Real Estate Valuation: A Subjective Approach highlights the subjective valuation components of residential and commercial real estate, which can lead to a range of acceptable property value conclusions.

It discusses the causes of housing booms and goes in depth into the heterogeneity of commercial real estate property valuation via examples from owner-occupied, multifamily residential, hotel, office, retail, warehouse, condo conversion, and mortgage-backed security areas of real estate. Other topics explored include the role of machine learning and AI in real estate valuation, market participant value perceptions, and the challenge of time in the valuation process. The primary theoretical basis for the range of acceptable values and the subjectivity of property valuation focuses on the work of G.L.S. Shackle from the Austrian School of Economics.

This illuminating textbook is suitable for undergraduate and master's students of real estate finance, and will also be useful for practitioners in residential and commercial real estate.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Chapter 1 From Austrian value subjectivity to Shackle’s Possibility Curve

DOI: 10.4324/9781003083672-1

Chapter highlights

The range of values for real estate

The spectrum of valuation

Austrian value subjectivity: historical origins

Shackle’s Possibility Curve: original model and modern context

Investor choice example: land development

We are prisoners of the present who must choose in the present on the basis of our present knowledge, judgments, and assessments.

GLS Shackle

1.1 The range of values for real estate

It has been said that beauty lies in the eyes of the beholder. In no asset class is this better exhibited than in real estate. Sometimes people’s assessment of real estate value is based on empirical evidence, and at other times, this evidence is somewhat (or completely) clouded with emotional ties or feelings of nostalgia. Regardless of the method, real estate is an illiquid asset class. In other words, it takes quite a bit of time to sell a property as compared to other assets such as stocks and bonds, or even smaller things such as bologna sandwiches. One reason for this time difference is the legal determination of the ability of the seller to adequately convey the property to the buyer. Another reason is the length of time it takes for an appraiser to provide an official value of record for the transaction. While these time pressures indubitably exist, the purpose of this book is to explore why it takes so long for a buyer and seller to agree on a price.

Let’s return to bologna sandwiches for a moment. If you desire to purchase one of these at your local restaurant, there really is no price negotiation. Right there on the menu you can plainly see the price for bologna sandwiches, with the only real price variability consisting of side items and beverages. Thus, the seller lists their determination of the current market price and you can take it or leave it. Within the bologna sandwich spectrum, I am sure there could be higher priced luxury versions (with fancier bread for example) as well as lower priced more standard versions, but in each case, the price is stated and the buyer can take it or leave it. If no restaurant customers purchase a bologna sandwich on a given day, this may not mean that the price is excessive; however, if this situation persists, the price will inevitably come down. Maybe customers just don’t like bologna sandwiches anymore owing to perceived health risks, or maybe the price offered in the particular restaurant is just too high. “Jimmy makes a great bologna sandwich, but at that price I think I will just stay home and make it myself”. For this one restaurant in the bologna sandwich selling universe, the supply was too great relative to demand, so the price came down.

The concept of subjective price is related to the supply and demand charts exhibited in classical economics. Under the scenario just described, the surplus of bologna sandwiches led to the price decline. At some magical point, the quantity of the supply and the quantity of the demand meet, achieving equilibrium. While this represents convenient theory, the process by which equilibrium is achieved is rarely mentioned and often ignored. Equilibrium is so celebrated that you would think that once it is achieved that there would be some ceremony where the sandwich makers and the sandwich buyers come together in song, or at least come together with prepared speeches. The pathway to equilibrium for any asset price represents the period where there is disagreement among market participants as to the value for a stated asset.

Returning to real estate, given the length of time typically required for a buyer and seller to agree on a price (i.e., the time that the property is offered for sale on the open market), there is obviously a difference of opinion between the purchase price that a seller desires and what prospective buyers who decide not to pay this price believe is the appropriate amount. We have all seen the residential or commercial property that is initially offered at one price, but then after a few months when the seller is unsuccessful in finding a willing buyer at the offering price, the price is subsequently dropped. In fact, sometimes rather than a price drop, the property is taken off the market for a period of time, only to be offered for sale as a new listing at a reduced price soon thereafter. What is going on from a pricing standpoint during this period of time? Apparently the market process is not able to locate a buyer willing to pay the indicated price. The tacit assumption is that if demand exists for the subject property, would-be buyers are only interested in purchasing the property at a strike price lower than what is currently being offered. The implication of all of this is that there is a range of acceptable values for the subject property as determined by various market participants.

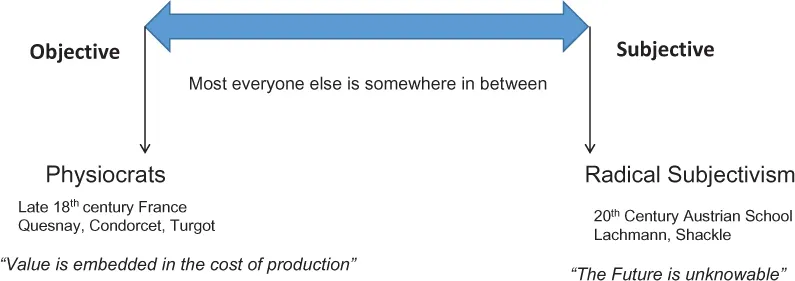

The range of values for real estate is highly influenced by the valuation method employed. The three most common forms of valuation for real estate are the sales approach, the cost approach, and the income approach. Each of these methodologies has a combination of objective and subjective value considerations. As shown in Exhibit 1.1, embedded in all valuation are subjective and objective components.

Exhibit1.1 Spectrum of Valuation.

1.2 The spectrum of valuation

The sales approach involves the use of objective, empirical data such as consummated sales of properties deemed similar to the subject property. These “comparable properties” form the basis for the asking price of the property being sold, as a rational market participant would not expect to pay more than other rational market participants have paid for a like or similar property. While this sounds almost entirely objective, the sales approach does have a significant level of subjectivity, especially as the comparable properties deviate in some form or fashion from the subject property being valued. As we will discuss more in Chapter 3, home sales have a perceived objectivity in valuation as long as there are recent sales of similar homes in the market. But what if the subject property consists of a brick structure with three bedrooms and two bathrooms, but that exact paradigm is not found in the comparable properties surveyed? There must be some mechanism to obtain an “apples to apples” comparison, whereby the historical comparable properties’ sales prices are increased or lowered based on whether the subject property is deemed inferior or superior in some component of value. The sales approach is the most common appraisal method for owner-occupied homes and owner-occupied commercial properties.

The cost approach has historically been viewed as the most objective form of value, as it consists of a determination of how much it would cost to reproduce the subject property should it be razed to the ground. The cost approach owes its origins to a group of economists in 18th-century France who were known as the physiocrats. They believed that the source of all wealth was in agriculture and that value is embedded in the cost of production. As alluded to in Exhibit 1.1, some famous members of this economic school were Francois Quesnay, Anne Robert Jacques Turgot, and Marie Jean de Caritat, Marquis de Condorcet. As a generalization, these gentlemen believed that value is embedded in the cost of production. In other words, a determination of value for a given object is ultimately related to how much it costs to produce. In the landmark “Tableau êconomique” of 1758, Quesnay developed the notion of economic equilibrium and the term laissez-faire (i.e., “allow to do” without government intervention) among other well-known ideas. In this book, the first circular diagram for how a national economy works was devised, and the groundwork for the cost approach was theorized. Today, the cost approach is utilized in newly constructed properties to determine the insurable value of a residential or commercial property and the effective age of a property which, in turn, is helpful for determining how long a lender might consider amortizing a loan secured with the subject property. Additionally, the current cost approach includes more subjective elements such as “entrepreneurial profit”, as a real estate developer would not be motivated to build a property and sell it for the cost of construction alone. Other subjective elements in the cost approach include the assumed cost of components (i.e., the cost of appliances in an apartment building) and the various adjustments to the subject property’s valuation based on differences in layout, size, and type of construction. Examples of the cost approach in the context of this book will be discussed in Chapter 3.

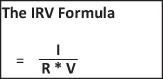

The income approach is utilized for commercial properties where the tenant is different from the owners of the property, and a lease has been negotiated whereby net income can be capitalized to estimate value. I have written on the income approach extensively (Goddard & Marcum 2012), so this book will discuss how the income approach fits into the subject of valuation subjectivity, a mark that it consistently achieves. Exhibit 1.2 illustrates the basic IRV formula which sits at the base of the income approach.

Exhibit1.2 IRV Formula.

The three basic components of the IRV formula are income, rate, and value. Income is traditionally viewed as net income, and the rate employed is known as a capitalization rate (a.k.a. “cap rate”). The capitalization rate takes the net income and converts it to a value. The equation can be written differently to solve for the element that is unknown:

Income = rate * value

Rate = income/value

Value = income/rate

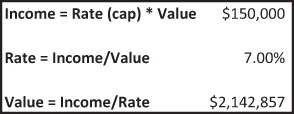

As baseball announcer Vin Scully used to say, “for those of you scoring at home”, if we assume a net income of $150,000 annually and a cap rate of 7.00%, you can back into a property value of $2,142,857. This exact looking value would typically be rounded to $2,150,000, or perhaps $2,200,000. Thus, subjectivity exists in even the simplest of calculations! Exhibit 1.3 allows the opportunity for the reader to explore their inner Vin Scully and “score from home”. Just take the two knowns and back into the answer for each of the three IRV components. This is where Vin meets IRV.

Exhibit1.3 Various IRV Iterations.

Appraisal theory suggests that each of the three valuation approaches should wind up in about the same place. While this is a great concept, we often do not live in an M.C. Escher world of symmetry. The assumptions contained in each of these approaches can be massaged to ordain a certain unison result that makes the range of values appear moot. In the United States, an appraisal by an independent third party is required for most loans secured by real estate. A popular definition for an appraisal is an opinion of value, of which apparently there could be many opinions if not for supremacy of one opinion by government fiat. While the “independent third party” has a nice ring to it, one of the first questions that the appraiser of record asks when taking on an assignment is what the purchase price is that has (finally) been negotiated between a buyer and seller. This reminds me of a Kierkegaard line, “in case he who should act was to judge himself according to the result, he would never get to the point of beginning”. What would happen if the independent third party approached the assignment like the characters in an Agatha Christie novel, and didn’t lead with the answer required at the outset? Taken to its extreme, market chaos could ensue, whereby appraisers arrive at very different value conclusions than two market participants (a buyer and a seller). Shown in a different light, if the third-party evaluation was not required for the majority of purchases requiring a loan from a financial institution, the sales contract between two market participants would be all that was required. If that was the case, neither a book like this nor the real estate appraisal industry would be necessary. So let’s not wish that situation into existence!

As will be elucidated in the chapters that follow, each of these three elements has a subjective component that contributes to possibilities of different opinions of market value for a given property. In order to calculate net income, we must first start with the gross potential income of the subject property. What if a space is vacant? Do we include this space in our calculation? Do we simply value the property based on its specific performance, or must we also consider how the property’s rents, vacancies, and expenses compare to other properties in the market? When deriving a cap rate, should we simply use the IRV formula, or should we compare what other investors have received when purchasing similar properties? Finally, how does the value per square foot compare with similar consummated sales in the recent past? All of these are good questions which we will explore in depth later, but for now, let us recognize the subjectivity which enters into the valuation model when these questions are considered.

The one element of Exhibit 1.1 not yet explored is ...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Dedication Page

Table of Contents

About the Author

Preface

1 From Austrian value subjectivity to Shackle’s Possibility Curve

2 The role of machine learning and artificial intelligence in real estate valuation

3 Overview and pitfalls of home valuation subjectivity

4 Subjectivity of commercial real estate valuation

5 Market participant value perceptions

6 Subjectivity of cap rates, discount rates, and debt yields

7 Subjectivity in hotel property valuation

8 Discounted sellout and subjectivity

9 Mortgage-backed securities and subjectivity

10 The provocation of time

Glossary

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Real Estate Valuation by G. Jason Goddard in PDF and/or ePUB format, as well as other popular books in Business & Construction Industry. We have over 1.5 million books available in our catalogue for you to explore.