Corporate governance and corporate reporting are closely linked to each other, and their respective evolutionary patterns are mutually influencing. Along with the recent expansion of company disclosure, a growing attention is being paid to corporate governance determinants and mechanisms underpinning the decision to voluntarily adopt non-financial disclosure formats, such as integrated reporting.

At institutional level, several national corporate governance codes have been changed towards the recognition and inclusion of this innovative, non-financial language. In academic research, the influence of corporate governance variables vis-à-vis the choice to embrace such reporting practices has been subject to a long scrutiny. However, only a little inquiry has so far analysed the influence of corporate governance factors on integrated reporting adoption, quality, and credibility.

Accordingly, the aim of the book is to investigate if, and to what extent, corporate board composition and characteristics can affect, at the same time, the decision to voluntarily adopt integrated reporting by companies as well as their financial performance. The study carries out an empirical analysis of the professional features of board members at the time of their decision to implement integrated reporting as a new form of company accountability. The work provides innovative insights into the articulated relationships between the quantitative and qualitative composition of corporate boards and the latter's choice to uptake this advanced form of reporting to represent the wider value creation processes of their organisations.

The company is an artificial person which has no heart, mind or soul of its own.

Directors, once appointed, become the heart, mind and soul of the company.

The sense of the book

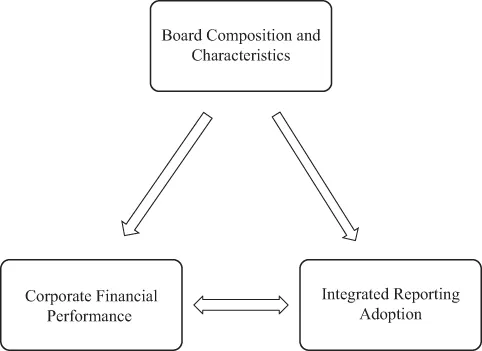

The aim of this book is to investigate if and to what extent corporate board composition and characteristics can affect, at the same time, the decision to voluntarily adopt integrated reporting by companies as well as their financial performance. These relationships are examined at the time of adoption and with reference to organisations located in countries other than South Africa, where this accountability tool is mandatory for listed companies.

Drawing on this analysis, the study intends to provide innovative insights into the articulated relationship between the quantitative and qualitative composition of corporate boards on the one side, and firm financial performance and the board’s choice to uptake this advanced form of reporting on the other one.

Furthermore, the book also explores the association between the financial performance of the company and the decision of implementing integrated reporting. Some studies have in fact found the choice of integrated reporting as being guided by an “impression management” approach, i.e. as a means through which managers can favourably influence investors and stakeholders. Figure 1.1 summarises the linkages that will be explored in this study.

Figure 1.1 The linkages investigated in the book.

In this respect, this research can be located into the broader stream of academic and professional literature investigating the complex nexus of relationships between corporate governance determinants, mechanisms, and consequences (De Villiers and Dimes, 2020), and, more specifically, it is sympathetic with the studies that have advanced that the human side of corporate governance and its linkage to value creation should be better understood (Huse, 2007).

In general terms, it can be said that corporate governance and corporate reporting are closely linked to each other, and their respective evolutionary paths appear to have been mutually influencing (Fiori and Tiscini, 2005; Kolk, 2008; Kolk and Pinkse, 2010; Chan et al., 2014).

From a theoretical viewpoint, since the emergence within companies of the separation between ownership and control (Berle and Means, 1932), conducive later to the Agency theory (Jensen and Meckling, 1976) and the doctrine of shareholder primacy and value (Rappaport, 1986), corporate governance has been mainly conceived as a way to guarantee investor protection. This view echoes the Milton Friedman’s well-known philosophy on the basis of which the only social responsibility of corporations is to increase their profits for shareholders (Friedman, 1970).

In this respect, Shleifer and Vishny (1997, p. 737) state that “corporate governance deals with the ways in which suppliers of finance to corporations assure themselves of getting a return on their investment”, while La Porta et al. (2000, p. 4) refer to corporate governance as a “set of mechanisms through which outside investors protect themselves against expropriation by the insiders”, where ‘the insiders’ are embodied by managers and controlling shareholders. Hence, it can be maintained that Agency theory calls for a more significant proportion of outside and independent directors in the board, in that they can align more easily shareholder and manager interests, thus more effectively exerting the perceived board’s primary function of ‘control’. Interestingly enough, this modern view contrasts with the traditional vision going back to the 1930s, according to which the role of executives was instead to “instill the sense of moral purpose in company’s employees” (Barnard, 1938, p. 89).

Only recently the various general calls for broadening the governance scope towards a more profound consideration of interests and needs of different categories of interests (Stakeholder theory) have started being heard (Freeman and Reed, 1983; Luoma and Goodstein, 1999). This approach has been essentially articulated in terms of corporate governance and board’s behaviour through the Stewardship theory and the Resource-Dependence theory.

According to the Stewardship theory, managers are not only to be conceived as those to be controlled because they assume a self-interested and ‘opportunistic behaviour’. They can have a ‘good steward behaviour’ (Donaldson and Davis, 1991, as they are moved by incentives that are not (only) of financial nature related to both their own satisfaction (i.e. recognition, personal achievement) and the organisational one (i.e. good performance or company success). It follows that the board’s primary function is still that of control, but the latter is fundamentally shifted to managers, who thus become an integral component of the company’s governing body. In other words, Stewardship theory favourably views the presence of insiders in the boardroom as, having a profound knowledge of the organisation, they can maximise shareholders’ profit as well as outsiders’ interests.

In addition to Agency and Stewardship conceptual approaches, Resource-Dependence theory has also been put forward to study corporate governance (Pfeffer and Salancik, 1978). The central focus of this theory expands beyond the needs and interests of providers of financial capital to consider the overall external environment in which the company operates. In particular, organisations aim to exert control on the surrounding context to assimilate the set of resources they need to survive. Accordingly, the function of the board of directors is not only that of acting as a monitoring body but also that of providing resources to the organisation through its external networks (Hillman and Dalziel, 2003).

On a broader perspective, there seems to be a wide consensus that over the years corporate governance and, consequently, board roles and functions have become more complex and difficult regarding not only the protection of the rights and interests of shareholders and investors, but more generally the response to the expectations of stakeholders, communities, and networks rotating around companies and their operations, and the information thereon (Huse and Rindova, 2001; Ayuso et al., 2014). This evolution has translated into various attempts to integrate the above delineated different theoretical views (Donaldson and Davis, 1991; Muth and Donaldson, 1998; Kiel and Nicholson, 2003; Nicholson and Kiel, 2007). In this respect, it might be interesting to consider whether also the relationship between board composition and its features, company financial performance, and integrated reporting can be better understood in light of a more unitary conceptual approach drawing on all of these diverse theories.

In parallel with the evolution of the roles of corporate governance, in the last 20 years corporate disclosure also has been relentless expanding its boundaries towards the enclosure of a more comprehensive set of information well beyond that required by financial reporting (Lev and Zarowin, 1999). At first, there has been the publication of information on the environmental and social impacts of organisational activities and then, more generally, on corporate value creation processes, also encompassing intangibles. This expansion process in company disclosure has been supported not only by a new political and societal climate and a relatively more open reporting attitude of companies, but also by innovative research findings, according to which disclosure of discretionary information should not be seen as necessarily negatively impacting firm performance and value (Verrecchia, 1983; Botosan, 1997).

In light of the above theoretical and practical developments, it is not surprising that the expansion of both the functions and roles of corporate governance on the one hand, and of voluntary disclosure, and in particular of reporting models other than the traditional financial one, on the other hand, has brought about a rising level of attention paid to the linkages between these two areas. In this picture, growing consideration is being given today to a better understanding of the corporate governance determinants that underlie the decision by corporate boards and managers to adopt and publish non-financial reporting formats. More and more, information about how this is organised influences perceptions and actions of companies. In this respect, the way in which organisations report externally on their activities and performance can be interpreted as the result of the mindsets and behaviours of those people who govern them, namely, the board members and the management team. Evidently, by implementing and communicating on their reports company’s strategies, structures, and internal procedures, those people can also convey messages and diffuse an organisational culture that points to specific directions as opposed to others. Indeed, information and the way it is structured influence perceptions and actions in and around companies.

On the other hand, the relationship between corporate governance and reporting is not limited to an organisation’s boundaries. External governance mechanisms, represented by institutional forces and national cultures, do play a role (La Porta et al., 2000; Duong et al., 2016). In this respect, it can be observed that national corporate governance Codes have also moved towards the recognition and inclusion of these new non-financial reporting languages and forms (see Chapter 2).

As to academic research, the influence of corporate governance mechanisms vis-à-vis the choice to embrace a given reporting practice has been subject to long scrutiny and debate. Many studies, based on differentiated theoretical approaches, have investigated the corporate governance features as explanatory factors of different types of disclosure, such as those relating to financial reporting, Corporate Social Responsibility (CSR), and Intellectual Capital (IC). However, only a few papers thus far have analysed the influence of corporate governance variables on the adoption of integrated reporting and the quality and credibility of this form of accountability. Even fewer studies have investigated this link in terms of board members’ experience and background, even though different voices have recently advocated that also the diversification of the board is key for a balance between shareholder/stakeholder-ism, and namely long-term value creation (Barton, 2011; FCLT Global, 2019; Coffee, 2020) (for more depth, see Chapter 3). This perceived gap in the literature inspired the making of this book.

Within this frame, this introductory chapter intends to delineate some of the general issues associated with the relationship between voluntary disclosure and corporate governance, focussing on integrated reporting in the second part of this section.

Disclosure, voluntary disclosure, and corporate governance: some introductory remarks

Since the 1990s, an increasing interest in the issue of corporate disclosure has been manifested by legal systems, regulatory bodies, and investors. Following the financial scandals that occurred in the past decades, the increased awareness of the relevance of corporate information for an efficient functioning of financial markets, as well as the progressive articulation of the con...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Dedication

Table of Contents

List of illustrations

Foreword

Acknowledgments

1 Introduction

2 Corporate governance and integrated reporting: an international perspective

3 Corporate governance and voluntary disclosure: a review of the literature

4 From theory to practice: board characteristics, financial performance, and the adoption of integrated reporting

5 Boards, reporting, and long-term value creation: towards an integrated view

Appendices

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Integrated Reporting and Corporate Governance by Laura Girella in PDF and/or ePUB format, as well as other popular books in Business & Accounting Standards. We have over 1.5 million books available in our catalogue for you to explore.