eBook - ePub

The Independence of Credit Rating Agencies

How Business Models and Regulators Interact

- 200 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Independence of Credit Rating Agencies

How Business Models and Regulators Interact

About this book

The Independence of Credit Rating Agencies focuses on the institutional and regulatory dynamics of these agencies, asking whether their business models give them enough independence to make viable judgments without risking their own profitability.

Few have closely examined the analytical methods of credit rating agencies, even though their decisions can move markets, open or close the doors to capital, and bring down governments. The 2008 financial crisis highlighted their importance and their shortcomings, especially when they misjudged the structured financial products that precipitated the collapse of Bear Stearns and other companies.

This book examines the roles played by rating agencies during the financial crisis, illuminating the differences between U.S. and European rating markets, and also considers subjects such as the history of rating agencies and the roles played by smaller agencies to present a well-rounded portrait.

- Reports on one of the key causes of the 2008 financial crisis: agencies that failed to understand how to analyze financial products

- Describes inherent business model and pricing conflicts that compromise the independence of credit rating agencies

- Reveals how rating agencies large and small, regulatory bodies, and vested interests interact in setting fees and policies

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Chapter one

Rating Agencies and the Rating Service

Rating allows the information asymmetry in the financial and credit markets to be reduced, providing a synthetic judgment of an issue or an issuer that summarizes both the qualitative and quantitative information available.

The quality of the service provided is influenced by the relationship between the rater and the evaluated entity, and normally in the event of solicited rating the information provided is more useful with respect to unsolicited rating.

The service offered by the rater is normally used by both financial investors (individual and institutional) and lenders: In the former the rating is one of the instruments used for selecting the best investment opportunities, while for the latter the rating is used directly in the credit risk evaluation procedure.

Looking at the policies declared by all the main worldwide raters, the chapter discusses the differences in the policies adopted by different raters and evaluates the impact of regulation on the usefulness of the rating service for different types of customers.

Keywords

Issue rating; issuer rating; solicited rating; unsolicited rating; rating users

1.1 Introduction

Financial investors do not have access to the same information set among themselves, and the existence of horizontal asymmetric information (Ramakrishnan and Thakor, 1984) can be a disincentive for capital flows to the financial market and lead to the inefficient allocation of available financial resources (Stiglitz and Weiss, 1981). Information asymmetry increases the impact of a firm’s reputation on the cost and amount of capital that can be raised through the financial market: In this scenario, smaller and younger firms are penalized and may be more financially constrained than bigger players (Diamond, 1989).

To overcome the problem of information asymmetry, firms can hire information providers to obtain an objective evaluation of their business. If the market trusts the evaluators, such firms can reduce the cost of capital or increase capital collected by publishing the judgment obtained due to the expected market reaction to any decrease in information asymmetry (Kerwer, 2002).

Rating agencies provide judgments of an issuer or issue that summarize all available public and reserved information (Cowan, 1991). The main advantage of the rating service is the opportunity to signal to the market the expected impact of reserved information without making it public, due to the confidentiality constraint that characterizes the relationship between the entity evaluated and the agency (Goh and Ederington, 1993).

The rating service is not comparable with the (implicit) judgment of lenders due to the different purposes of the evaluations: In the first case the judgment is only an opinion on an issue or an issuer, whereas the latter case involves direct financial exposure for the lender (Krahnen and Weber, 2001). Moreover, the information given to the market by the rating agencies is more clearly readable for those who are not skilled financial investors.

This chapter analyzes the service offered by rating agencies and presents an updated analysis of the market. Sections 1.2 and 1.3 identify the main characteristics of the service and the users respectively. Section 1.4 presents a detailed outlook of the worldwide market, pointing out the current level of competition and expected trend for the next years. Section 1.5 analyzes the expected characteristics of the service, examining the main requirements established by the supervisory authorities. Finally, Section 1.6 summarizes the chapter and concludes with some policy implications.

1.2 The Rating Service

Rating agencies are information providers that reduce the level of information asymmetry in the market by defining a judgment (the rating) on an issue or an issuer (Ferri and Lacitignola, 2009). A unique definition of the rating service is not available but, on the basis of business declarations given by the rating agencies, some common characteristics can be identified (see Table 1.1).

Table 1.1

Rating Service Definitions

| SCRiesgo | The risk ratings granted by SCRiesgo are the results of an extensive analytical process that includes an exhaustive revision of quantitative and qualitative factors. |

| Demotech Inc. | Our rating process provides an objective baseline for assessing solvency, which in turn provides insight into changes in financial stability. Financial Stability Ratings® are based upon a series of quantitative ratios and quantitative considerations, which together comprise our Financial Stability Analysis Model®. |

| Ecuability S.A. | The credit risk assessment is an opinion based on both qualitative and quantitative data that can be more or less relevant according to the economic environment of each industry or sector. Each type of rating also varies according to the nature of the issue, the issuer, its history, and its corporate culture. |

| MARC | Rating assesses the likelihood of timely repayment of principal and payment of interest over the term to maturity of debts. |

| PACRA | Rating is an interactive process relying primarily on gathering information from the issuer and supplementing it with strategic information obtained from outside independent sources. The entire process is aimed at evaluating (a) financial risk and (b) business risk. Information with regard to (a) is generally provided by the company requesting for rating and, only when necessary, such information is corroborated or complemented by information from other sources. |

| RAM | Rating is an objective and impartial opinion on the ability and willingness of an issuer to make full and timely payments of their financial obligations. It represents a ranking within a consistent framework showing the degree of future default risk of a particular debt, relative to other rated securities in the market. |

| TURK Rating | The rating reflects the company’s current financial strength as well as how the financial position may change in the future. In this respect, extensive research on the outlook of the sector in which the firm operated is also an integral part of the rating methodology. |

Source: Rating agency websites (accessed 03.01.2013).

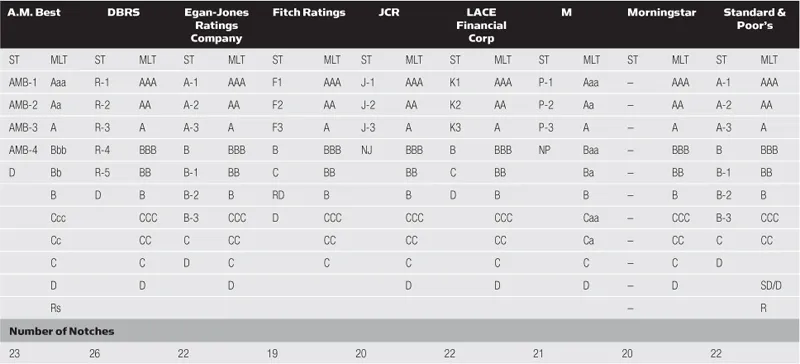

A rating is a synthetic judgment that summarizes, using an alphanumeric scale, the main qualitative and quantitative characteristics of an issue or issuer (Nickell, Perraudin, and Varotto, 2000). The agency does not assume any responsibility for inaccuracy in the rating because they explicitly declare that it represents only an opinion (Bussani, 2010). The judgment is stated using the rating classes (i.e. AAA, BB, A1, etc.) as main segmentation criteria and, when necessary, the agency may offer a more detailed classification using secondary segmentation criteria, defined as notches (i.e.+,−,+/−, etc.). Each agency can define different levels of detail for their rankings, and frequently defines different rating scales for different types of issuers and issues and/or different time horizons (see Table 1.2).

Table 1.2

Rating Scales for Bond Issues in the Short and Medium to Long Term

Notes: –=Information not available

Source: SEC (2012), Report to Congress Credit Rating Standardization Study, available at<www.sec.gov>(accessed 03.01.2013).

The information given to the market may be supplied by further information about the perspectives of the issue or the issuer that are summarized in the outlook or credit watch. The purpose of these two instruments is the same, but while the first is normally us...

Table of contents

- Cover image

- Title page

- Table of Contents

- Copyright

- Dedication

- Foreword

- Acknowledgements

- List of Tables

- List of Figures

- Introduction

- Chapter one. Rating Agencies and the Rating Service

- Chapter two. Rating and Financial Markets

- Chapter three. The Rating Market

- Chapter four. Economic and Financial Equilibrium of Rating Agencies

- Chapter five. Rating Agencies’ Pricing Policies

- Chapter six. Organizational Structure and Rating Agency Independence

- Chapter seven. The Economic Independence of Rating Agencies

- Conclusions

- Appendix

- References

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Independence of Credit Rating Agencies by Gianluca Mattarocci in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.