In this second edition of Investing in Movies, industry veteran Joseph N. Cohen provides investors and producers with an analytical framework to assess the opportunities and pitfalls of film investments.

The book traces macroeconomic trends and the globalization of the business, including the rise of streamers, as well as the impact these have on potential returns. It offers a broad range of guidelines on how to source interesting projects and advice on what kinds of projects to avoid, as well as numerous ways to maximize risk-adjusted returns. While focusing primarily on investments in independent films, Cohen also provides valuable insights into the studio and independent slate deals that have been marketed to the institutional investment community. As well, this new edition has been updated to fully optimize the current film industry climate including brand new chapters on the Chinese film market, new media/streaming services, and the effects of COVID-19 on the global film market.

Written in a detailed and approachable manner, this book is essential for students and aspiring professionals looking to gain an insider perspective against the minefield of film investing.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Summary—Investors in any business need accurate information in order to assess risk and project rewards. The movie business, however, does not provide the full panoply of publicly available information to make such judgments, so prospective investors have to seek other sources of information to augment their analysis. In particular, this chapter distinguishes between “budget” and “actual film cost” and points out the lack of transparency with regard to domestic and international distribution and marketing costs and the difficulty of determining accurate correlations between domestic box office and ancillary revenue streams, such as home video and free and pay television. The first challenge that prospective investors face, assuming they are looking at financing a single picture or a slate of studio films, is how budgetary discipline will be exercised. The chapter addresses a number of considerations that impact budgetary discipline. Finally, the chapter reviews historical expectations with regard to investing in a portfolio of studio films and why expectations and actual results did not always match.

Invariably, whenever I tell someone that I advise very rich individuals with respect to their film and television investments, that person is skeptical about my clients’ intentions, “They really don’t expect to make money, do they?” For some reason, it’s really about hobnobbing with the stars, or getting their girlfriends (or boyfriends) in the movies, or impressing their cronies. I won’t deny that I have come across investors who have acted out of one or more of these questionable motives. But most of these “fringe” investors typically never show the color of their money. They make lots of promises, but rarely close.

My clients are self-made multimillionaires or billionaires, for the most part. Some are scions of inherited wealth, but the scions of inherited wealth are usually surrounded by legions of legal and investment advisers who do their darnedest to keep their legatees out of the clutches of fast-talking producers. These fiduciaries are basically risk adverse. They aren’t knighted for generating above-average investment returns, but they face the danger of being axed if they invest in areas that are perceived to be exceptionally high risk—and the movie business certainly has the reputation of being not much better than the slot machines in Vegas.

The self-made rich, however, are used to taking risks. That is why they have as much money as they do. But they tend to be extremely analytical in their approach to risk management. It’s all a matter of probabilities, and the fact that they have opted to play in this space is indicative of their belief that rational investment strategies are possible in the movie business. The bets are too large to simply act out of whimsy.

That is not to say that their initial incursions into the motion picture industry were not somewhat capricious. Several major players I am aware of, including several of my clients, were, in fact, the “victims” of fast-talking producers. You have to realize that producers are some of the most persuasive salesmen around. They have to be, because they are dependent on their gift of gab for hooking studios or wealthy individuals to pony up significant sums of money on the basis of a “pitch,” a script or a package (director and stars). In the case of wealthy individuals, most instances of being taken to the cleaners did not involve major losses, because their basic reticence about the bona fides of film investment served as a natural drag to the contagious enthusiasm exhibited by the producers. In general, smart investors can be fleeced only once, maybe twice, and then they either leave the field or decide that they want to learn the rules of the game and apply the same set of rigorous investment strategies that they have employed in their primary businesses. The self-made rich do not like to be made fools of. Hence, their stubborn insistence on mastering the macro- and microeconomic facts that underlie the motion picture business. Once this intellectual mastery has occurred, they can proceed to explore rigorous business strategies, culled from the experiences of the major studios and successful independent producers. Now they are in the world that business consultants are familiar with, throwing around concepts like market share, leverage, risk transfer, niche strategies, co-financings, return on investment (ROI) and tax shelter. They have gone beyond the perception of the business as a veritable crap shoot.

Hollywood soaks up information, just like Wall Street, and while the quantum of information transmitted in Hollywood contains a far higher percentage of industry gossip than Wall Street, the information flow is also characterized by virtually instantaneous transmission. What books are available to be optioned, what films have fallen apart (so the director and actors are now available), what executives are about to be sacked (so do not waste your time pitching new projects to them)—all of that represents insider knowledge that is not generally available to the public at large. What is readily available to the general public is the latest box office data—at least the top ten grossing films for the weekend. Those box office numbers by themselves are not sufficient to determine the profitability of a film, or even whether the film is profitable at all. Arguably, it is a fact that most of the key parameters that determine a film’s success are hidden below the water line, much like an iceberg, which discourages serious investors from dabbling in the movie business.

The first impediment to investing in the movie business, therefore, is lack of concrete public information. This is particularly frustrating for Wall Street types who, in the Internet Age, are used to being able to extract any item of quantitative data they desire at the push of a button. If anything, stock and bond market analysis may be oversaturated with data, and one of the first tasks of analysts these days is to sift through the data to learn what they should take seriously and what they should ignore. The film industry is nowhere near as transparent.

Let me try to be more precise. No totally reliable data is published regarding film budgets. Occasionally, you will see estimates in the press, but these are only estimates. No sources for these estimates are given, and I have seen vast discrepancies among estimates on the same film. There are many reasons for the lack of published data. Most important, there is no incentive for the producers or studios to reveal their hand. By doing so, they give away valuable information to competitors as well as to the creative participants (actors, directors and writers) who are profit participants in the film. Like sports franchise owners, it is in the studios’ interest to plead poverty. Since all the major studios are subsidiaries of large public conglomerates whose annual 10Ks are about as long as PhD theses, there is no way you can glean the profitability of individual films from SEC filings. The film operations are buried within larger divisions, which frequently include television programming, broadcasting, theme parks, video distribution and so on. Studio bragging rights are determined primarily by box office share, and generally only domestic box office share (“domestic” in the quaint parlance of the industry means both the United States and Canada). There is no definitive way to measure individual studios’ profit margins. Even box office share is not weighted for the number of releases in the studio’s release calendar for that year.

In general, studios tend to understate budgets rather than hype them. There is an embarrassment factor at work here. Let’s face it—in an era of excess, where the mega-rich are buying $100 million homes and $10,000 pocketbooks (conspicuous consumption has returned after the economy has been boosted by continuous liquidity injections by the Federal Reserve)—it is a little obscene to make a movie that is more expensive than the GNP of half the countries in the world. In addition, the industry has a predilection for Schadenfreude, which is a German expression for taking pleasure in other people’s misfortune. Hollywood practically oozes Schadenfreude—not because its participants are more misanthropic than most, but because there is an abiding superstition that Hollywood is a zero-sum game. If you succeed, it means that there is less available success out there for me. Perhaps that principle makes sense when applied to competing films on the same weekend, but it clearly is wrongheaded when applied on a macro basis. If you make a baseball movie that works, contrary to established opinion, that will increase the odds that my baseball movie may also get made (as long as mine isn’t the fifth film in the cycle, and the three previously produced baseball films didn’t tank). But, as we shall see later, given that there are few variables (I will suggest two, somewhat tongue in cheek) that show consistent positive correlations with box office success, repeating successful genres or themes is no guaranty of future success. Sequels to highly successful films, the so-called franchises, are a different matter, and there is definitely a reasonable positive correlation there. In fact, there used to be a rule of thumb (another one of those rules of thumb that are more industry wives’ tales than empirically grounded truths) that a sequel should do roughly 75% of the domestic box office achieved by its predecessor. Many sequels over the past 5 years have outperformed their predecessors, but studio executives are concerned that more recent experience has been much less positive.

The very notion of “budget” is a shifty concept. Sometimes it refers to the projected cost of the film going in, and sometimes it refers to the actual cost of production, as determined when the film is delivered (“delivery” is a technical term that refers to the fact that all the elements needed to exploit the film have been completed and made available to the relevant distributors). As initially prepared, budgets represent best guesses regarding the ultimate cost of the film, prepared on a line-item basis and then tallied up. The responsibility for preparing such budgets falls on the so-called line producer and his staff. The line producer is the person who is the chief operating officer of the film. He or she is generally not the senior producer on the project. The senior producer is the person who typically acquired the rights to the project, developed the screenplay, hired the director and the key cast, brought in the studio to distribute the film and secured the necessary financing. In the old days, the senior producer function rested with one individual. Now that role has often been fragmented particularly with respect to putting together the financing and arranging distribution. Those tasks fall on individuals who frequently take “executive producer” rather than “producer” credit. The line producer answers to the producer, who, depending on the power and oversight of the financiers and distributors (who are often one and the same), may be the autocrat of the project or the factotum of the money guys, who are unaffectionately known as “suits.” Nevertheless, only the credited producers on a film get to ascend the podium to receive the Oscar for Best Picture.

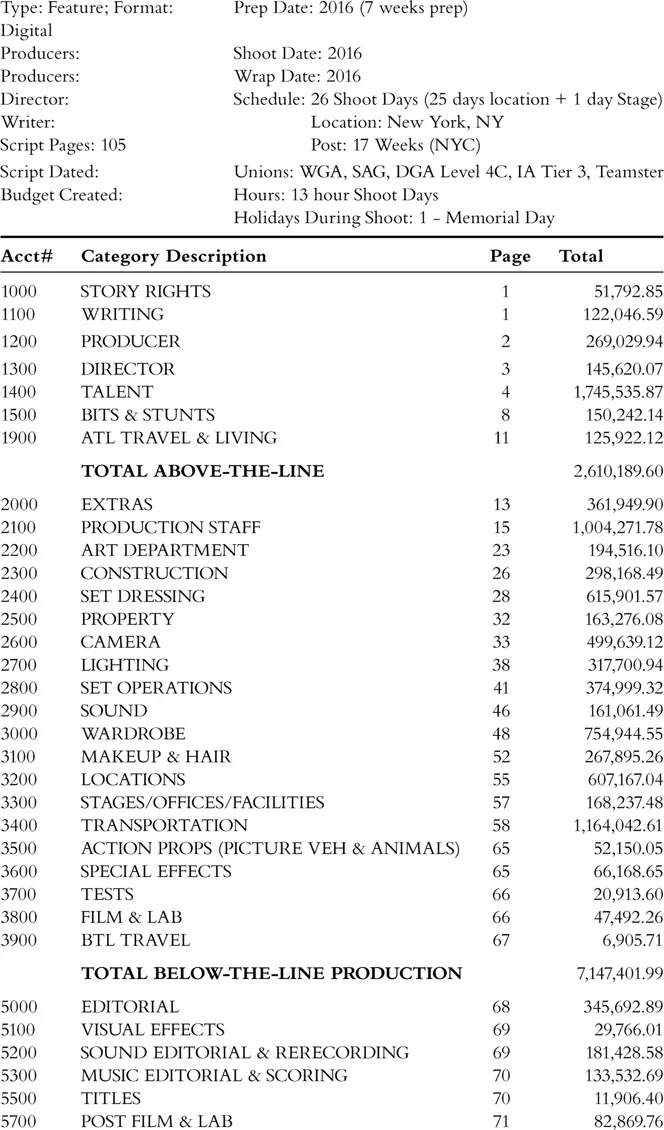

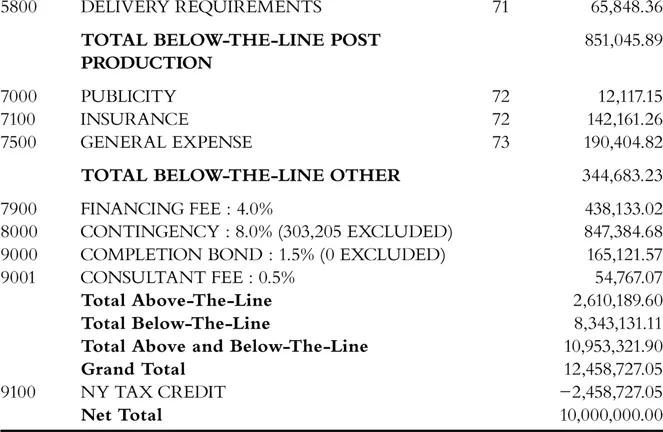

In Figure 1.1 you will find a sample “top sheet” for a film shot in New York that my company was an advisor on. The top sheet represents the first two pages of a standard film budget and includes an overview of all the major costs associated with the film.

If you examine a complete budget, you will be reviewing 50–80 pages of numbers broken down into categories, like Art Department and Visual Effects, with a summary statement, the top sheet. The top sheet is broken down into two sections: above-the-line and below-the-line. Above-the-line represents the cost of the rights (including development expenditure related to the screenplay), actors, director and producing group, while below-the-line represents the actual production costs, including crew, construction, locations, transportation, visual effects and film stock, as well as post-production expenditure, including editing, music and so on.

FIGURE1.1 Sample Film Budget.

Before these numbers can be calculated, the line producer has to “break down” the screenplay and figure out how many days it will realistically take to capture on film all of the action and dialogue contained in the screenplay. Typically, the line producer is given fairly free rein in coming up with this breakdown. Of course, this is done in the context of what kind of production the given project is likely to represent. If it is a big studio production with major stars and a prominent director, the line producer will approach the budgeting process with a certain bias, while if it is an independent film that clearly has limited capital available, he or she will approach the job with a radically different frame of mind.

Enter the director. Frequently, the line producer has been selected by the director or is even the director’s own man (or woman). That is, many directors typically work with the same line producer time after time. There are advantages to the production in this cozy relationship. Given that the two are used to working together, there is a greater probability that the shoot will go more smoothly. The line producer knows the strengths and weaknesses of the director and is better able to support him or her. But this symbiosis is also fraught with danger, particularly as far as the “suits” are concerned. When the line producer is effectively an arm of the director, when he or she clearly knows where his bread is buttered in the sense that he or she will continue to work with the director in the future but may never see the financiers on this project again, there is tremendous risk that there will be less than total financial conscientiousness displayed in the construction of the budget and less than total financial discipline exercised during the making of the film.

One must remember that some directors, not all, are first and foremost artists. The French refer to these directors as auteurs. That does not mean that such directors do not exhibit financial discipline, but it does mean that their primary responsibility is to their artistic vision. If that vision requires reshooting scenes or expanding the scope of the production design or low-balling the true budget to entice the financiers to commit to the project, even the most ethical of directors will be sorely tempted—and not every director starts out with the highest ethical standards. There are some directors who are marvelous in terms of being able to create cinematic masterpieces whom I would never bankroll because they cannot be controlled. Some producers may con themselves into believing that they can control any director through sheer force of will, but for the most part, they are kidding themselves. On the set the director is basically king. Yes, you can fire him (subject to what I will discuss later as an “essential elements” clause), but then you really risk the film going totally out of control, both financially and creatively.

Lack of budgetary discipline cannot always be laid at the foot of the director. Studios are often just as much to blame. Many studio executives who have responsibility for overseeing productions do not have a lot of physical production experience. After all, it’s not their money, and it’s not necessarily in their interest to keep the director on too tight a leash. Like the federal government, studios frequently attempt to solve problems by throwing more money at them. This is particularly true on the big action and special effects films, where there is a great deal of pressure to come up with state-of-the-art action and special effects. Granted, if you skimp on these sequences, you jeopardize the commercial prospects of the film—but all too often the studios acquiesce to a shooting schedule on a straightforward production that is far too accommodating. Clint Eastwood is not only a great director, but he is also the opposite of prodigal when it comes to the pace of his direction. As an example, Clint took only 36 days to shoot Million Dollar Baby. This can be compared with the 70-day-plus schedules that are not uncommon today even on studio dramas and comedies.

Let’s confess to a not-well-kept secret that is relevant here: more and more, the studios are turning to younger, less-experienced directors who are considered hipper and more attuned to the youth audiences that are the primary demographics for a large percentage of the films the studios are making today. Many of these directors have honed their skills on commercials and music videos that are incredibly good-looking, but short on plot and characterization. To a significant extent, these inexperienced feature directors are learning on the job, which often entails longer production schedules.

Independently financed productions, because of tighter capital constraints, tend to be much more disciplined when it comes to budgets. But frequently this translates to a less-polished finished product. Just because an independent producer says that he can shoot a given film in 5 weeks on a budget of X doesn’t mean that the film will be roughly comparable to a studio version shot in 10 weeks on a budget of 2X. While capital constraints are incredibly important, they cannot succeed in placing a square peg in a round hole. While I have complained about excesses with respect to the number of days utilized for principal photography, there is the flip side of the coin that places a practical floor on the least number of shooting days that can accommodate a given script. There are only so many setups (individual scenes from a script breakdown point of view) that can be accomplished in a given day, irrespective of the number of takes that are required. Independent producers should always keep in mind the mantra of independent filmmaking—good, fast and cheap.

Enter the completion guarantor. The completion guarantor is the entity that covers budgetary overages and guarantees that the film will be delivered by a specified date. Virtually all independent films, apart from ones with micro-budgets, as well as a growing number of studio films (although the vast majority still self-bond) utilize completion guarantors. To the extent a bank is involved in providing any portion of the financing, it is necessary that the film be “bonded” by a reputable completion guarantor. Similar requirements are often placed on the film by equity investors.

There is a very good reason that banks do, and equity investors should, require such protection. With respect to project finance lending (that is, stand-alone single-picture financing), the banks are lending primarily against bankable contracts from distributors who commit to paying an advance upon delivery of the film. Entertainment banks may give some credit for the estimated value of unsold rights, the so-called gap lending, but in either case if the film is abandoned or if the film goes over budget and there is no source to provide the required additional capital, the value of those distributor advances is nil. In addition, distribution contracts stipulate outside delivery dates, and if for whatever reason the producer fails to make timely delivery, the distributor is no longer obligated to honor the contractual advance. Completion guarantors take on the burden of ensuring that such events do not happen, and, if they occur, the completion guarantors ensure that the named beneficiaries on the bond are made whole. In the case of an abandoned picture, for example, the completion guarantor will reimburse the financiers for any monies expended to date.

There is obviously a cost associated with utilizing a completion bond company. First, the bond company will insist that a contingency be added to the budget. This contingency functions much like the deductible on your homeowner’s policy. The contingency is typically 10% of the budget, possibly with certain exclusions, (but may be more in the case of complicated special effects films), and it must be fully expended to cover any budgetary overages before the completion guarantor kicks in. Second, the completion guarantor charges a fee, which is typically around 2–3% of the budget (more precisely, of the defined budget, which for completion bond purposes may exclude certain expe...

Table of contents

Cover

Half Title Page

Title Page

Copyright Page

Dedication

Table of Contents

Acknowledgments

Introduction

1 Pros and Cons of Motion Picture Investment

2 Macroeconomic Trends and Studio Co-Financing

3 Tax and Other “Soft Money” Benefits and Limited Partnerships

4 Welcome to the World of Independents

5 The Evolution of Revenue Streams

6 COVID and Post-COVID

7 The Rise of the Streamers

8 Cast of Characters

9 Globalization of the Business

10 How to Have Fun and Not Lose Your Shirt

11 Managing Risk

12 Working the Banks and Non-Bank Lenders

13 How to Beat the Odds: Niche Strategies

14 Evaluating Projects and How to Pitch Them

15 Where You Should Be in the Food Chain: Distribution versus Production

16 The Sinkhole of Development

17 Exit Strategies: The Value of Film Libraries

18 New Directions: The Digital World

19 Art versus Commerce

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Investing in Movies by Joseph N. Cohen in PDF and/or ePUB format, as well as other popular books in Business & Film & Video. We have over 1.5 million books available in our catalogue for you to explore.