eBook - ePub

Venture Capital and Private Equity Contracting

An International Perspective

- 780 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Venture Capital and Private Equity Contracting

An International Perspective

About this book

Other books present corporate finance approaches to the venture capital and private equity industry, but many key decisions require an understanding of the ways that law and economics work together. This revised and updated 2e offers broad perspectives and principles not found in other course books, enabling readers to deduce the economic implications of specific contract terms. This approach avoids the common pitfalls of implying that contractual terms apply equally to firms in any industry anywhere in the world.

In the 2e, datasets from over 40 countries are used to analyze and consider limited partnership contracts, compensation agreements, and differences in the structure of limited partnership venture capital funds, corporate venture capital funds, and government venture capital funds. There is also an in-depth study of contracts between different types of venture capital funds and entrepreneurial firms, including security design, and detailed cash flow, control and veto rights. The implications of such contracts for value-added effort and for performance are examined with reference to data from an international perspective. With seven new or completely revised chapters covering a range of topics from Fund Size and Diseconomies of Scale to Fundraising and Regulation, this new edition will be essential for financial and legal students and researchers considering international venture capital and private equity.

- An analysis of the structure and governance features of venture capital contracts

- In-depth study of contracts between different types of venture capital funds and entrepreneurial firms

- Presents international datasets from over 40 countries around the world

- Additional references on a companion website

- Contains sample contracts, including limited partnership agreements, term sheets, shareholder agreements, and subscription agreements

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Topic

CommerceSubtopic

Finances d'entreprisePart One

Introduction

Outline

1 Introduction and Overview

2 Overview of Agency Theory, Empirical Methods, and Institutional Contexts

3 Overview of Institutional Contexts and Empirical Methods

1

Introduction and Overview

This chapter provides an overview of the topics covered in the book entitled “Venture Capital and Private Equity Contracting: An International Perspective”. Broadly framed questions addressed in this book include, but are not limited to, the following: What covenants and compensation terms are used in limited partnership contracts? In what ways are limited partnership contracts related to market conditions and fund manager characteristics, and how do these contracts differ across countries? What are the cash flow and control rights that are typically assigned in venture capital and private equity contracts with investee firms, and when do fund managers demand more contractual rights? Do different contractual rights assigned to different parties influence the effort provided by the investor(s)? In what ways are different financial contracts related to the success of venture capital and private equity investments? By considering venture capital and private equity contracting in an international setting, this book offers an understanding of why venture capital and private equity markets differ with respect to fund governance, investee firm governance, and investee firm performance.

Keywords

Venture capital; private equity; financial contracting

These days it is difficult to not have heard of the terms “venture capital” and “private equity”. The venture capital and private equity markets are frequently discussed in popular media and typically referred to as “scorching” in the popular press, at least in boom times. The market has direct relevance for entrepreneurs who want to raise money, investors who want to make money from financing entrepreneurs, and individuals who want to work for a fund or set up their own fund. Also, venture capital and private equity is of significant interest to the public sector, as government bodies around the world strive to find ways to promote entrepreneurship and entrepreneurial finance. It is widely believed that venture capital and private equity funds facilitate more innovative activities and thereby improve the well being of nations. It is thought of as a critical aspect of national growth in the twenty-first century.

In the next 23 chapters, which are divided into 4 parts, we will provide an analysis of the issues that venture capital and private equity market participants face during the fund-raising process (Part II), investment process (Part III), and divestment process (Part IV). A common theme across all issues involves agency costs, and hence agency theory is reviewed after this introductory chapter in Chapter 2 (Part I). All the issues addressed in this book are analyzed from an empirical law and finance perspective, with a focus on financial contracting. Financial contracts are central to the establishment of the relationship between venture capital and private equity funds and their investors. Financial contracts also govern the relationship between venture capital and private equity funds and their investee entrepreneurial firms, as well as determine the efficacy of the divestment process. In most chapters we refer to datasets to grasp the real-world aspects of the venture capital and private equity process. Further, it is important to consider international evidence to grasp the impact of laws and institutions on the respective venture capital and private equity markets. The empirical methods and legal and institutional settings in this book are overviewed in Chapter 3.

1.1 What is Venture Capital and Private Equity?

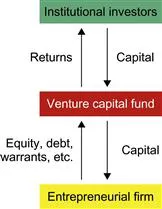

At the outset, it is important to discuss what is meant by the terms venture capital and private equity. Venture capital and private equity funds are financial intermediaries between sources of funds (typically institutional investors) and high-growth and high-tech entrepreneurial firms. Funds are typically established as limited partnerships, but as discussed herein, there are other types of funds. A limited partnership is in essence a contract between institutional investors who become limited partners (pension funds, banks, life insurance companies, and endowments who have rights as partners but trade “management” rights over the fund for limited liability) and the fund manager who is designated the general partner (the partner that takes on the responsibility of the day-to-day operations and management of the fund and assumes total liability in return for negligible buyin). Chapter 5 examines in detail the structure of limited partnerships and limited partnership contracts. The basic intermediation structure of venture capital and private equity funds is graphically summarized in Figure 1.1.

Figure 1.1 Venture capital financial intermediation.

Venture capital funds are typically set up with at least US$50 million in capital committed from institutional investors and often exceed US$100 million. Some of the larger private equity funds raised more than US$10 billion in 2006.1 Fund managers typically receive compensation in the form of a management fee (often 1–2% of committed capital, depending on the fund size) and a performance fee or carried interest (20% of capital gains). Chapter 6 discusses factors related to fund manager compensation. Venture capital funds invest in start-up entrepreneurial firms that typically require at least US$1 million and up to US$20 million in capital. Private equity funds invest in more established firms, as discussed further below.

Venture capital is often referred to as the “money of invention” (see, e.g., Black and Gilson, 1998; Gompers and Lerner, 1999, 2001; Kortum and Lerner, 2000) and venture capital fund managers as those that provide value-added resources to entrepreneurial firms. Venture capital fund managers play a significant role in enhancing the value of their entrepreneurial investments as they provide financial, administrative, marketing, and strategic advice to entrepreneurial firms, as well as facilitate a network of support for an entrepreneurial firm with access to accountants, lawyers, investment bankers, and organizations specific to the industry in which the entrepreneurial firm operates (Gompers and Lerner, 1999; Leleux and Surlemount, 2003; Manigart et al., 2002a, b; Sahlman, 1990; Sapienza et al., 1996; Wright and Lockett, 2003). Academic studies have shown us that venture capital-backed entrepreneurial firms are on average significantly more successful than nonventure capital-backed entrepreneurial firms in terms of innovativeness (Kortum and Lerner, 2000), profitability, and share price performance upon going public (Gompers and Lerner, 1999, 2001).

Venture capital and private equity investments carried out by a fund typically last over a period of 2–7 years. A venture capital limited partnership envisages this extended investment horizon and hence is structured over a 10-year horizon (with an option to continue for an additional 3 years) so that the fund manager can select investments over the first few years and then bring those investments to fruition over the remaining life of the fund. Investments are made with a view toward capital gains upon an exit event (a sale transaction), as entrepreneurial firms typically are not able to pay interest on debt or dividends on equity. The terms of the investment often give the venture capital fund significant cash flow rights in the form of equity and priority in the event of liquidation. As well, the venture capital fund typically receives significant veto and control rights over decisions made by the management of the entrepreneurial firm.

The terms venture capital and private equity differ primarily with respect to the stage of development of the entrepreneurial firm in which they invest. Venture capital refers to investments in earlier-stage firms (seed or start-up firms), whereas private equity is a broader term that also encompasses later-stage investments as well as buyouts and turnaround investments. In this book, unless explicitly stated otherwise, for ease of exposition we use the term “private equity” to encompass all private investment stages including venture capital. The various financing stages are defined as follows.

• Seed

− Financing provided to entrepreneurs to research, assess, and develop an initial concept before a business has reached the start-up phase.

• Start-up

− Financing provided to firms for product development and initial marketing. Firms may be in the process of being set up or may have been in business for a short time but have not sold their product commercially.

• Other early stage

− Financing to firms that have completed the product development stage and require further funds to initiate commercial manufacturing and sales. They will not yet be generating a profit.

• Expansion

− Financing provided for the growth and expansion of a firm which is breaking even or trading profitably. Capital may be used to finance increased production capacity, market or product development, and/or to provide additional working capital.

• Bridge financing

− Financing made available to a firm in the period of transition from being privately owned to being publicly quoted.

• Secondary purchase/replacement capital

− Purchase of existing shares in a firm from another private equity investment organization or from another shareholder or shareholders.

• Rescue/turnaround

− Financing made available to an existing firm which has experienced trading difficulties (firm is not earning its cost of capital (WACC)), with a view to reestablishing prosperity.

• Refinancing bank debt

− To reduce a firm’s level of gearing.

• Management buyout

− Financing provided to enable current operating management and investors to acquire an existing product line or business.

• Management buyin

− Financing provided to enable a manager or group of managers from outside the firm to buyin to the firm with the support of private equity investors.

• Venture purchase of quoted shares

− Purchase o...

Table of contents

- Cover image

- Title page

- Table of Contents

- Copyright

- Dedication

- Preface

- Part One: Introduction

- Part Two: Fund Structure and Governance

- Part Three: Financial Contracting between Funds and Entrepreneurs

- Part Four: Investor Effort

- Part Five: Divestment

- Part Six: Conclusion and Appendices

- Bibliography

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Venture Capital and Private Equity Contracting by Douglas J. Cumming,Sofia A. Johan in PDF and/or ePUB format, as well as other popular books in Commerce & Finances d'entreprise. We have over 1.5 million books available in our catalogue for you to explore.