- 398 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

This new edition of this classic title, now in its seventh edition, presents a balanced and comprehensive introduction to the theory, implementation, and practice of time series analysis. The book covers a wide range of topics, including ARIMA models, forecasting methods, spectral analysis, linear systems, state-space models, the Kalman filters, nonlinear models, volatility models, and multivariate models.

Information

Publisher

Chapman and Hall/CRCYear

2019Print ISBN

9781498795630

9781138066137

Edition

7eBook ISBN

9781498795661

Chapter 1

Introduction

A time series is a collection of observations made sequentially through time. Examples occur in a variety of fields, ranging from economics to engineering, and methods of analysing time series constitute an important area of statistics.

1.1Some Representative Time Series

We begin with some examples of the sort of time series that arise in practice.

Economic and financial time series

Many time series are routinely recorded in economics and finance. Examples include share prices on successive days, export totals in successive months, average incomes in successive months, company profits in successive years and so on.

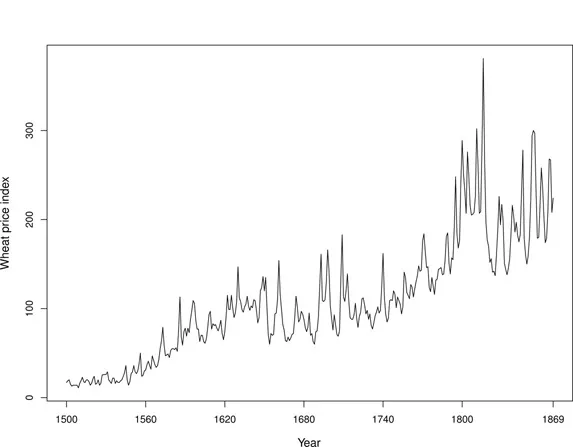

The classic Beveridge wheat price index series consists of the average wheat price in nearly 50 places in various countries measured in successive years from 1500 to 1869 (Beveridge, 1921). This series is of particular interest to economics historians, and is available in many places (e.g. in the

tseries package of R). Figure 1.1 shows this series and some apparent cyclic behaviour can be seen. The trend of the series will be studied in Section 2.5.2.

To plot the data using the

R statistical package, you can load the data bev in the tseries package and plot the time series (the > below are prompts):> library(tseries) # load the library> data(bev) # load the dataset> plot(bev, xlab="Year", ylab="Wheat price index", xaxt="n")> x.pos<-c(1500, 1560, 1620, 1680, 1740, 1800, 1869)# define x-axis labels> axis(1, x.pos, x.pos)

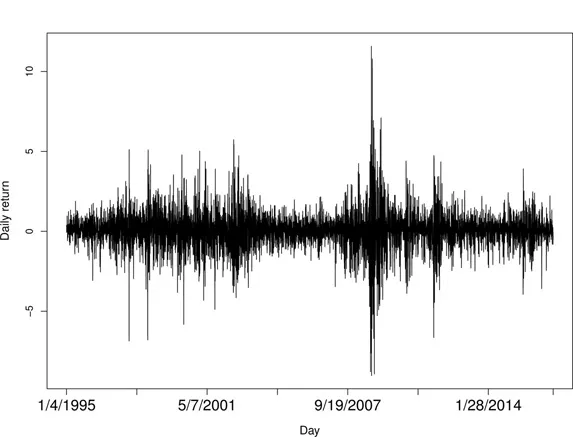

As an example of financial time series, Figure 1.2 shows the daily returns (or percentage change) of the adjusted closing prices of the Standard & Poor’s 500 (S&P500) Index from January 4, 1995 to December 30, 2016. The data shown in Figure 1.2 are typical of return data. The mean of the return series seems to be stable with an average return of approximately zero, but the volatility of data changes over time. This series will be analyzed in Chapter 12.

To reproduce Figure 1.2 in

R, suppose you save the data as sp500_ret_1995-2016.csv in the directory mydata. Then you can use the following command to read the data and plot the time series.> sp500<-read.csv("mydata/sp500_ret_1995-2016.csv")> n<-nrow(sp500)> x.pos<-c(seq(1,n,800),n)> plot(sp500{\$}Return, type="l", xlab="Day",ylab="Daily return", xaxt="n")> axis(1, x.pos, sp500{\$}Date[x.pos])

Physical time series

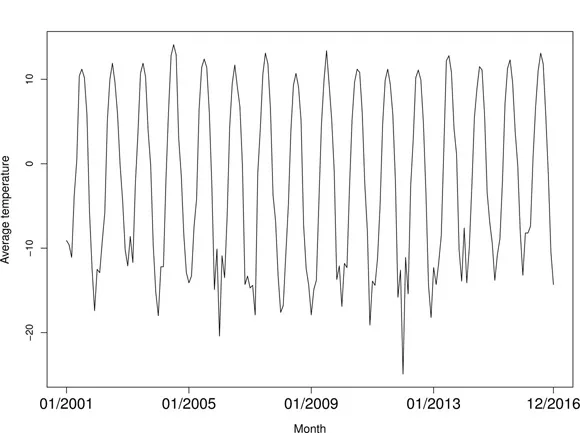

Many types of time series occur in the physical sciences, particularly in meteorology, marine science and geophysics. Examples are rainfall on successive days, and air temperature measured in successive hours, days or months. Figure 1.3 shows the average air temperature in Anchorage, Alaska in the United States in successive months over a 16-year period. The series can be downloaded from the U.S. National Centers for Environmental Information (

https://www.ncdc.noaa.gov/cag/). Seasonal fluctuations can be clearly seen in the series.

Some mechanical recorders take measurements continuously and produce a continuous trace rather than observations at discrete intervals of time. For example, in some laboratories it is important to keep temperature and humidity as constant as possible and so devices are installed to measure these variables continuously. Action may be taken when the trace goes outside pre-specified limits. Visual examination of the trace may be adequate for many purposes, but, for more detailed analysis, it is customary to convert the continuous trace to a series in discrete time by sampling the trace at appropriate equal intervals of time. The resulting analysis is more straightforward and can readily be handled by standard time series software.

Marketing time series

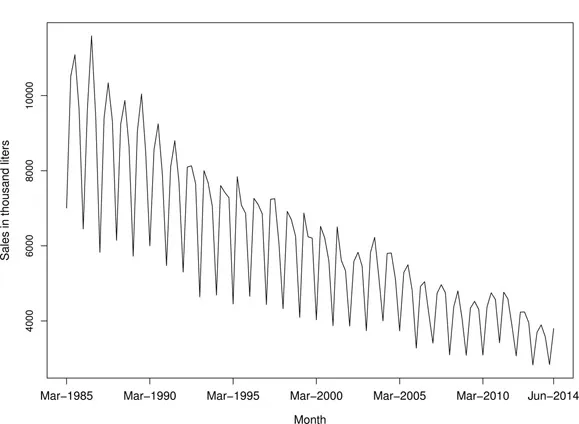

The analysis of time series arising in marketing is an important problem in commerce. Observed variables could include sales figures in successive weeks or months, monetary receipts, advertising costs and so on. As an example, Figure 1.4 shows the domestic sales of Australian fortified wine by winemakers in successive quarters over a 30-year period, which are available at the Australian Bureau of Statistics (

http://www.abs.gov.au/AUSSTATS/). This series will be analysed in Sections 4.8 and 4.9. Note the trend and seasonal variation which is typical of sales data. It is often important to forecast future sales so as to plan production. It may also be of interest to examine the relationship between sales and other time series such as advertising expenditure.

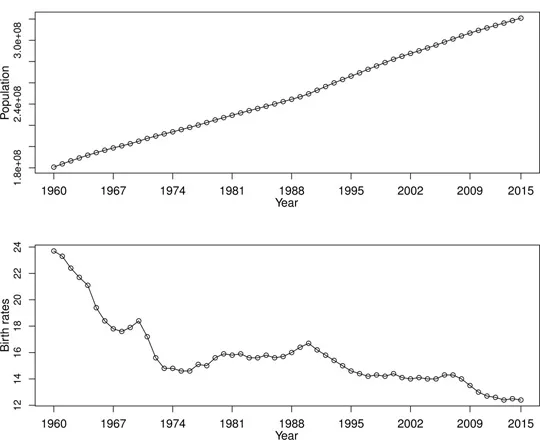

Demographic time series

Various time series occur in the study of population change. Examples include the total population of Canada measured annually, and monthly birth totals in England. Figure 1.5 shows the total population and crude birth rate (per 1,000 people) for the United States from 1965 to 2015. The data are available at the U.S. Federal Reserve Bank of St. Louis (

https://fred.stlouisfed.org/). Demographers want to predict changes in population for as long as 10 or 20 years into the future, and are helped by the slowly changing structure of a human population. Standard time series methods can be applied to study this problem.

To reproduce Figure 1.5 in

R, you can use the following command to read the data and plot the time series.> pop<-read.csv("mydata/US_pop_birthrate.csv", header=T)> x.pos<-c(seq(1, 56, 7), 56)> x.label<-c(seq(1960, 2009, by=7), 2015)> par(mfrow=c(2,1), mar=c(3,4,3,4))> plot(pop[,2], type="l", xlab="", ylab="", xaxt="n")> points(pop[,2])> axis(1, x.pos, x.label, cex.axis=1.2)> title(xlab="Year", ylab="Population", line=2, cex.lab=1.2)> plot(pop[,3], type="l", xlab="", ylab="", xaxt="n")> points(pop[,3])> axis(1, x.pos, x.label, cex.axis=1.2)> title(xlab="Year", ylab="Birth rates", line=2, cex.lab=1.2)

Process control data

In process control, a problem is to detect changes in the performance of a manufacturing process by measuring a variable, which shows the quality of the process. These measurements can be plotted against time as in Figure 1.6. When the measurements stray too far from some target value, appropriate ...

Table of contents

- Cover

- Half Title

- Series Page

- Title Page

- Copyright Page

- Dedication

- Contents

- Preface to the Seventh Edition

- Abbreviations and Notation

- 1. Introduction

- 2. Basic Descriptive Techniques

- 3. Some Linear Time Series Models

- 4. Fitting Time Series Models in the Time Domain

- 5. Forecasting

- 6. Stationary Processes in the Frequency Domain

- 7. Spectral Analysis

- 8. Bivariate Processes

- 9. Linear Systems

- 10. State-Space Models and the Kalman Filter

- 11. Non-Linear Models

- 12. Volatility Models

- 13. Multivariate Time Series Modelling

- 14. Some More Advanced Topics

- Appendix A Fourier, Laplace, and z-Transforms

- Appendix B Dirac Delta Function

- Appendix C Covariance and Correlation

- Answers to Exercises

- References

- Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Analysis of Time Series by Chris Chatfield,Haipeng Xing in PDF and/or ePUB format, as well as other popular books in Mathematics & Probability & Statistics. We have over 1.5 million books available in our catalogue for you to explore.