eBook - ePub

Rethinking Valuation and Pricing Models

Lessons Learned from the Crisis and Future Challenges

- 652 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Rethinking Valuation and Pricing Models

Lessons Learned from the Crisis and Future Challenges

About this book

It is widely acknowledged that many financial modelling techniques failed during the financial crisis, and in our post-crisis environment many techniques are being reconsidered. This single volume provides a guide to lessons learned for practitioners and a reference for academics. Including reviews of traditional approaches, real examples, and case studies, contributors consider portfolio theory; methods for valuing equities and equity derivatives, interest rate derivatives, and hybrid products; and techniques for calculating risks and implementing investment strategies. Describing new approaches without losing sight of their classical antecedents, this collection of original articles presents a timely perspective on our post-crisis paradigm.

- Highlights pre-crisis best classical practices, identifies post-crisis key issues, and examines emerging approaches to solving those issues

- Singles out key factors one must consider when valuing or calculating risks in the post-crisis environment

- Presents material in a homogenous, practical, clear, and not overly technical manner

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

1

The Effectiveness of Option Pricing Models During Financial Crises

Chapter Outline

1.1 Introduction

1.2 Methodology

1.3 Data

1.4 Results

1.5 Concluding Remarks

References

1.1 Introduction

Options can play an important role in an investment strategy. For example, options can be used to limit an investor’s downside risk or be employed as part of a hedging strategy. Accordingly, the pricing of options is important for the overall efficiency of capital markets.1 The purpose of this chapter is to explore the effectiveness of the original Black and Scholes (1973) option pricing model (BS model) against a more complicated non-parametric neural network option pricing model with a hint (NN model). Specifically, this chapter compares the effectiveness of the BS model versus the NN model during periods of stable economic conditions and economic crisis conditions.

Past literature suggests that the standard assumptions of the BS model are rarely satisfied. For instance, the well-documented “volatility smile” and “volatility smirk” (Bakshi et al., 1997) pricing biases violate the BS model assumption of constant volatility. Additionally, stock returns have been shown to exhibit non-normality and jumps. Finally, biases also occur across option maturities, as options with less than three months to expiration tend to be overpriced by the Black–Scholes formula (Black, 1975).

In order to address the biases of the BS model, research efforts have focused on developing parametric and non-parametric models. With regard to parametric models, the research has mainly focused on three models: The stochastic volatility (SV), stochastic volatility random jump (SVJ) and stochastic interest rate (SI) parametric models. All three models have been shown to be superior to the BS model in out-of-sample pricing and hedging exercises (Bakshi et al., 1997). Specifically, the SV model has been shown to have first-order importance over the BS model (Gencay and Gibson, 2009). The SVJ model further enhances the SV model for pricing short-term options, while the SI model extends the SVJ model in regards to the pricing of long-term options (Gencay and Gibson, 2009).

Although parametric models appear to be a panacea with regard to relaxing the assumptions that underlie the BS model, while simultaneously improving pricing accuracy, these models exhibit some moneyness-related biases for short-term options. In addition, the pricing improvements produced by these parametric models are generally not robust (Gencay and Gibson, 2009; Gradojevic et al., 2009). Accordingly, research also explores non-parametric models as an alternative, (Wu, 2005). The non-parametric approaches to option pricing have been used by Hutchinson et al. (1994), Garcia and Gencay (2000), Gencay and Altay-Salih (2003), Gencay and Gibson (2009), and Gradojevic et al. (2009).

Non-parametric models, which lack the theoretical appeal of parametric models, are also known as data-driven approaches because they do not constrain the distribution of the underlying returns (Gradojevic et al., 2011). Non-parametric models are superior to parametric models at dealing with jumps, non-stationarity and negative skewness because they rely upon flexible function forms and adaptive learning capabilities (Agliardi and Agliardi, 2009; Yoshida, 2003). Generally, non-parametric models are based on a difficult tradeoff between rightness of fit and smoothness, which is controlled by the choice of parameters in the estimation procedure. This tradeoff may result in a lack of stability, impeding the out-of-sample performance of the model. Regardless, non-parametric models have been shown to be more effective than parametric models at relaxing BS model assumptions (Gencay and Gibson, 2009; Gradojevic and Kukolj, 2011; Gradojevic et al., 2009). Accordingly, the BS model is compared against a non-parametric option pricing model in this chapter.

Given its currency, little research has been conducted on the effectiveness of option pricing during the 2008 financial crisis. However, the 1987 stock market crash has proved to be fertile grounds for research with regard to option pricing during periods of financial distress. For example, Bates (1991, 2000) identified an option pricing anomaly just prior to the October 1987 crash. Specifically, out-of-the-money American put options on S&P 500 Index futures were unusually expensive relative to out-of-the-money calls. In a similar line of research, Gencay and Gradojevic (2010) used the skewness premium of European options to develop a framework to identify aggregate market fears to predict the 1987 market crash.

This chapter expands the option pricing literature by comparing the accuracy of the BS model against NN models during the normal, pre-crisis economic conditions of 1987 and 2008 (the first quarter of each respective year) against the crisis conditions of 1987 and 2008 (the fourth quarter of each respective year). Therefore, this work also provides new and novel insights into the accuracy of option pricing models during the recent 2008 credit crisis.

The results suggest that the more complicated NN models are more accurate during stable markets than the BS model. This result is consistent with the past literature that suggest non-parametric models are superior to the BS model (e.g. Gencay and Gibson, 2009; Gradojevic et al., 2009). However, the results during the periods of high volatility are counterintuitive as they suggest that the simpler BS model is superior to the NN model. These results suggest that a regime switch from stable economic conditions to periods of excessively volatile conditions impedes the estimation and the pricing ability of non-parametric models. In addition to the regime shift explanation, considerations should be given to the fact that the BS model is a pre-specified non-linearity and its structure (shape) does not depend on the estimation dataset. This lack of flexibility and adaptability appears to be beneficial when pricing options in crisis periods. It conclusion, it appears as if the learning ability and flexibility of non-parametric models largely contributes to their poor performance relative to parametric models when markets are highly volatile and experience a regime shift.

The results make a contribution that is relevant to academic and practitioners alike. With the recent financial crisis of 2007–2009 creating pitfalls for various asset valuation models, this chapter provides practical advice to investors and traders with regard to the most effective model for option pricing during times of economic turbulence. In addition, the results make a contribution to the theoretical literature that investigates the BS model versus its parametric and non-parametric counterparts by suggesting that the efficacy of the option pricing model depends on the economic conditions.

The remainder of this chapter is organized as follows: Section 1.2 outlines the methodology, Section 1.3 discusses the data, Section 1.4 presents the results and Section 1.5 provides concluding remarks.

1.2 Methodology

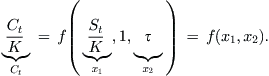

The option pricing formula is defined as in Hutchinson et al. (1994) and Garcia and Gençay (2000):

where Ct is the call option price, St is the price of the underlying asset, K is the strike price and τ is the time to maturity (number of days). Assuming the homogeneity of degree one of the pricing function ϕ with respect to St and K, one can write the option pricing function as follows:

We extend the model in Equation (1.2) with two additional inputs—the implied volatility and the risk-free interest rate:

We estimate Equation (1.3) non-parametrically using a feedforward NN model with the “hint” fr...

Table of contents

- Cover image

- Title page

- Table of Contents

- Editor’s Disclaimers

- Copyright

- Foreword

- Editors

- Contributors

- 1. The Effectiveness of Option Pricing Models During Financial Crises

- 2. Taking Collateral into Account

- 3. Scenario Analysis in Charge of Model Selection

- 4. An “Economical” Pricing Model for Hybrid Products

- 5. Credit Valuation Adjustments– Mathematical Foundations, Practical Implementation and Wrong Way Risks

- 6. Counterparty Credit Risk and Credit Valuation Adjustments (CVAs) for Interest Rate Derivatives–Current Challenges for CVA Desks

- 7. Designing a Counterparty Risk Management Infrastructure for Derivatives

- 8. A Jump–Diffusion Nominal Short Rate Model

- 9. The Widening of the Basis: New Market Formulas for Swaps, Caps and Swaptions

- 10. The Financial Crisis and the Credit Derivatives Pricing Models

- 11. Industry Valuation-Driven Earnings Management

- 12. Valuation of Young Growth Firms and Firms in Emerging Economies

- 13. Towards a Replicating Market Model for the US Oil and Gas Sector

- 14. Measuring Systemic Risk from Country Fundamentals: A Data Mining Approach

- 15. Computing Reliable Default Probabilities in Turbulent Times

- 16. Discount Rates, Default Risk and Asset Pricing in a Regime Change Model

- 17. A Review of Market Risk Measures and Computation Techniques

- 18. High-Frequency Performance of Value at Risk and Expected Shortfall: Evidence from ISE30 Index Futures

- 19. A Copula Approach to Dependence Structure in Petroleum Markets

- 20. Mistakes in the Market Approach to Correlation: A Lesson For Future Stress-Testing

- 21. On Correlations between a Contract and Portfolio and Internal Capital Alliocation

- 22. A Maximum Entropy Approach to the Measurement of Event Risk

- 23. Quantifying the Unquantifiable: Risks Not in Value at Risk

- 24. Active Portfolio Construction When Risk and Alpha Factors are Misaligned

- 25. Market Volatility, Optimal Portfolios and Naive Asset Allocations

- 26. Hedging Strategies with Variable Purchase Options

- 27. Asset Selection Using a Factor Model and Data Envelopment Analysis– A Quantile Regression Approach

- 28. Tail Risk Reduction Strategies

- 29. Identification and Valuation Implications of Financial Market Spirals

- 30. A Rating-Based Approach to Pricing Sovereign Credit Risk

- 31. Optimal Portfolio Choice, Derivatives and Event Risk

- 32. Valuation and Pricing Concepts in Accounting and Banking Regulation

- 33. Regulation, Regulatory Uncertainty and the Stock Market: The Case of Short Sale Bans

- 34. Quantitative Easing, Financial Risk and Portfolio Diversification

- 35. Revisiting Interest Rate Pricing Models from an Indian Perspective: Lessons and Challenges

- 36. Investment Opportunities in Australia’s Healthcare Stock Markets After the Recent Global Financial Crisis

- 37. Predicting ASX Health Care Stock Index Movements After the Recent Financial Crisis Using Patterned Neural Networks

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Rethinking Valuation and Pricing Models by Carsten Wehn,Christian Hoppe,Greg N. Gregoriou in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.