- 560 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

In the years since it first published, Neuroeconomics: Decision Making and the Brain has become the standard reference and textbook in the burgeoning field of neuroeconomics. The second edition, a nearly complete revision of this landmark book, will set a new standard. This new edition features five sections designed to serve as both classroom-friendly introductions to each of the major subareas in neuroeconomics, and as advanced synopses of all that has been accomplished in the last two decades in this rapidly expanding academic discipline. The first of these sections provides useful introductions to the disciplines of microeconomics, the psychology of judgment and decision, computational neuroscience, and anthropology for scholars and students seeking interdisciplinary breadth. The second section provides an overview of how human and animal preferences are represented in the mammalian nervous systems. Chapters on risk, time preferences, social preferences, emotion, pharmacology, and common neural currencies—each written by leading experts—lay out the foundations of neuroeconomic thought. The third section contains both overview and in-depth chapters on the fundamentals of reinforcement learning, value learning, and value representation. The fourth section, "The Neural Mechanisms for Choice, integrates what is known about the decision-making architecture into state-of-the-art models of how we make choices. The final section embeds these mechanisms in a larger social context, showing how these mechanisms function during social decision-making in both humans and animals. The book provides a historically rich exposition in each of its chapters and emphasizes both the accomplishments and the controversies in the field. A clear explanatory style and a single expository voice characterize all chapters, making core issues in economics, psychology, and neuroscience accessible to scholars from all disciplines. The volume is essential reading for anyone interested in neuroeconomics in particular or decision making in general.

- Editors and contributing authors are among the acknowledged experts and founders in the field, making this the authoritative reference for neuroeconomics

- Suitable as an advanced undergraduate or graduate textbook as well as a thorough reference for active researchers

- Introductory chapters on economics, psychology, neuroscience, and anthropology provide students and scholars from any discipline with the keys to understanding this interdisciplinary field

- Detailed chapters on subjects that include reinforcement learning, risk, inter-temporal choice, drift-diffusion models, game theory, and prospect theory make this an invaluable reference

- Published in association with the Society for Neuroeconomics—www.neuroeconomics.org

- Full-color presentation throughout with numerous carefully selected illustrations to highlight key concepts

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Part I

The Fundamental Tools of Neuroeconomics

Outline

Chapter 1 Basic Methods from Neoclassical Economics

Chapter 2 Experimental Economics and Experimental Game Theory

Chapter 3 Computational and Process Models of Decision Making in Psychology and Behavioral Economics

Chapter 4 Estimation and Testing of Computational Psychological Models

Chapter 5 Introduction to Neuroscience

Chapter 6 Experimental Methods in Cognitive Neuroscience

Chapter 7 Evolutionary Anthropological Insights into Neuroeconomics

Chapter 1

Basic Methods from Neoclassical Economics

Andrew Caplin and Paul W. Glimcher

Much of neuroeconomics rests on an understanding of basic microeconomic thought. This chapter presents a concise overview of the main threads in modern economic studies of decision making. Beginning with a review of the history of both pricing theory and choice theory, the chapter describes the Marginal Revolution. It then goes on to develop Samuelson’s fundamental Revealed Preference approach and the notion of axiomatic proof. Several of the most important theories that grew from Samuleson’s work, including Expected Utility Theory, are described. The chapter concludes with a discussion of how axiomatic modeling approaches can be used as powerful tools in neuroscientific/neuroeconomic research by describing axiomatic studies of dopamine function.

Keywords

Microeconomics; Expected Utility Theory; axioms; economic theory; dopamine; choice

Outline

Introduction

Rational Choice and Utility Theory: Some Beginnings

Early Price Theory and the Marginal Revolution

Early Decision Theory and Utility Maximization

The Ordinal Revolution and the Logic of Choice

Quantitative Tests of Qualitative Theories: Revealed Preference

GARP

Understanding Rationality

Axiomatic Approaches: Strengths

Axiomatic Approaches: Weaknesses

Expected Utility Theory

Defining the Objects of Choice: Probabilistic Outcomes

Continuity Axiom

Independence

The Expected Utility Theorem

Axioms and Axiomatic Reasoning

Using Axioms: The Neoclassical Approach in Neuroeconomics

The Reward Prediction Error Hypothesis

The DRPE Axioms and the Ideal Data Set

Concluding Remarks

References

Introduction

A basic introduction to the economic theory of choice is crucial for those starting out in the field of neuroeconomics. One reason for this is that the theory involves abstractions, such as “utility functions,” that are of first-order importance in organizing our understanding of choice behavior. Another reason is that it provides tools for testing theories of choice against data. The third reason is even more fundamental. A history of the economic theory of choice carries lessons for the evolution of neureconomics that will both help shape the field in the coming decades and will allow neuroeconomists to avoid critical errors that crippled early economists in their studies of human choice behavior. Those who study behavior from the economic point of view have introduced not only specific models and tests but also some remarkable methodological advances, all of which can be leveraged by modern neuroeconomists. For all of these reasons a deep understanding of this “economic” way of thinking will prove increasingly important as the field matures.

One reason that economic methods are of such great value in neuroeconomics is that they are designed for relatively complex decision-making situations when compared to standard neurobiological tasks. Being forced to face-up to the complexities of decision making and social interaction has forced economic theorists to develop methods of a qualitative as well as a quantitative nature that are unique in the social and natural sciences. Over the centuries, economists have been forced to ask themselves again and again the question of whether or not they are approaching their questions from the right angle. As a result, they have developed methods that are ideal when one is qualitatively unsure about the appropriate modeling framework. That is particularly relevant because it is just the situation in which neureconomics finds itself today. The relationship between neural activity and decision making is just beginning to be unraveled. The fact that the theoretical underpinnings of neuroeconomics remain emergent, explains in part the appeal and importance of the methods and models of economic theory to neuroeconomists.

This chapter provides a short guide to some of the methods and models economists and others in related disciplines have developed in their struggle to systematize our understanding of choice behavior. The chapter is organized around the theory of utility maximization, often referred to as the theory of rational choice, because it is the centerpiece of contemporary economic theories of individual choice. The goal of this chapter is to show just how powerful and flexible these tools can be, and illustrate the help they may offer to those seeking to understand how neural phenomena and choice interact. A second goal of the chapter is to highlight some of the limitations of these approaches; limitations that can often be addressed or supplemented by the approaches from psychology, neuroscience and anthropology presented in the rest of this book. To those ends, we turn now to a highly selective tour through some of the highlights of the economic theory of individual decision making. In the process, we will encounter the general methods that economists have developed for testing their theories.

The first section of this chapter opens with a sketch of several early ideas in the economic theory of choice. That brings us, in section two, to the standard theory of utility maximization that achieved its mature form in the work of Vilfredo Pareto during the opening decades of the twentieth century. In section three we introduce the revealed preference approach to choice theory introduced by Paul Samuelson (1938). In section four we describe the expected utility theory of John von Neumann and Oskar Morgenstern (1944). In section five we present an illustration of how these methods can be used in contemporary Neuroeconomics, with a discussion of the Dopaminergic Reward Prediction Error Model.

Rational Choice and Utility Theory: Some Beginnings

One can view modern utility theory as deriving from two streams of thought in early economics: price theoretic and decision theoretic reasoning.

Early Price Theory and the Marginal Revolution

A key goal of traditional economics has always been to understand patterns in the prices and quantities of goods that are traded in markets. It is intuitively clear that these exchange-values, the prices people actually pay for things, must reflect a balance of forces between certain technologically impacted costs of production and some notion of use-value; how valuable and useful the goods are to those who are interested in obtaining them. But early researchers struggled to understand how these distinct notions of value (exchange-value, production costs, and use-value) could be related. Although it seemed obvious that the usefulness of a good must be an important determinant of how much someone would pay for that good (the exchange-value), it was unclear how this could be reconciled with the fact that relatively useless objects like diamonds were expensive, while life-necessities like water were essentially free.

David Ricardo (1817), perhaps the most important economist of the early nineteenth century, was a central figure in developing the earliest workable answer to these questions concerning the determination of prices. He focused the majority of his energies on studying the costs of producing objects, in the belief that the costs of production were central to determining exchange-value. He reasoned that the prices of those commodities produced by human effort were determined by the prices of the inputs necessary for their production, such as the price of labor and the price of, for example, land. In its crudest form, this became known as the “labor theory of value,” according to which, a good’s value derives from the number of labor hours it takes to produce. Thus, according to the labor theory of value, diamonds cost more than water because they take so much more labor input to produce than does water.

The theory that labor input determines value has, however, some obvious flaws that soon became apparent. After all, pieces of heavy rock cut into the shape of clouds are quite as hard to produce as diamonds, yet we observe that they have a price of near zero (at least when compared to diamonds) on an open market. But the field would not learn how to resolve the diamond–water paradox for many years. Resolutions to this paradox were provided only in the middle and late nineteenth century during the course of what is now called the Marginalist Revolution.

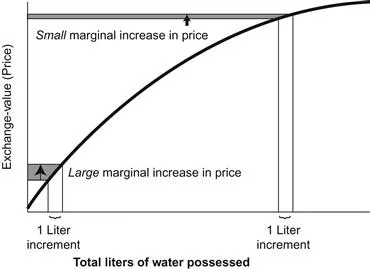

The conceptual break that led to this revolution is simple, yet profound. The key was to realize that the price of water in a particular situation should not to be thought of as reflecting the average value of all water but rather, that it should be thought of in terms of what is known as its marginal value. Here the word marginal refers, in essence, to the first derivative of a function; taking its meaning from the latin word meaning border or edge. To understand the key insight of the marginal revolution, consider a graph of liters-of-water against the total exchange-value of that amount of water, as shown in Figure 1.1. To understand the marginalist approach we want to consider the figure as depicting an empirically observed dataset at the level of a marketplace. It tells us, based on an imaginary empirical dataset of the kind gathered during the marginal revolution, how the price of an additional liter of water depends on how much water the decision maker already possesses. What the marginal revolution focused on was the empirical observation that the second liter of water one comes to possess is observed to command a higher price, per liter, than does the 10,001st liter of water. And this turned out to be a broad empirical regularity: these economists noted the critical fact that the marginal value of a liter of water declined as the total amount of water the decision maker had increased. Thus, since water is plentiful and people already own a large amount of it under most circumstances, the price of an additional liter does not have to be high. Of course this also means that if water were to become scarce, it would be extremely expensive – much more expensive than diamonds.

Figure 1.1 During the Marginal Revolution it was realized that the exchange-value of a single liter of water or a single diamond was influenced both by the intrinsic value of that object and by how many of those objects the decision maker possessed. Here, that relationship is plotted for water. The graph shows the total exchange-value of any given number of liters of water. Note that as the total number of liters of water possessed increases, the value of an additional liter diminishes. Thus if a person possesses no water at all, a single liter is of tremendous value. If a person possesses thousands of liters then the exchange value, to him, of an additional liter would be low.

The next question posed by the early economists of the marginal revolution, however, is the critical one. Given the kinds of empirically observed price curves shown in Figure 1.1 these economists asked: why should it be that a decision maker who already has 10,000 liters of water will only pay a few cents for an additional liter but a decision maker who has only 1 liter of water will pay much more for that same amount of water? What could account for the fact that the same person was willing to pay such a large fraction of his wealth for a single liter of water under so...

Table of contents

- Cover image

- Title page

- Table of Contents

- Copyright

- Preface

- Acknowledgments

- List of Contributors

- Introduction: A Brief History of Neuroeconomics

- Part I: The Fundamental Tools of Neuroeconomics

- Part II: Neural and Psychological Foundations of Economic Preferences

- Part III: Learning and Valuation

- Part IV: The Neural Mechanisms for Choice

- Part V: Brain Circuitry of Social Valuation and Social Choice

- Appendix. Prospect Theory and the Brain

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Neuroeconomics by Paul W. Glimcher,Ernst Fehr in PDF and/or ePUB format, as well as other popular books in Psychology & Cognitive Psychology & Cognition. We have over 1.5 million books available in our catalogue for you to explore.