1962 and 1974, the BCEAO did not prescribe any reserve requirements (which might have complicated the calculation of the reserve component of the base), and generally provided easy access to its rediscount facilities.

The money supply may then be seen as reflecting both the behavior of the monetary authorities (via the monetary base) and the behavior of the private sector, including banks (via the money multiplier). The monetary authorities affect liabilities by changing the assets of the central bank—through its credit to governments, and changes in foreign and other assets. Since changes in government credit as well as in foreign assets could be regarded as being outside the control of the BCEAO, the behavior of the monetary authority would then be reflected in the changes in the other assets in the Bank’s portfolio. Private behavior, on the other hand, could be analyzed in terms of the changes in factors affecting the money multiplier (defined as the ratio of currency to the money supply and the ratio of bank reserves to deposits). On the basis of these considerations, the money supply (A/) (the sum of currency with the public (C) and demand deposits (D)) is related to the monetary base, or monetary liabilities (L) (currency with the public plus central bank reserves (R)), by a multiplier, k (k = 1/(c + r(1 – c)), where c and r are the ratios of currency to the money supply and of reserves to demand deposits, respectively. Changes in the money supply over discrete intervals of time may then be described in terms of first differences:5

From Mt−1 = kt−1 · Lt−1 and substituting in (1),

The last term, representing the interaction of changes in k and L, will normally be insignificant for small variations.

Changes in the monetary liabilities of the central bank are caused by corresponding changes in its assets: these are net foreign assets (F), net credit to the government (DG), and the balance of asset changes (LP)—or total changes in assets less changes in F and DG The latter are deemed to be a potential policy variable. In the case of the BCEAO, this last change will generally be brought about by variations in total rediscounted bills issued by the commercial banks.

Changes in the money multiplier. Δk, may be decomposed into changes due to variations in the currency to money ratio, ΔKc, and to changes in the reserve to demand deposit ratio, Δkr. Thus,

where:6

and

Finally, equation (2) may be subdivided into the various components identified as affecting the money supply:

where the subscripts to M refer to the causal factors of the change—with the first term in parentheses on the right-hand side approximating the effects of the change in money multiplier and the second approximating the impact of the changes in monetary liabilities.

Following this analytical framework, changes in the money supply can be broken down into changes attributable to variations in the money multiplier and to the changes in the monetary liabilities of the BCEAO (Table 7 in the Statistical Appendix). Of these two determinants of the money supply, cumulative (yearly) changes in the money multiplier accounted for only 12 percent of the increase in the money supply in the group (although there were some individual years, particularly in the early 1960s, when the money multiplier had more impact). Monetary liabilities also had a greater impact on the money supply in individual countries, although this varied from accounting for 70 percent of changes in the money supply in Senegal to as much as 98 percent in Niger.

The relative importance of changes in monetary liabilities for variations in the money supply is not surprising, given that the habit of using banks and monetary institutions in these countries continued to expand between 1963 and 1974. On the other hand, the money multiplier is predominantly influenced by fluctuations in the currency ratio that are caused mainly by changes in commercial output and export prices, which tend to have “cyclical” or weather-influenced fluctuations. In a year with a good agricultural season, for instance, the consequent rise in farmers’ incomes leads to increased currency holdings (since banking habits are less developed in the rural areas). Over a period, however, these fluctuations tended to cancel each other out and the trend influence of the changes in the currency ratio on the money multiplier was small, as was, therefore, its relative influence on the money supply. The relatively high currency ratio also almost completely swamped the effects of the changes in the reserve ratio on the money multiplier.

The fluctuations in monetary liabilities also seem to have been the most important influence upon the changes in the money supply when the series is adjusted for trend. In Tables 8 and 9 in the Statistical Appendix, total changes in the money supply in the entire WAMU area and in Ivory Coast are divided between trend and cyclical changes, as are the influences of the changes in monetary liabilities and the money multiplier on those in the money supply. Ignoring algebraic signs, the changes caused by the money multiplier accounted for less than 20 percent of the total change in the money supply (uncorrected for trend), and for about 30 percent for the trend-corrected series as well as for the cyclical-corrected series. (A comparable analysis for other member countries yielded similar, though somewhat less pronounced, results.)

While the trend influence of the changes in the money multiplier tended to reinforce the trend influence of the changes in monetary liabilities on the money supply, their respective cyclical contribution was conflicting in all but two years in the BCEAO area as a whole and in all but three years in Ivory Coast. Thus, a cyclical increase in liabilities was accompanied by a dampening of the value of the money multiplier and vice versa. These opposing cyclical influences explain the relatively smaller influence of the cyclical changes on the money supply in comparison with the impact of trend changes. The offsetting cyclical behavior of liabilities and the money multiplier is perhaps not surprising. When base money increases abruptly, both the cash ratio and reserve ratio may be expected to rise in the short run until the public and the banks have had time to adjust their asset portfolio to the new circumstances.

Changes in the monetary liabilities of the BCEAO have been the predominant trend and cyclical influence on the changes in the money supply. In the BCEAO area, liability changes may be attributable to changes in net foreign assets and in net credit to governments (both of these create corresponding changes in domestic monetary liabilities), and, as a residual, in changes in the monetary liabilities corresponding to changes in other assets (Table 10 in the Statistical Appendix). At least theoretically, these residual effects could be considered as controllable by policy (through, for instance, the rediscount policy).

For the period considered, the influence of changes in credit to governments was minimal; such credit was rigorously limited by the statutes of the BCEAO which governed not only the amount, but also the duration of the credit. Of the remaining two components, the average impact of the changes in net foreign assets was slightly below half, and that of the potentially policy controllable liabilities slightly above half, of the total change in the money supply attributable to the change in monetary liabilities. Moreover, in all but three years, foreign assets and residual assets had an offsetting influence on the money supply in the area as a whole, indicating either an increased causal and negative relationship between them or an attempt by the BCEAO to use the policy controllable assets to dampen the effects of changes in foreign assets on the money supply. However, the latter seems unlikely; there is little other evidence of conscious attempts to regulate credit in the light of changes in foreign assets, and the negative relationship between the two types of asset is only consistently evident in two individual member countries. Furthermore, even in the case of Senegal, the cumulative negative impact of the changes in foreign assets was more than offset by the cumulative positive impact of the changes in potentially policy controllable variables, so neutralizing developments may have been fortuitous. This question of the passivity of credit policy is elaborated in the following section.

The results of an analysis into the impact of the components of the money multiplier sho...

Table of contents

Cover Page

Title Page

Copyright Page

Contents

Prefatory Note

I The West African Monetary Union and the Theory of Currency Unions

II The Central Bank of West African States, 1962–74: Its Structure and Functions

III The Money Supply Process and the Use of Monetary Instruments, 1963–74

IV Credit Inflation and the Reform of the Monetary Union, 1974