This book examines four aspects of Malaysian consumers' financial vulnerabilities. First, it discusses the issue of over-indebtedness due to excessive reliance on consumer financing. Second, the book investigates why Malaysians are ill-prepared for their golden years in terms of retirement planning and savings. Third, it delves into the problem of financial fraud victimisation among Malaysian consumers. Fourth, the book analyses the reasons why Malaysians are underinsured despite the distinct benefits of life insurance.

Drawing on secondary data from government agencies such as Bank Negara Malaysia, Employees' Provident Fund, Royal Malaysian Police and the Department of Statistics Malaysia, each chapter presents statistical trends reflecting the four financial vulnerabilities. In-depth analyses of the literature reveal three broad psychological domains (cognition, motivation, and disposition) and specific psychological factors (e.g. over-confidence, self-control, social norms, and financial literacy) that significantly influence consumers' financial decisions. The four financial vulnerabilities investigated in this book directly address the strategic outcomes of the Malaysian National Strategy for Financial Literacy 2019–2023 (MNSFL), a five-year plan to elevate the financial literacy of Malaysians. Finally, the book presents strategic recommendations that are believed to be useful guidelines for relevant policymakers to promote positive financial behaviours and rational attitudes among consumers.

It will be a useful resource for policymakers and researchers interested in economic psychology and behavioural finance.

Personal finance is an issue that is relevant to all individuals. It is about the behaviour and practices of money management and encompasses a spectrum of financial aspects such as spending, saving, investing, borrowing, and protection. Financial management skills are normally gained from past experiences and sources such as books, magazines, the Internet, newspapers, social media, and advice from friends and family. In addition, people sometimes follow their emotions and gut feelings in their money-related decisions. Due to the limitations in financial knowledge and skills, not everyone succeeds in managing their finances and are at times, vulnerable to financial shocks and uncertainties that may occur over their lifetime.

In traditional economic theories, people are assumed to be rational. These theories hypothesise that individuals base their decisions in a perfect world with complete information and would always seek to maximise utility and wealth. However, the reality is that humans are imperfect beings living in an imperfect world. In this line of reasoning, proponents of new behavioural economic theory argue that the field of economics and finance cannot be separated from the discipline of human behaviour, cognition, and psychology. Analysing individuals as true homo sapiens rather than “homo economicus” beings should therefore provide a more accurate picture of individuals’ financial behaviour. Scholars from the behavioural finance paradigm suggest that individuals who make decisions based on emotions and instincts are prone to behavioural biases, hence leading them into making “sub-optimal” financial decisions. The irrationalities related to the behaviour and choices that people make, thus, explain why the outcomes achieved may sometimes be unexpected and undesirable in the pursuit of financial goals.

Recognising that behaviour and emotions are central in people’s decision-making, this book focuses on exploring the common financial vulnerabilities that consumers face over their life cycle, and the behavioural and psychological causes of these vulnerabilities will be analysed. There are four financial aspects that will be covered in this book, namely over-indebtedness, retirement savings inadequacy, financial fraud victimisation, and underinsurance. While debt may be considered inevitable, especially in the early part of the life cycle, over-indebtedness could be a major problem and could possibly lead to delinquency and bankruptcy if left uncontrolled. Such financial problems may also lead to other psychological and social problems such as deteriorated physical health, stress, depression, and strained relationships.

Retirement savings inadequacy is another issue that has been long discussed and debated by policymakers across the globe. Countries that are experiencing population ageing, such as Malaysia, will have an increasing portion of elderly population in the future, hence, ensuring that they have sufficient retirement savings is eminent. Despite mandatory contribution plans enacted, retirees’ savings usually fall significantly below the adequate level to be able to sustain pre-retirement lifestyles.

The third aspect discussed in this book relates to financial fraud victimisation. Numerous incidents of victimisation cases have been reported to authorities over the past several years, and many cash-rich individuals have lost big sums of their hard-earned money to the scrupulous hands of fraudsters. Thus, understanding the cause of this consumer financial vulnerability is vital in implementing effective control measures.

The last issue to be examined in this book relates to underinsurance among Malaysian consumers. Despite numerous consumer education and awareness campaigns, it remains perplexing as to why many Malaysians do not have any form of insurance and Shariah-compliant insurance (takaful) protection. Are Malaysians overconfident about their earning abilities? Do they lack the self-control when it comes to taking on debts and preparing for the future? Are they naïve in their investment decisions, or are they too trusting? Are they innocently ignorant or are they simply greedy? These are questions that the book tends to explore, with a focus on the Malaysian scenario.

This book aims to achieve four objectives. The first objective is to examine the current state and trends of various consumer financial vulnerabilities in Malaysia, namely, (i) over-indebtedness, (ii) retirement savings inadequacy, (iii) fraudulent financial and investment victimisation, and (iii) lack of protection using insurance and takaful products. Each of these vulnerabilities will be examined and discussed in four (4) separate chapters, namely, Chapters 2 to 5, respectively. The second objective is to explore the causes of consumer financial vulnerabilities from the perspective of behavioural theories and empirical evidence. The third objective is to discuss the various policies that have already been implemented to influence consumer financial behaviour in Malaysia. Lastly, the fourth objective is to propose additional strategies to policymakers on ways to nudge consumers in the right way in regards to their finances.

1.1 Background of Malaysia

1.1.1 Economic status

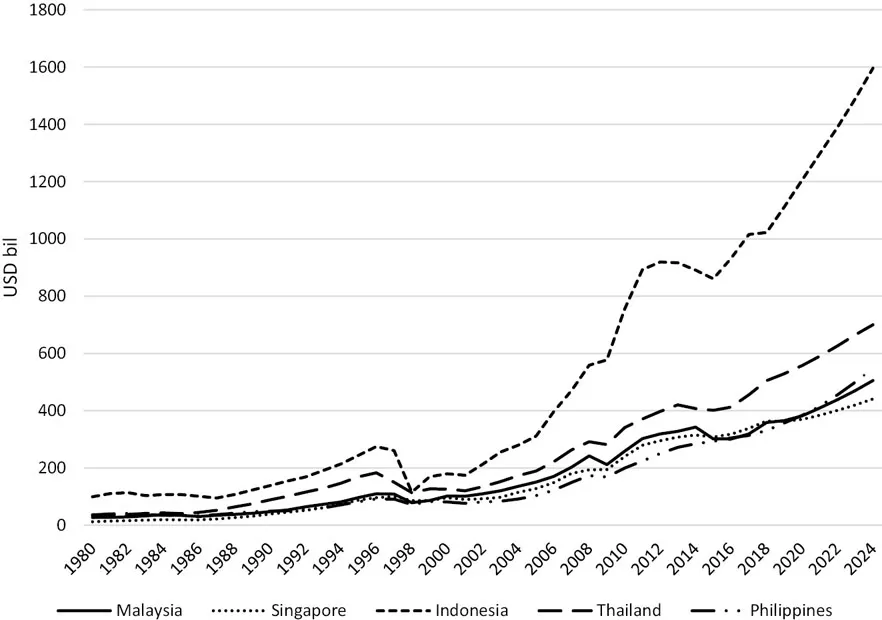

Malaysia is an emerging economy, located in the heart of Southeast Asia, and aspires towards becoming a high-income nation. According to the Global Competitiveness Report 2018, out of 140 economies, Malaysia ranks 25th globally in terms of national competitiveness and productivity (World Economic Forum, 2018). Among the ten Association of Southeast Asian Nations (ASEAN) countries, Malaysia ranks fourth in terms of gross domestic product (GDP) size, after Indonesia, Thailand, and Philippines (International Monetary Fund, 2019). As at 2020, the Malaysian GDP at current prices is estimated to be USD381.52 billion. Figure 1.1 shows the trend of GDP (current prices) of the top five ASEAN economies.

Figure 1.1GDP of the top five ASEAN economies (in billions of USD).

Source: International Monetary Fund (2019).

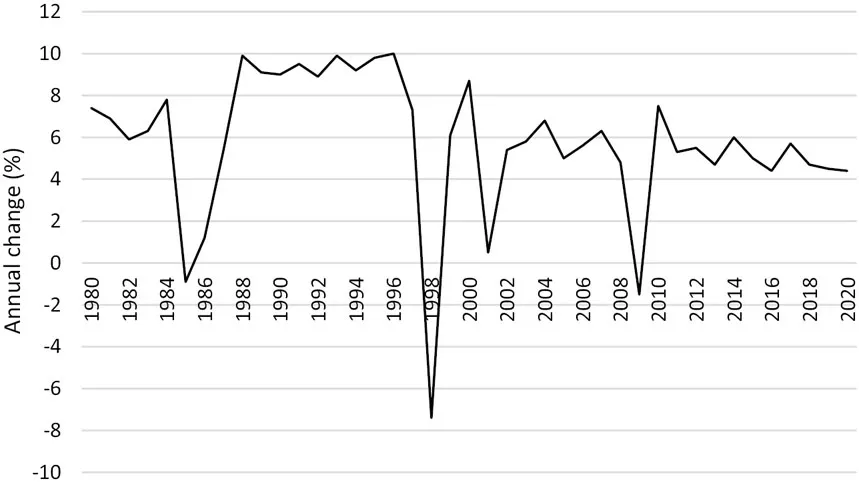

Meanwhile, Figure 1.2 shows the annual percentage change of real GDP in Malaysia from 1980 to 2020. There are notable downward shocks noted in this illustration, particularly in years 1985, 1998, and 2009. These shocks are due to the financial crises, namely the 1985 commodity shock triggered by the high-interest rate regime in the United States (the Volker shock), the 1998 Asian financial crisis triggered by the floating of the Thai baht, and the 2008 global financial crisis caused by the subprime mortgage crisis in the United States. As can be seen from the graph, these crises had obvious effects on Malaysia’s economic growth. The Malaysian GDP growth rate averages at 5.25% annually from 2010 to 2020.

Figure 1.2Malaysia’s real GDP growth (annual percentage change).

Source: International Monetary Fund (2019).

1.1.2 Population

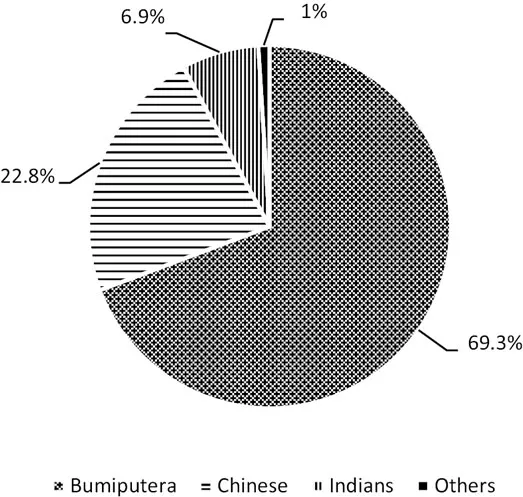

Malaysia’s population as of 2019 is estimated to be 32.6 million of which 29.4 million (90.2%) are Malaysian citizens, while the remaining 3.2 million (9.8%) are non-citizens. The country is a multi-ethnic nation with four main ethnic groups – Bumiputeras, Chinese, Indians, and others. The Bumiputera group holds the largest majority of citizens (69.3%), followed by the Chinese (22.8%), Indians (6.9%), and others (1.0%) (Department of Statistics Malaysia, 2019). Figure 1.3 illustrates the composition of ethnic groups in Malaysia as of 2019.

Figure 1.3Population composition of Malaysian citizens according to ethnicity in 2019...

Table of contents

Cover

Half Title

Series Information

Title Page

Copyright Page

Table of Contents

List of Figures

List of Tables

Preface

Acknowledgements

1 Overview: Consumer financial vulnerabilities in Malaysia

2 Consumer debt: Friend or foe?: Exploring its causes and consequences

3 Will Malaysians retire in contentment or misery?: Financial behaviour issues approaching old age

4 Falling prey to financial fraud: Investigating the causes of victimisation

5 The paradox of life insurance protection: Why are consumers underinsured?

6 Summary and strategic recommendations

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Consumer Financial Vulnerabilities in Malaysia by Nurul Shahnaz Ahmad Mahdzan,Mohd Edil Abd Sukor,Izlin Ismail,Mahfuzur Rahman in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.