![]()

1

Local Economic Development in a Global Market

The vast majority of decisions affecting local economic development (LED) are made by private individuals or institutions. Often the decisions are made by persons living half a world away from the affected locality. These choices are generally made on the basis of self-interest after consideration of the costs and benefits. Many economic development practitioners seek to understand how market processes operate so that they can help their organizations make good decisions. Others seek to influence private economic decisions by affecting the real or perceived costs and benefits of decisions so as to stimulate economic development. In both cases, it is essential to understand how the market economy operates. This chapter describes how economists view economic activities and serves as a point of departure for understanding the development process.

How Economists View the World

Students who have not studied economics sometimes fail to understand the role of models and assumptions in economic analysis, the economist’s view of individual behavior, and how disagreements about policy can arise. A sketch of these important aspects of the economic paradigm will set the stage for further analysis.

MODELS AND ASSUMPTIONS

Economists often build deductive models to help understand economic processes. Models are deliberate simplifications of reality because the economy includes so many variables that interact with each other in so many ways that we can understand process only by focusing on a few variables at a time. The variables not under consideration are usually assumed to stay the same, the well-known “ceteris paribus” or “other things equal” assumption. For instance, when thinking about how quality of life may affect job growth, it is necessary to assume that the state of the national economy and other critical variables do not change when comparing areas. Otherwise, a city with very poor quality of life located in a fast-growing area might show higher job growth than a city with high quality of life in a slow-growing area.

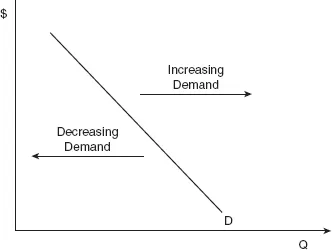

An important application of the “other things equal” assumption is found in the law of demand. It states that if the price of a good falls, the quantity individuals are willing and able to consume will increase, holding other things equal. Figure 1.1 is a demand curve consistent with the law of demand; it slopes downward. Changes in tastes and preferences, incomes, the price of other goods, expectations, and market size could result in a situation where the relation between price and quantity demanded could appear to violate the law of demand. For instance, price and quantity demanded could increase at the same time if the size of the market also increased. Therefore, to focus only on the relationship between price and quantity sold, it is necessary to make explicit the assumption that everything stays the same except price and quantity.

Students often object to the many assumptions that are incorporated in economic models because they are unrealistic. In reality, other things do not remain equal, so why do economists assume that they do? The value of the assumptions is that they provide a systematic framework for analysis, and they may be relaxed so that the impact of changing certain assumptions may also be analyzed. For instance, the assumption that the size of the market or incomes do not change may be replaced by the assumption that market size or incomes increase. Then it can be shown that increases in market size or incomes will shift the entire demand curve to the right (called an increase in demand).

Figure 1.1 The Demand Curve

NOTE: The demand curve shows how many units of a product consumers will purchase at various prices. Under some conditions, the demand curve represents social benefits. Thus, someone would value the 10th unit at $5. Changes in income, market size, price of other goods, preferences, and expectations could cause the demand to increase or decrease.

Spatial economic models are often predicated on unrealistic assumptions, such as perfect knowledge, profit-maximizing behavior, uniform transportation costs, consumers with identical tastes, and homogeneous space. The insights gained from these models can be increased if consideration is given to how the models will be affected if the assumptions were changed. Changing the assumptions of a model provides insights about the variables that were being held constant.

INDIVIDUAL BEHAVIOR AND UTILITY MAXIMIZATION

For most economists, individuals are the building blocks from which group actions emerge, so it is important to understand what motivates them. The powerful assumption that economists make is that individuals are motivated to maximize their own utility. Money provides utility, but so do other things, such as love. In the sphere of economic development, money is usually the most powerful motivator, but individuals also receive satisfaction from things such as helping their community.

Adam Smith highlighted the importance of self-interest:

It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their own self-interest [in trying to get these things]. … We address ourselves, not to their humanity but to their self love, and never talk to them of our own necessities but of their advantages.

According to Adam Smith, a market system creates rewards and incentives that encourage utility-maximizing individuals to do what is in the public interest as if they were guided by an “invisible hand.”

Disagreements about the extent to which individuals seeking their own self-interest actually serve the public interest are at the heart of the debate between those who believe in “letting the market operate” and those who believe that government involvement is important for successful economic performance.

Economists also assume that individuals are rational in their efforts to maximize utility. The rationality assumption is essential if economic models are to predict behavior. If individuals did not act rationally, then all behavior could be explained as the result of irrational actions.

Students sometimes object to the concept of utility-maximizing man. One objection is based on the mistaken idea that utility-maximizing behavior is selfish. In fact, economists recognize that altruistic behavior can provide satisfaction to some individuals. The second objection is that the utility maximizing assumption does not examine how tastes and preferences are formed or why individuals differ in how they attain satisfaction. Economists tend to assume that individuals have a set of preferences, but little attention is given to how preferences are formed. It is likely that if economic life and social life were different, individuals would have a different set of preferences. Urban and regional economists often rely on the work of psychologists, sociologists, and planners, who are more informed about questions of preference formation.

IDEOLOGICAL PERSPECTIVES ON MARKET OPERATIONS

Economists explore two distinct types of questions. On the one hand, positive questions address the world as it is. On the other hand, normative questions inquire about how things should be or ought to be and involve value judgments. Economists disagree about appropriate policies either because of different analyses of how the economy operates (positive) or because they have different values (normative).

Sometimes policymakers are more concerned with economic growth than static efficiency, particularly individuals involved in economic development. A community that operates inefficiently but grows rapidly may be better off in the long run than a community that maintains a high level of static efficiency but does not grow rapidly.

Economic development policies are cast in a way that forces policymakers to choose between static efficiency and economic growth. Some critics of economic planning suggest that too much planning stunts growth because unemployed resources are necessary for innovation and the development of new products.

Equity refers to fairness. When a policy change hurts some individuals but benefits others, questions of fairness arise. If income is tilted too much toward one group, it may be difficult to maintain social stability. Imbalances in the distribution of income may reduce economic prosperity. Economists are not very good at deciding which actions are more equitable, because such decisions cannot be made on scientific grounds. Nevertheless, the appropriateness of most changes must be decided, at least partly, on the basis of fairness.

There are two alternative perspectives on the extent to which government involvement in the economy may improve economic welfare—conservative and liberal.

The conservative perspective places a high value on economic freedom and economic efficiency. Many conservatives agree with Friedman (1962) that capitalism is necessary for political freedom. The analyses of conservative economists tend to show that the laissez-faire market works well. When competitive market conditions exist, individuals seeking their own self-interest act in society’s interest. Consequently, conservatives tend to oppose government involvement in regional and urban problems. Even when their analysis leads them to believe that market outcomes are imperfect, conservatives tend to believe that imperfect market outcomes are preferable to government-imposed solutions (which may also be imperfect).

Liberal economists tend to place a high value on economic equity when viewing market operations as sometimes both inefficient and inequitable but still useful. Blinder (1987) referred to the liberal philosophy as combining respect for the efficiencies of the free market with concern for those the market leaves behind. Consequently, liberals tend to believe that government action is important for solving urban problems and securing a more equitable distribution of income. Fundamentally, liberals want to maintain the basic framework of market decision making; but they believe that there is substantial potential for government actions to improve market outcomes. In particular, government regulations and taxes may help when markets are not operating as they should.

Conservatives and liberals constitute the mainstream of economic thinking. Both perspectives rely on the market to provide information and establish the basic incentives that encourage socially desirable behavior. Most of the policy issues discussed in this text are within the liberal-conservative framework.

Radical economic analysis is outside mainstream thinking and often provides interesting challenges to traditional economic thinking. Radical economists are distrustful of the market. Many radical economists believe that the market is not an impartial mechanism that helps organized economic activities. Rather, the market is a means of social control. They are less concerned with whether market mechanisms are efficient than they are with whose interests the market serves. Government programs that affect economic outcomes often help the wealthy because the same interests that control the market also control government. Radicals tend to see urban problems as a reflection of class conflicts. Radicals see greater government involvement in the economy, including direct ownership of productive resources, as a more preferable solution to problems than either a policy of laissez-faire or government modification of market outcomes.

How Markets Work

Markets are a process (not a place) through which buyers and sellers conduct transactions. Markets coordinate numerous economic decisions and provide incentives that influence behavior. To emphasize these important functions, Milton Friedman has claimed that no one in the world knows how to make a pencil. He meant that no one knows how to complete all the steps in the process—cutting the trees, mining the graphite, and so forth. Yet the market helps coordinate these decisions, and many more. Prices tell producers which components of the pencils are needed, what kinds of pencils folks want and provide an incentive for production and an incentive to use less.

When the market is working well, the incentives generated by the market encourage individuals to behave in a way that benefits society. For instance, when a community’s economy starts to decline, local resources become idle. Prices of land, labor, intermediate goods, and other resources may fall. The declining prices send two signals. (1) If you own productive resources, do not bring them to this region because the resources can earn more elsewhere. Thus, new workers may not relocate to the area, and current residents may consider leaving. (2) At the same time, falling resource prices might encourage producers, wishing to employ resources, to consider relocating or starting in the region.

The example of community decline illustrates a situation where the market is working well. However, the market does not always generate outcomes that are socially beneficial. When markets create suboptimal or perverse outcomes, government officials attempt to intervene. Sometimes the interventions involve small changes in incentives, or “tweaking” the market, and at other times the market may be completely overridden.

Bartik (1990) contended that appropriate interventions in market outcomes is the hallmark of successful LED policy. Accordingly, an understanding of how markets operate is a prerequisite to understanding the forces that shape local economies and development policies.

SUPPLY AND DEMAND

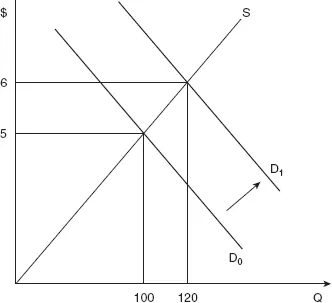

Figure 1.2 illustrates how supply and demand operate. The demand curve shows how consumer purchases will be affected as prices change, other things being equal. Similarly, the supply curve shows the quantity of output producers would be willing and able to sell at various prices. The higher prices will induce businesses to produce greater output, other things equal.

Let D0 be the operative demand curve. Price will be determined at the point where the quantity supplied and quantity demanded are equal, Point a in Figure 1.2. The price will be $5. At that price, consumers will produce 100 units, and consumers will purchase 100 units. At any other price, there will be either a shortage or surplus of the product. The $5 price is considered an equilibrium price because once it is attained it will not change unless the supply or demand curves shift. It may take the market a long time to find the equilibrium price; so at any given time, the actual price may not be in equilibrium.

Figure 1.2 Supply and Demand

NOTE: The initial price and quantity of a product are determined by the initial demand and supply curves D0 and S, respectively. Equilibrium price and output will be $5 and 100 units, respectively. If demand increased to D1, price and output of the product would increase to $6 and 120 units, respectively.

Suppose that economic development caused the population and incomes of residents to increase. As a result, the demand curve will increase from D0 to D1. Price and output will increase. Immediately, we can visualize one of the impacts of economic development on the demand for local products. Similarly, factors that increase the demand for the output of local establishments can contribute to LED. For example, if demand for American-made cars increased, communities with automobile production facilities would probably experience increases in employment as the output of automobiles increased.

SUPPLY, DEMAND, AND EFFICIENCY

When there are many well-...