While the coronavirus disease (COVID-19) has resulted in severe global health and economic crises, it also presents an opportunity for a green, sustainable, and resilient recovery enabled by sustainable energy. This guidance note examines the effects of COVID-19 on the energy sector in Asia and the Pacific. It looks at how the sector has responded so far and outlines key actions that energy stakeholders can take during the response and recovery phases. The guidance note also highlights how the Asian Development Bank's support to the energy sector is helping its developing member countries recover from the pandemic and achieve sustainable development.

- 48 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Topic

BetriebswirtschaftSubtopic

Energiebranche1 Introduction

Solar panels gathering sun power and turbines harvesting wind power at the Burgos Wind and Solar Farm in Burgos, Ilocos Norte in the Philippines (photo by Al Benavente/Asian Development Bank).

Energy supply and system operations around the globe have been able to meet demand reliably during the pandemic, despite concerns over personnel shortages throughout lockdowns and travel restrictions that put limitations on operation and maintenance (O&M). The main effects in the energy sector have included decreasing commodity prices for fossil energy (including oil, natural gas, and coal) as a result of decreased final energy demand and decrease in overall power demand, but with increased demand in the residential sector and limitations on personnel mobility which slowed down project development and implementation.1 While the entire global energy system has been affected, the way each country has been affected varies substantially.

The coronavirus disease (COVID-19) has affected countries as a whole, but the abovementioned effects have been more acutely felt in urban centers. While commercial, public, and social services were either halted or partially restricted during lockdown, there was still a need for Required Core Urban Service Standards.2 These service standards are broadly crosscutting and while energy is directly needed in both heating and cooling and electricity, energy remains essential in delivering all core urban services.

During quarantine and lockdown, the measures that were put in place to prevent the spread of COVID-19 resulted in a significant reduction in pollutants due to less mobility and decreased electricity demand and industrial production (which are primarily dependent on fossil fuels). While this is a positive development in terms of air quality due to the reduction in greenhouse gases (GHGs), making these reductions permanent requires structural changes—in particular, building upon or creating policies that focus on measuring and managing urban air quality and indoor air quality to encourage energy efficiency and clean energy use.

In Metro Manila, Philippines, for example, during the first 30 days of enhanced community quarantine, fine particulate matter (PM2.5) levels were at the lowest on record. Nitrogen dioxide (NO2) levels were over 50% lower compared to 2019. While this was likely due to reduced transportation activity, large reductions in fossil fuel-based power production was also likely to have contributed to the decline in air pollution levels. When the country moved to enhanced general community quarantine, which was less restrictive, the levels of both PM2.5 and NO2 rebounded to levels seen just before the enhanced community quarantine.3 This rebound was also seen in Delhi, India where NO2 levels dropped by over 40% during the country’s COVID-19 lockdown, but had nearly rebounded to pre-COVID-19 levels by mid-August.4

In both the Peoples’ Republic of China (PRC)5 and in Europe,6 satellite data have demonstrated a significant reduction of NO2 in urban centers during the time when major limitations were placed on the movement of populations and industries were shut down to stem the spread of the virus. The initial data demonstrated that while the PRC slowly reduced restrictions and brought its economy back to life, NO2 emissions increased.

While the response to dealing with the virus and the economic implications of such drastic measures is not the actual solution to addressing pollution, it does offer a vision of what clear skies look like, and the value of fresh air. Beyond these qualitative observations, it provides increased data on the sources and effects of the pollution that can be used to inform the interventions that may be used to clean the air and mitigate climate change, while at the same time providing jobs and bolstering economic activity. Annual emissions in 2020 are projected to be lower than 2019 by a significant amount, but this is not necessarily a structural change. After the 2007–2008 Great Financial Crisis, emissions rebounded to a level higher than before the crisis.

For suppliers of both primary and secondary energy, this has reduced revenue, while for many, the costs of operation have not diminished to the same degree, creating a negative financial impact. For end users, reduced prices of some energy sources have resulted in savings (such as reduced diesel prices for fossil fuel-based power production). However, unit retail prices for power have not decreased, and therefore increased residential use has resulted in increased costs that have been a burden for lower socioeconomic populations. Power utilities, many of whom were not in strong financial shape before the pandemic, have felt a major impact due to decreased demand (resulting in decreased revenue), while remaining fixed and variable costs have been combined with customers who are unable to pay due to broader economic effects of the pandemic. Such financial stressors can result in reduced O&M spending as well as decreased investment in new infrastructure, leading to lower levels of service or lack of progress to improving energy services. This may also limit countries’ efforts to address energy-related emission as part of their Nationally Determined Contributions to the Paris Agreement.

The financial effects across economies caused by the COVID-19 pandemic have been significant and continue to grow for many countries. The response to these effects will require economic stimulus to rebuild and revitalize economies. Government responses to the health impacts of COVID-19 indicate a clear willingness to provide funding at scale to counter immediate public health effects. Reducing conventional pollutants (especially PM2.5, which is linked to higher risk of susceptibility to COVID-19, and NO2, which is an indicator of local air pollution and GHGs) is also attracting increased attention for investment that has not historically been forthcoming for carbon mitigation pathways envisioned under the Paris Agreement.

Orienting stimulus to support sustainable energy systems will support economic recovery from the pandemic. The former UN Secretary-General Ban Ki-moon is quoted as saying, “Energy is the golden thread that connects economic growth, increased social equity, and an environment that allows the world to thrive.” Developing member countries (DMCs) of the Asian Development Bank (ADB) will increase their energy use as they develop economically. On this basis, it is expected that a share of stimulus offered in response to the economic effects of COVID-19 will flow into the energy sector. As countries consider the use of stimulus for economic rebuilding, it will be essential to make the most of these resources and may create an opportunity to address structural energy sector problems, both from a technical and policy perspective (e.g., inefficient generation, sub-cost recovery tariff structures, fossil fuel subsidies, ineffective or absent regulators, fossil fuel investments leading to future stranded asset risk in a low-carbon society).

Many low-carbon technologies have increased in performance while decreasing in costs over the past 10 years as many countries have gained significant experience in deployment.7 Technology choice will depend on the specific status and resources of the country, but there is a strong rationale to use the pandemic recovery period to invest in clean energy technologies.8 For example, both solar and wind power technologies can often offer long-term cost savings over conventional power production from coal, gas, and oil. Energy efficiency technologies can be deployed to limit increases in energy demand as countries increase in economic prosperity. These rationales provide the impetus for countries to begin investing in clean energy technologies at this time as ongoing performance improvements and cost reductions are expected to increase the value of these technologies further in the future. Investments in conventional pollution control and increased emphasis on technology innovation, with climate change benefits, could be areas of opportunity for investment by DMCs with long-term benefits.9

ADB has continued to invest in its DMCs as they struggle to manage during the COVID-19 pandemic and the recovery phase. The need for modernized energy systems is essential to meet the Sustainable Development Goals (SDGs) and ADB will continue to support the low-carbon transition as committed under the Paris Agreement (including reductions of GHGs and other air pollutants). In this respect, ADB’s current energy sector operations are well aligned with the needs of DMCs. There is also an opportunity to expand the scope of interventions to address gaps, such as access to electricity and “clean cooking,” and to increasingly leverage cross-sector opportunities for DMCs. This focus fits squarely within ADB’s mission, and aligns with its Strategy 2030.10

The purpose of this note is to (i) highlight the effects of COVID-19 on the energy sector and describe how the sector is responding, (ii) identify key actions that the broad set of energy sector stakeholders11 can take in both the response and the recovery phase, and (iii) identify the existing strength of ADB’s energy sector and how it can respond to the needs of DMCs in light of COVID-19. This note offers guidance on where to maintain ongoing areas of focus and where to place increased focus to address gaps in support of sustainable development in DMCs. Insights shared in this guidance note are expected to be of relevance and interest to stakeholders regionally and internationally as they engage to deliver resilient infrastructure in the Asia and Pacific region and beyond.

This note will focus on the primary areas where ADB invests in the energy sector: (i) power sector—including generation, transmission, and distribution, as well as end use; and (ii) natural gas transmission, distribution, and use—including liquified natural gas (LNG) infrastructure. The next steps following the development of this guidance note will require regional- and country-specific analysis to orient actions that can best address recovery from he pandemic.

2 Impacts of COVID-19 on the Global Energy Sector

Sri Lankan health workers wearing protective gears and carrying out tests for COVID-19 in Colombo, Sri Lanka. Energy systems have been successfully operating during the pandemic, supporting the health sector, education, and overall societal activities (photo by M.A. Pushpa Kumara/Asian Development Bank).

The global energy sector consists of a highly interrelated set of resources being used for a broad range of end uses that support economic activity and societal well-being. The sector includes a wide range of actors that include public and private sector stakeholders. For example, the power sector uses a range of fuels from fossil-based products (oil, natural gas, coal, or diesel); renewables (photovoltaics, wind, geothermal, hydro); and nuclear for generation. The power that is generated is then distributed through transmission and distribution infrastructure to consumers at different prices depending on the sector (industrial, commercial, or residential). In addition to this, some industry actors produce their own power and some last-mile customers use small-scale individual systems to meet modest power needs. The stakeholders involved in the process can include all levels of governments, utilities, independent regulators, private sector firms, and financiers. While the technical aspects of power generation, transmission, and distribution; and demand, are virtually the same in all countries, the structure of policy, regulation, and wholesale and retail markets varies from country to country.

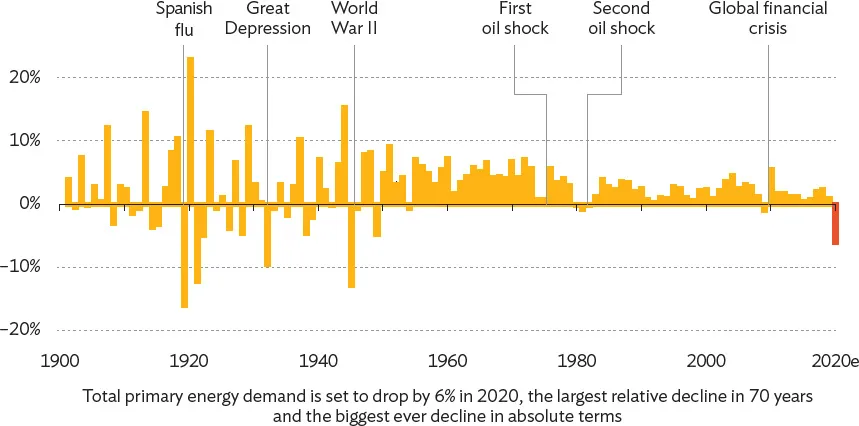

The demand for energy has dramatically decreased during the initial lockdown periods and the economic effects have resulted in year-on-year decline in 2020. The demand in some countries is recovering, but on a global basis, it is estimated that overall primary energy demand will decrease by over 5% year-on-year in 2020. The decrease in energy demand is much greater in 2020 than any experience in the past 7 decades (Figure 1). This would amount to a shock around seven times larger than that which occurred during the 2007–2008 financial crisis.

Figure 1: Change in Global Primary Energy Demand, 1900–2020e

Note: 2020e = estimated values for 2020.

Source: International Energy Agency (IEA). 2020. Global Energy Review. Paris.

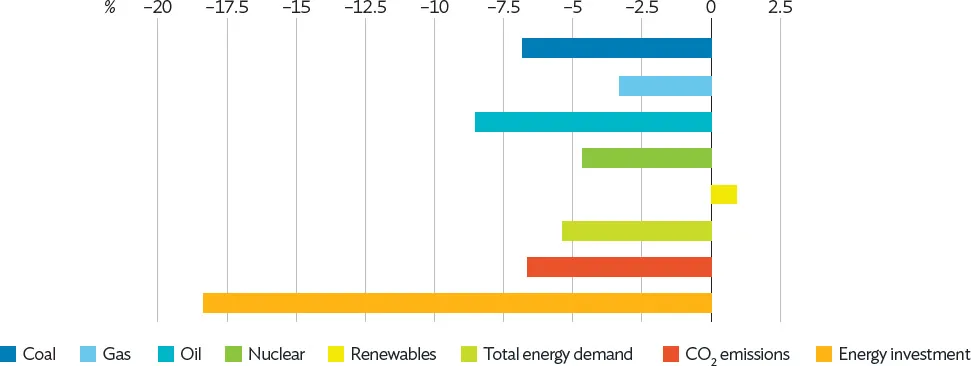

All fuels have experienced decreases in demand, except renewables (Figure 2). The reduction in GHG emissions is welcome, but is not structural in nature; rather, it is only related to the economic downturn and reduced transport acitivity during the pandemic. The reductions in energy sector investments will have both direct economic effects, especially in fossil fuel-producing countries, but also may temporarily halt investment strategies to enable reorientation toward low-carbon solutions.

Figure 2: Comparison of Energy Demand, Carbon Dioxide Emissions, and Investment Indicators (2020, Relative to 2019)

CO2 = carbon dioxide.

Source: International Energy Agency (IEA). Key Estimated Energy Demand, CO2 Emissions and Investment Indicators, 2020 Relative to 2019. Paris.

The decrease in electricity demand is less pronounced at a modest 2% and renewable generation is expected to surpass 2019 levels. This is due to its preferential position in the merit order due to low operating costs, as well as the increased capacity still being constructed and coming on line throughout 2020.

Annual GHG emissions are estimated to decrease by 7% in 2020. According to the Climate Action Tracker, a 4%–11% reduction could occur in 2020, and between 1% above and 9% below 2019 emissions in 2021, depending on the magnitude and length of the economic turndown.12 However, emissions are likely to rebound fairly quickly, and a short-term increase due to pent-up demand is also possible, based on experience from the global financial crisis.13 Global GHG emissions fell by 1.2% in 2009; however, the deployment of large stimulus packages was followed by a 5.9% rebound in 2010—well above the long-term average growth in emissions of around 2%.14

Global Trends in the Oil and Gas Sectors and Effects on Developing Member Countries

The decline in transport activity during the pandemic has had massive impacts to global oil demand. Global demand in oil decreased by 25% year-on-year in April 2020 largely due to the sharp drop in transport activity both domestic and globally (mobility consumes over 50% of global oil product supply), but also due to reduced demand in industrial sectors. This decrease in global demand, together with other geopolitical facto...

Table of contents

- Front Cover

- Title Page

- Copyright Page

- Contents

- Tables and Figures

- Abbreviations

- Executive Summary

- 1 Introduction

- 2 Impacts of COVID-19 on the Global Energy Sector

- 3 Guidance for Energy Sector Response and Recovery in the COVID-19 Context

- 4 ADB Support to Developing Member Countries in the Energy Sector

- 5 Conclusion

- Footnotes

- Back Cover

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access COVID-19 and Energy Sector Development in Asia and the Pacific by in PDF and/or ePUB format, as well as other popular books in Betriebswirtschaft & Energiebranche. We have over 1.5 million books available in our catalogue for you to explore.