Against a background of extraordinary growth in the popularity of betting and gaming across many countries of the world, there has never been a greater need for a study into gambling's most important factor - its economics.

This collection of original contributions drawn from such leading experts as David Peel, Stephen Creigh-Tyte, Raymond Sauer and Donald Siegel covers such interesting themes as:

*betting on the horses

*over-under betting in football games

*national lotteries and lottery fatigue

*demand for gambling

*economic impact of casino gambling

This timely and comprehensive book covers all the bases of the economics of gambling and is a valuable and important contribution to the ongoing and growing debates. The Economics of Gambling will be of use to academics and students of applied, industrial and mathematical economics as well as of being vital reading for those involved and interested in the gambling industry.

- 288 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Economics of Gambling

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Subtopic

Business GeneralIndex

Business1 Introduction

Leighton Vaughan Williams

When I was asked to consider putting together an edited collection of readings on the theme of the ‘Economics of Gambling’, I was both excited and hesitant. I was excited because the field has grown so rapidly in recent years, and there is so much new material to draw upon. I was hesitant, however, because I knew that a book of this nature would not be truly satisfactory unless the papers included in it were new and hitherto unpublished.

The pressures of time on academics have perhaps never been greater, and it was with this reservation in mind that I set out on the task of encouraging some of the leading experts in their fields to contribute to this venture. In the event, I need not have worried. The camaraderie of academics working on the various aspects of gambling research is well known to those involved in the ‘magic’ circle, but the generosity of those whom I approached surpassed even my high expectations.

The result is a collection of readings which draws on expertise across the spectrum of gambling research, and across the global village. The papers are not only novel and original, but also set the subject within the existing framework of literature. As such, this book should serve as a valuable asset for those who are coming fresh to the subject, as well as for those who are more familiar with the subject matter. Topics covered include the efficiency of racetrack and sports betting markets, forecasting, lotteries, casinos, betting behaviour, as well as broad literature reviews. The twenty-nine contributors hail from nineteen academic institutions, as well as government service, from as far afield as the UK, USA, Australia, Canada, Israel and Ireland.

In many cases, the contributions would, in my opinion, have gone on to be published in top-ranked journals, but the authors lent their support instead to the idea of a single volume that would help promote this field of research to a wider audience. In all the cases, the authors have provided papers which are valuable and important, and which contribute something significant to the burgeoning growth of interest in this area. It has been a joy to edit this book, and my deepest gratitude goes to all involved.

Most of all, though, my thanks go to my wife, Julie, who continues to teach me that there is so much more to life than gambling.

2 The favourite–longshot bias and the Gabriel and Marsden anomaly: An explanation based on utility theory

Michael Cain, David Peel and David Law

Introduction

Research on gambling markets has focused on the discovery and explanation of anomalies that appear to be inconsistent with the efficient markets hypothesis; see Thaler and Ziemba (1988), Sauer (1998), and Vaughan Williams (1999) for comprehensive reviews of the salient literature.

The best-known anomaly in the literature on horse-race gambling is the so-called ‘favourite–longshot bias’, where the return to bets on favourites exceeds that on longshots. This was first identified by Griffith (1949), and confirmed in the overwhelming majority of later empirical studies; see below for some further discussion. A second apparent anomaly was reported by Gabriel and Marsden (1990 and 1991), who compared the returns to winning bets in the British pari-mutuel (Tote) market with those offered by bookmakers at starting prices. They reported the striking finding that Tote returns to winning bets during the 1978 British horse-racing season were higher, on average, than those offered by bookmakers; even though, they suggested, both betting systems involved similar risks and the payoffs were widely reported. Consequently, they suggested that the British racetrack betting market is not efficient. As noted by Sauer (1998) in his recent survey, the Gabriel and Marsden finding calls for explanation. That is one of the main purposes of this chapter.

We will show that the relationship between Tote returns and bookmaker returns is more complicated than implied in the Gabriel and Marsden study. Whilst Tote pay-outs are higher than bookmakers for longshots, this is not the case for more favoured horses; also see Blackburn and Peirson (1995) for additional evidence consistent with this point. In addition, we argue that bets on the Tote are fundamentally different from bets with bookmakers since the bettor is uncertain of the pay-out. Whilst bettors have some limited information on the pattern of on-course Tote betting via Tote boards, off-course bettors have no such information and the pay-out is determined by the total amount bet. If Tote bettors did have full information on pay-outs, then, the fact that the Tote paid out £2,100 on winning bets of £1 in the Johnnie Walker handicap race at Lingfield on 12 May 1978 whilst the bookmaker SP odds were only 16 to 1, would in itself invalidate the usual economists’ notions of arbitrage processes and market efficiency. Assuming, then, that the Tote pay-out is uncertain whilst bookmaker returns are essentially certain, expected returns will be equalised only if the representative punter is risk-neutral, an assumption implicit in Gabriel and Marsden, and in previous analyses of the relationship between Tote and bookmaker returns; see, for example, Cain et al. (2001). However, the assumption that the representative bettor is risk-neutral is not consistent with the stylised fact derived from empirical work on racetrack gambling, that there is a favourite–longshot bias; bets on longshots (low-probability bets), have low mean returns relative to bets on favourites, or high probability bets. This has been documented by numerous authors for both the UK (book-maker returns) and for the US pari-mutuel system (see, e.g., Weitzman, 1965; Dowie, 1976; Ali, 1977; Hausche et al., 1981 and Golec and Tamarkin, 1998). The standard explanation for this empirical finding has been that the representative punter is locally risk-loving; see, for example, Weitzman (1965) and Ali (1977). However, Golec and Tamarkin (1998) have recently shown for US pari-mutuel data that a cubic specification of the utility function, of the Friedman and Savage (1948) form, that admits all attitudes to risk over its range, provides a more parsimonious explanation of the data than a risk-loving power utility function with exponent greater than unity. We will show that, if the representative bettor is not everywhere risk-neutral, an explanation of both the observed relationship between Tote and bookmaker returns and the favourite–longshot bias can still be provided. This is the second main aim of the chapter.

Theoretical analysis

Utility and the favourite–longshot bias

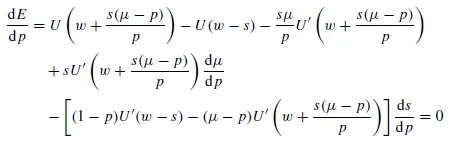

It is assumed that the representative bettor has utility function, U(⋅) and total wealth, w. With odds against winning of o and win probability, p, the expected pay-out to a unit bet is μ = p(1 + o) + (1 – p)0 = p(1 + o) and hence o = (μ/p) – 1 = (μ – p)/p. If the punter stakes an amount s, the expected utility of return is

E = E(U) = pU(w + so) + (1 – p)U(w – s)

The optimal stake for the punter is such that (əE/əs) = 0 and (ə2E/əs2) < 0 so that

and s = S(μ, p; w){if E > U(w)}. Substituting s = s(μ, p) into equation (1) gives expected utility, E, as a function of μ and p, and hence we may obtain an indifference map in (μ, p) space. It is thus possible to differentiate equation (1) with respect to p and equate to zero in order to find the combinations of expected return, μ, and probability, p, between which the bettor is indifferent. This produces

and hence, in view of equation (2), equation (3) reduces to

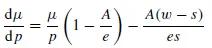

so that

where

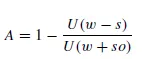

When w = 1 = s, the assumption made by Ali (1977) and Golec and Tamarkin (1998), equation (5) simplifies to

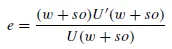

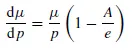

If U(0) = 0, then equation (6) reduces to

where e = e(X) = e(μ,/p) is the elasticity of U(⋅) at X = μ/p. Observe from equation (7) that the slope of the equilibrium expected return–probability frontier will be positive (or negative) depending on whether the elasticity is greater than (or less than) unity. Clearly, with a power utility function which is everywhere risk-loving, the (μ, p) frontier will be everywhere upward sloping – the traditional favourite–longshot bias.

A condition for the favourite–longshot bias is that (dμ/dp) > 0, in order that the mean return–probability relationship is not constant or declining throughout its range. It is perhaps surprising to find that this condition is consistent with a utility function that is not everywhere risk-loving over its range.

As an illustration, consider the utility functi...

Table of contents

- Cover Page

- Title Page

- Copyright Page

- Figures

- Tables

- Contributors

- 1 Introduction

- 2 The favourite–longshot bias and the Gabriel and Marsden anomaly: An explanation based on utility theory

- 3 Is the presence of inside traders necessary to give rise to a favorite–longshot bias?

- 4 Pari-mutuel place betting in Great Britain and Ireland: An extraordinary opportunity

- 5 Betting at British racecourses: A comparison of the efficiency of betting with bookmakers and at the Tote

- 6 Breakage, turnover, and betting market efficiency: New evidence from Japanese horse tracks

- 7 The impact of tipster information on bookmakers’ prices in UK horse-race markets

- 8 On the marginal impact of information and arbitrage

- 9 Covariance decompositions and betting markets: Early insights using data from French trotting

- 10 A competitive horse-race handicapping algorithm based on analysis of covariance

- 11 Efficiency in the handicap and index betting markets for English rugby league

- 12 Efficiency of the over–under betting market for National Football League games

- 13 Player injuries and price responses in the point spread wagering market

- 14 Is the UK National Lottery experiencing lottery fatigue?

- 15 Time-series modelling of Lotto demand

- 16 Reconsidering the economic impact of Indian casino gambling

- 17 Investigating betting behaviour: A critical discussion of alternative methodological approaches

- 18 The demand for gambling: A review

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Economics of Gambling by Leighton Vaughan-Williams in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.