- 308 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

A practical, sensible plan for finding the type of self-employment that suits you, and taking charge of your own future.

If you dream of getting out of job jail—or if a layoff has left you thinking about finally pursuing your entrepreneurial dreams—this easy-to-read guide shows you how to create a Plan B business that fits your skills, interests, and preferred work lifestyle.

You will learn the four ways to create an income when there aren't any jobs available—or any jobs that interest you. Filled with stories of successes and failures, this practical book covers the good, the bad, and the ugly about each of the business models, so you can make smart decisions, avoid mistakes and pitfalls, and find a better alternative for a fulfilling life when Plan A just isn't working for you anymore.

Information

CHAPTER 1

I Worked Hard, I Played by the Rules, and This Is All I Get?

LET'S FACE IT, if you are reading this book, you are already in transition. You realize you aren't going to get what you want from what you are doing now. You need a Plan B because your Plan A job isn't working for you. You are starting to lean forward, interested to learn more about Plan B.

Let's define the terms Plan A and Plan B and the differences between them. Plan A is a job working for a company to earn a paycheck. It is the “working for the man” plan to make money. You pretty much know in advance how much you will earn based on your hourly rate or annual salary.

Plan B, as we use it, refers to the other ways you can make a living that do not involve working for someone else. For example, you may use your experience to start your own company, or you may decide to buy a business. Plan B puts you in charge of your time and the work you do. And you are writing your own paycheck.

During the past three decades the world has changed, and it's not going to change back any time soon. The rules most of us have grown up with have gone out the window. Jobs have been outsourced overseas and they are not coming back. You and many others have arrived at this new reality for any number of reasons. Some people planned all along to work for themselves, but for many others, there is no choice: a job was eliminated, a skill set was no longer needed, or declining health no longer made it possible to continue working at the same job.

Perhaps this all-too-true story will sound familiar because something similar has happened to you or someone you know. Let's use David's situation as an example.

David, a passionate sales engineer professional, was waiting his turn to find out if he was going to have a job after the latest round of layoffs. He had survived the last two rounds but was worried about this one. Sales were sliding, and management had announced they were going to reduce the number of employees to a fraction of the current staff.

David walked in the door on this particular morning and saw his manager, Jim, and the human resources manager, Stacy.

“This can't be good,” he thought. Jim and Stacy stood up. He shook their hands and they all sat down.

Stacy looked straight at David and said gently, “This is going to be a difficult conversation, David. Your position has been eliminated.”

David flinched as if he had just been punched in the gut.

“Do you need a minute or would you like us to continue?” asked Jim.

“No, go on,” David said. It's not like he wasn't expecting it, but that didn't take away the shock.

Jim and Stacy explained the layoff package and talked about the severance pay, help with his job search, and on and on.

Suddenly, David's rage exploded. He stood, yanked up his right shirt sleeve, and pointed to the company's colorful logo tattooed on the inside of his forearm. “I bleed six colors for this company. I worked hard, I played by the rules, and this is all I get?”

As David learned, loyalty to one company no longer provides job security.

Why Is Plan A Not Working Anymore?

If you're living your Plan A, you may already feel vulnerable because you realize your job could end. That's good—at least you are paying attention. Those who feel safe are either oblivious to today's reality, or in denial. If you know people like that, please give them a copy of this book; they are the ones who need to sit up and take notice.

Plan B is about making plans before you need them. The captain of the Titanic probably thought his job was pretty secure…that is, until he hit the iceberg and remembered there were not enough lifeboats for the number of passengers on board. If you don't want to go down with the ship, keep reading and get to work on your Plan B. You never know when your path may encounter icebergs.

With a job—your Plan A—you may be making a living but perhaps your lifestyle is not ideal. You are probably like most people—trading time for money, and perhaps both are running out. You may have come to realize that, although some of your bosses have been brilliant, caring, and competent, leaders in too many organizations are small-minded, self-centered individuals who may say the right things but don't really give a hoot about what happens to you. They are too busy with their own high-pressure, iceberg-filled reality.

All you've really wanted was to enjoy the company of smart, hard-working peers, be mentored by considerate and knowledgeable bosses, and ease into a comfortable retirement lifestyle at an early age. You did what they told you to do: get a good education, get a good job, and work hard. That was your Plan A.

How is that working out for you? I understand any anger. I have been there…

But don't throw this book at the nearest wall! It can be your best friend from this point on. You are about to create your own economic stimulus package by learning how to create your Plan B.

But first, let's see exactly where Plan A went astray. Consider the wisdom of the Greek historian Plutarch:

“To make no mistakes is not in the power of man; but from their errors and mistakes the wise and good learn wisdom for the future.”

The Mythical Promise of Plan A (Whatever happened to the gold watch?)

The traditional Plan A has been to work for a company for twenty, thirty, or forty years and get a lifelong pension and health care benefits. Traditionally, Plan A had a contingency for job loss; you simply go on a job search for a replacement job. Some of you may find a replacement job and be able to continue with your Plan A. Or you may find the replacement job's pay is a fraction of what you were making. And, for many, there simply are no replacement jobs. An associate's, bachelor's, or master's degree might get you a job, but there are no guarantees.

In fact, it is estimated the average person today will have changed jobs seven to ten times in their lifetime. An interesting statistic I heard recently is that the average twenty-two-year-old will change jobs twelve times by the time they are thirty-eight years old. The driving force behind this churn is the rapid advance of technology coupled with the culture shift involving the human dynamics of technology dependence.

Those in their twenties and thirties will likely never know job or career security. Even if there is a chance for job security, many younger workers simply aren't interested in staying with one company for the promise of an eventual pension decades in the future. Their future success will come from their ability to be entrepreneurial.

Whether we blame it on lack of job security or the demise of company loyalty, the fact remains…it may be time to kiss Plan A goodbye.

Financial Security Is Still Possible

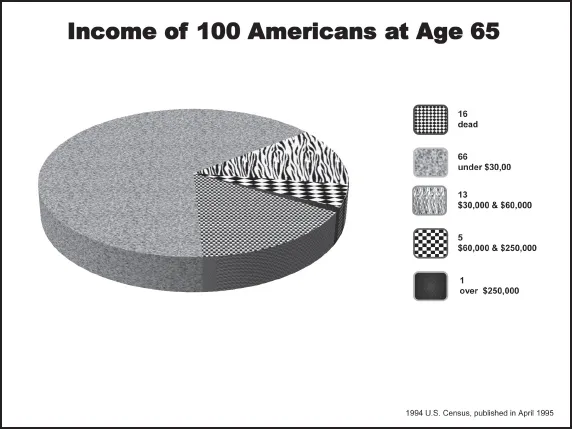

I attended a business presentation a few years ago with a US Census chart that illustrated in 1994 only five out of one hundred people in the United States achieved financial security, and only one of those enjoyed total financial freedom (defined as being able to do and have virtually anything you want, within reason.) That statistic seems to still be true today.

This book can guide you through considering—maybe for the first time—how to create your Plan B so you can become one of those enjoying total financial freedom. Take a minute to step back and think about what your environment has taught you so far. The education system has been designed to move students into jobs working for someone else. A typical high school education does not teach the basics of business, nor does a two- or four-year degree. Master's degree programs train you to be even more valuable inside an organization but do not teach you to run your own company. My undergraduate business degree and two master's degrees certainly did not prepare me for the Plan B that I had to create. Traditional influences such as schools and family may have originally led you away from creating a Plan B and urged you toward getting a job.

Now, however, a Plan B is within your reach and you have the power to create one. Like anything else you have started, it will be a journey, but this time you will have a road map of what lies ahead.

How Did We Get Here? (And where are we going?)

The details may be quite different, but the pattern is basically the same. We have made decisions that did not work out as we had planned. Additionally, local, national, and international economics have directly impacted each of us. How long it will take to recover from any losses will vary based on many things, such as the skills you have, your initiative, and the strength of the demand for what you can offer others.

The goal of this book is to help you make the best choices in these difficult times, and to give you a lot of insider information. You will learn the good, the bad, and the ugly about each of the Plan B options so you can choose yours wisely.

Clearly, I cannot know your specific goals for financial security and what you hope to be doing as you continue your work life. I can, however, show you useful, timely information so you can consider what might be possible.

Your grandparents could have lived quite well on $30,000 a year at retirement. Their mortgage was probably paid off and their lifestyle was simple. Vacations once a year were the norm. But today, the lifestyle expectations of those approaching retirement aren't about staying home and watching television. Instead, they are about traveling, volunteering, and remaining active. All of those activities cost money. And your grandparents didn't have cell phone, internet access, or cable bills to pay either.

Statistically speaking, above are the data of the average income of people in the United States from 1996.1

Who Is Going to Pay the Bills When You Retire?

One of the early working titles of this book was, “What is your Plan B, or will you have to work until you die?” It was too long for a title, but it's still quite apt as a point to ponder.

Facing the facts, most of us are going to be on our own. Social Security is a mere pittance, if it even survives the next few decades. Pension plans are pretty much becoming a thing of the past. Research on the funding levels of some local and state retirement plans for government workers revealed many of them were well below the levels needed to deliver on the promises made. That means some retirement funds don't have enough money to pay for the employee pension and medical benefits costs that have been earned by workers, and those plans will eventually run out of money. For some people, the checks will simply stop coming.

In 2000, there were approximately 68,000 people over 100 years of age in the United States. In 2050, the projected number is 834,000.

—U.S. CENSUS

Hallmark Cards sold approximately 85,000 “Happy 100th Birthday” cards in 2007.

—WSJ BLOG, “HALLMARK'S CENSUS OF CENTENARIANS,” A PRIL 10, 2008

One of the many reasons for the funding problems in both public and private sectors is that we are living longer. Life expectancy in 1950 was sixty-eight; in 2002 it jumped to seventy-seven. That means people are receiving pension payments, medical benefits, and social security checks almost a decade longer than our relatives did fifty years ago. Many more people are celebrating their one-hundredth birthday, and it takes a lot of money to live well for that long.

Companies, hit hard by the down economy, are scaling back. Of those that survive, many will no longer offer lifelong pensions or medical benefits. One Federal Bureau of Investigation (FBI) agent told me they have nicknamed their new pension plan “the work until you die plan.” New hires at a variety of organizations are told they will not have medical benefits after they retire. Certainly AT&T, GM or Citibank aren't going to offer job security or guarantee a retirement plan. Even if they wanted to, they are not able to afford it.

We all want to hold on to the lifestyle that we've worked so hard to achieve. We don't want to shrink it, or live a narrower life. Yet, many people's dreams are melting down as the economic growth stalls. Investments have destroyed many retirements. Poof! It's gone. There may not be enough hours or days left to simply work longer and harder to replenish the retirement fund.

Financial advisors just a few years ago taught us the rule of thumb that we need 65% of our yearly income to keep our same lifestyle in retirement. Then the figure went to 80%. The percent that is the right number for you will, of course, depend on your expenses and lifestyle. Be sure to discuss this with your retirement experts to determine what your happily ever after number will be.

Social Security Benefits

When it was originally introduced, Social Security was designed to offer financial assistance to help the aging population survive. But that was back in 1935, when the average life expectancy was less than sixty-five years.

When Social Security payouts began, there were, on average, over forty workers paying into the fund and their monies supported one retiree—a ratio of more than 40 to 1. With the invention of the birth control pill and family planning tactics, our country's birth rate dropped. In 2000, for example, the ratio of workers to retirees was 3.4 to 1. By 2050, or when today's college students reach retirement age, the ratio will be 2 to 1. Many other developed nations face the same concern: not enough younger workers paying social security taxes to support the growing number of seniors.1

For decades, we've heard warnings that the Social Security fund will run out of money. The most recent projection is it will be totally depleted by the year 2036.2

Besides the increase in longevity and the decreased number of workers paying taxes per retiree, another contributing factor is the repeated withdrawals on Social Security funds to balance the federal budget or to pay for other government programs. Unfortunately, social security payments are the only income many retirees will receive, which will create extreme hardship when the fund dries up.

An Illinois highway maintenance worker can earn up to $148,000 annually with overtime. The state's enhanced early retirement program will pay that person up to $75,000 per year, starting at age fifty and after twenty-five years on the job. By age eighty, that person will have received $1.2 million more than a participant would have in the state's regular retirement plan.

—FLORIDA TODAY, DECEMBER 9, 2011, “TAXPAYERS ARE LEFT WITH A TICKING TIME BOMB”

Retirement Plans Designed to Benefit…Whom?

Traditional jobs have created pensions designed to provide lifelong retirement income, even for those employees with as few as twenty years of service, regardless of the employee's age.

One example of this is the military—certainly a dangerous and demanding career. A common career choice is to join for twenty years, then retire and begin receiving a 50% pension payout right away. This is a sweet deal: join the military at age twenty, work for twenty years, retire at age forty, live until age one hundred, and enjoy a sixty-year pension payout which is three times longer than the time served in the military.

For example, one forty-something retired soldier shared with me that he retired after twenty years of service and is now receiving $31, 000 annually for the rest of his life. It is not enough to fund a great lifestyle, true, but it is a steady check.

The problem is that no government or organization can sustain that kind of cash outlay for long...

Table of contents

- Cover Page

- Title Page

- Copyright Page

- Table of Contents

- Introduction

- Chapter 1 - I Worked Hard, I Played by the Rules, and This Is All I Get?

- Chapter 2 - Is Your why Bigger than Your BUT?

- Chapter 3 - The Real Deal about you

- Chapter 4 - There are Many Paths to a Plan B

- Chapter 5 - Thinking it Through: Avoiding the Pitfalls of Wrong (and Costly) Decisions

- Chapter 6 - Six Key Ingredients of the Most Successful Businesses

- Chapter 7 - The Real Deal about Starting Your Own Business

- Chapter 8 - The Real Deal about Buying a Business

- Chapter 9 - The Real Deal about Buying a Franchise

- Chapter 10 - The Real Deal about Network Marketing

- Chapter 11 - Putting Your Plan B into Action

- Appreciation & Acknowledgements

- Resources and Offers

- About the Author

- Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Plan B by Kathleen Rich-New in PDF and/or ePUB format, as well as other popular books in Business & Entrepreneurship. We have over 1.5 million books available in our catalogue for you to explore.