The Economics of Banking provides an accessible overview of banking theory and practice. It introduces readers to the building blocks of fundamental theories and provides guidance on state-of-the-art research, reflecting the dramatic changes in the banking industry and banking research over the past two decades.

This textbook explores market failure and financial frictions that motivate the role of financial intermediaries, explains the microeconomic incentives and behavior of participants in banking, examines microlevel market stress caused by economic recessions and financial crises, and looks at the role of monetary authorities and banking regulators to reduce systemic fragility as well as to improve macroeconomic stability. It delivers broad coverage of both the micro and macroeconomics of banking, central banking and banking regulation, striking a fine balance between rigorous theoretical foundations, sound empirical evidence for banking theories at work, and practical knowledge for banking and policymaking in the real world.

The Economics of Banking is suitable for advanced undergraduate, master's, or early PhD students of economics and finance, and will also be valuable reading for bankers and banking regulators.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Banks are among some of the most important yet sometimes the most controversial institutions in an economy. Banks provide socially desirable services for households, firms, and other financial institutions, but bank failure often costs enormously for taxpayers and economic growth. In this chapter, we will take a brief look inside the banking industry, explain terms and jargon that we will use frequently in the rest of this book, and focus on the features in banking that make banks and the economics of banking special.

According to Encyclopædia Britannica, a bank is “an institution that deals in money and its substitutes and provides other money-related services. In its role as a financial intermediary, a bank accepts deposits and makes loans”. That is, a bank provides financial intermediation services between lenders and borrowers, collecting funds from lenders and lending the funds to borrowers; of course, nowadays, we shall also interpret “deposits”, “loans”, “depositors”, and “borrowers” more broadly. In addition, the boundary between banks and other types of financial institutions is becoming more and more blurred, for example, certain financial institutions such as mutual funds also provide financial intermediation services. In the narrow sense, only a financial institution that carries a banking license that is issued by banking authority is legally classified as a bank. However, as many of the issues discussed in this book are applicable to a wide variety of financial intermediation services which do not necessarily take place in these narrowly defined banks, we do not confine ourselves with such narrowly defined banks, and sometimes we use “bank” and “financial intermediary” interchangeably.

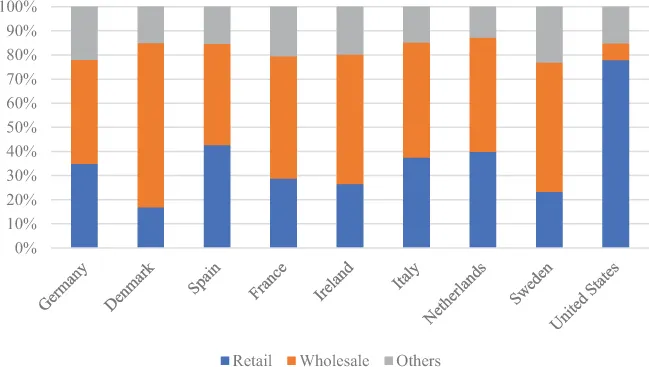

Box 1.1 (p.14) presents an anatomy of a highly stylized bank that allows us to see what a typical bank does and how we can measure its banking outcomes and performance. The balance sheet in the Box characterizes the sources from which the bank raises funding, i.e., in its liabilities, and how these funds are invested, i.e., in its assets. Typically, a bank can raise funding from a large variety of entities, for example, from individuals via checking accounts or savings accounts (retail deposits), from other banks via interbank lending (wholesale funding), from financial markets via issuing bonds or other financial securities, from shareholders, etc. Figure 1.1 shows a decomposition of banks’ funding in the US and several European countries. For many developed European countries, retail deposits only account for less than half of total bank liabilities, while funding from other financial institutions, or, wholesale funding, accounts for a larger share. In contrast, retail deposits account for a much larger share in the US. Furthermore, banks are typically highly leveraged institutions, with much higher leverage ratios than non-financial firms. Given the limited liability of a bank, high leverage ratio implies that its shareholders only incur a small share of bankruptcy cost when the bank goes bust; this creates a potential for banks to take excess risks.

Figure1.1 Sources of bank funding for banks in Europe and US, as percentage of total liabilities, as of 2019Q4

Notes: vertical axis is in percentage points. Sources of bank funding include retail deposits, wholesale funding, and others. Data source: European Central Bank Statistical Data Warehouse, available on https://sdw.ecb.europa.eu/, and FDIC Historical Bank Data, available on https://banks.data.fdic.gov/explore/historical.

Usually, a large share of funds are lent out as loans, to households, firms, financial institutions, etc. Banks are investing in financial assets, too, such as stocks and bonds; investment activities are nowadays of increasing importance for many banks. Banks also hold cash and other “liquid assets” such as government bonds that can be easily converted to cash, often as reserves to meet depositors’ withdrawal demand. Overall, through standard intermediation, a bank collects funding from creditors at certain funding cost (for example, interest rate for deposits), and issues loans to borrowers at loan rates that are higher than funding rates. The margin between these two rates is thus the bank’s profit.

Banking sector is systemically important

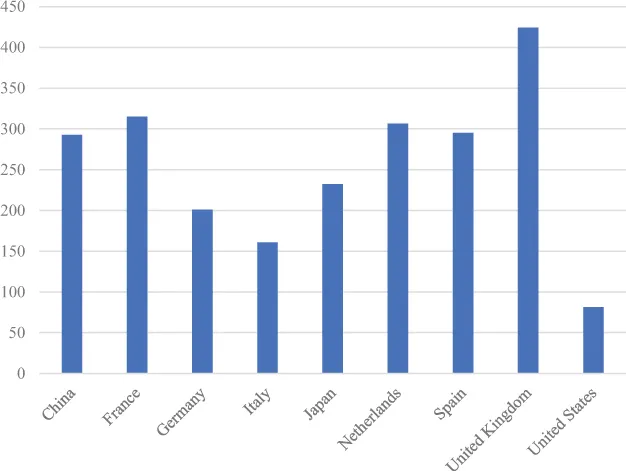

Why are banks special, then? First of all, banks are special and often gain a lot of attention among the general public, researchers, and policy makers because the banking sector is one of the most important sectors in a modern economy. Banks are mobilizing and managing an enormous amount of resources in the economy. Figure 1.2 shows bank assets to GDP ratio in a number of countries in the world, as of 2019. In many countries, the banking sector accounts for a big share of the economy: on average, total bank assets are around two to four times as large as GDP for countries in Western and Northern Europe; the banking sector is obviously larger, relative to GDP, in financial centers: for example, total bank assets in the United Kingdom are 424% of GDP, and in Luxembourg the number is 1433%, down from 2644% in 2008! In these financial centers, the banking sector also employs a large share of the labor force and makes a major contribution to GDP. On the other hand, the United States is in a stark contrast to the other big economies in the world: as an originating country of the 2007–2009 global financial crisis as well as a number of financial crashes and busts in history, the US does not have an extraordinarily large banking sector compared to the size of the economy.

Figure1.2 Bank assets to GDP ratio in nine countries, 2019Q4

Notes: computed by the author. Vertical axis is in percentage points. Data sources: China Banking and Insurance Regulatory Commission, available on https://www.cbirc.gov.cn/cn/view/pages/tongjishuju/tongjishuju.html; Bank of Japan, available on https://www.boj.or.jp/statistics/index.htm/; European Central Bank Statistical Data Warehouse; Eurostat, available on https://ec.europa.eu/eurostat/; FDIC Historical Bank Data; Federal Reserve Economic Data (FRED) from Federal Reserve Bank of St. Louis, available on https://fred.stlouisfed.org/.

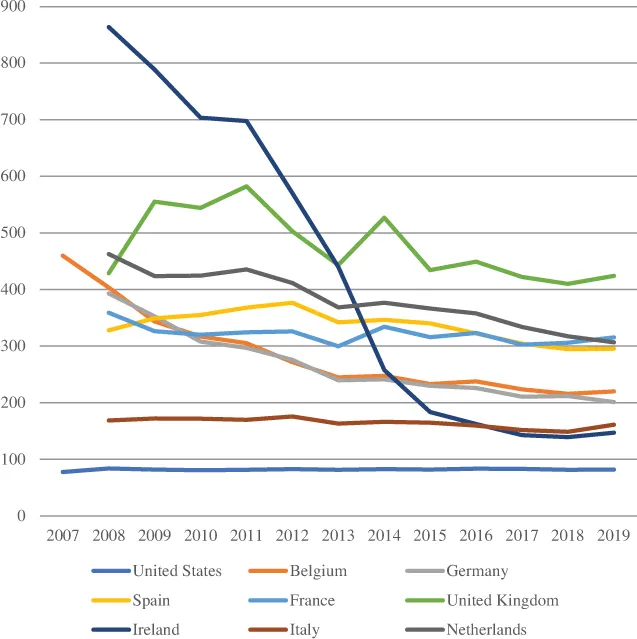

Figure 1.3 presents the evolution in the size of the banking sector across Europe and the US in 2007–2019. The banking sectors in different countries exhibit clearly different dynamics: in some countries, the banking sector stays relatively “low and stable”, such as Italy and the US; in some countries, the banking sector has been in contraction, such as Ireland and the Netherlands, and it seems the larger a country’s banking sector was at the run-up to the 2007–2009 global financial crisis, the bigger post-crisis contraction it experienced. The UK, as a financial center, made a strong recovery in its banking sector after the crisis, while the 2016 Brexit referendum seems to trigger a slow outflow of the banking business.

Figure1.3 Bank assets to GDP ratio in the US and Europe, 2007–2019

Notes: computed by the author. Vertical axis is in percentage points. Data sources: European Central Bank Statistical Data Warehouse, Eurostat, FDIC Historical Bank Data, and Federal Reserve Economic Data (FRED) from Federal Reserve Bank of St. Louis.

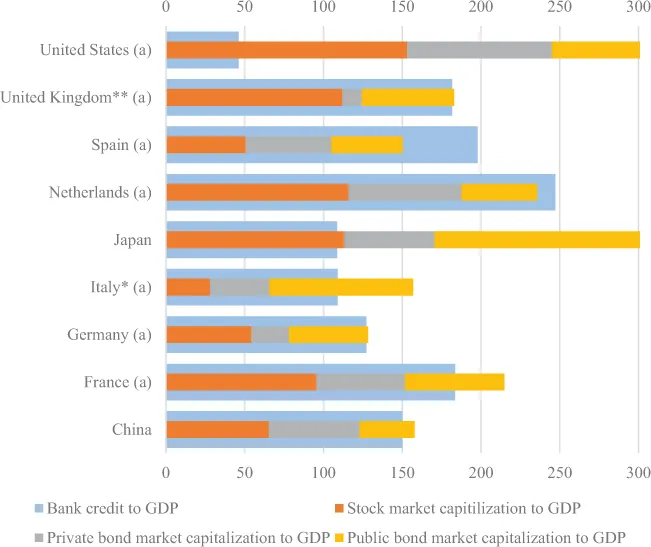

The banking sector is often a major provider of financial resources in an economy, besides other providers offering “market funding”. Figure 1.4 presents the relative importance of various funding resources across different countries, measured by the size of a funding resource relative to GDP. Besides funding by bank credit, market funding includes stock market capitalization and bond market capitalization. The bond market is further broken down to private bond market and public bond market that provide funding for public finance through bond securities such as government bonds.

Figure1.4 Market funding versus bank funding in nine economies, 2017

Notes: computed by the author. Horizontal axis is in percentage points. For each country, the thick bar indicates total bank credit to GDP, and the thin stacked bar indicates market capitalization to GDP. Market capitalization includes stock market capitalizatio...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Contents in Brief

Table of Contents

List of figures

Preface

Acknowledgments

Acronyms

Part I Introduction

Part II The Microeconomics of Banking

Part III The Macroeconomics and Political Economy of Banking

Part IV The Economics of Banking Regulation

Part V Appendix

Bibliography

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Economics of Banking by Jin Cao in PDF and/or ePUB format, as well as other popular books in Economics & Financial Engineering. We have over 1.5 million books available in our catalogue for you to explore.