![]()

Part I

BUBBLES AND THE ECONOMY

![]()

1

AN ANATOMY OF BUBBLES

The valuation of assets plays a crucial role in the market economy. A rise in the price of one asset relative to another encourages resources to flow in that direction, whether we are talking about technology shares, houses, or tulip bulbs. But private markets also seem periodically to lose themselves in wild speculation and then equally wild pessimism: bubbles followed by busts.

The classic profile of a bubble involves several stages.1 In the beginning there is a so-called displacement, some outside event that changes the investment landscape and seems to open up a new opportunity. The displacement can be the end of a war, a new technology (canals, railways, the internet), or perhaps a large fall in interest rates. The nature of the displacement is the biggest source of variation between bubbles, and perhaps this is one of the causes of the problem. We are unlikely to see a second internet bubble, but who knows what new technology in the future could generate similar excitement?

If this displacement effect is strong enough, it generates an economic boom as investment goes into the new area. Often banks play a major role in fueling the bubble by accommodating a rapid expansion in credit. But history suggests that even if existing banks are not major participants, other sources of credit and finance come to the fore, including new banks, other types of finance companies, foreign banks, personal credit, and so on. New investment floods into the booming sector, pushing up prices and opening up still more profit opportunities.

At some stage the bubble reaches a phase variously called euphoria or mania, where speculation mounts on top of genuine investment and expectations for potential returns reach wild heights. Strong market performance is extrapolated endlessly forward and any consideration of fundamental valuation criteria is swept aside. More and more people are drawn into speculation, in the hope of making quick money. It is at this point that taxi drivers talk about the market; near the final peak everybody’s mother wants to buy too! Generally you find numerous people warning of a bubble, sometimes politicians and bankers, at other times newspaper writers. But their first warnings are usually too early and they often become discredited.

Eventually the market rise slows as some people take profits and fewer people are willing to come in. Sometimes there is a period of eerie calm, before a new event precipitates a decline in prices. This event can be a new external shock such as a war, or it may be a rise in interest rates or a slowdown in the economy as new investments have come on stream and it has become evident that there is overcapacity. The trigger does not necessarily have to be a large event; sometimes it is simply “the straw that breaks the camel’s back.”

The next stage is called “revulsion”: prices fall, financial distress rises, bankruptcies mount, and banks pull back on lending. The economy is affected by the fall in new investment and the rise in uncertainty so that perfectly good projects now fail, adding to the distress. General business confidence evaporates and everybody wants to “wait and see” before committing to new hiring or fresh investments. Consumers may also hold back on large purchases such as cars or houses, concerned that their jobs are at risk as well as their investments.

There may also be a “panic” phase, when prices fall extremely rapidly as people try to sell before everyone else and there are hardly any buyers. Liquidity may dry up. Prices fall precipitately, in a kind of reverse speculation. Eventually, either they fall so far that people decide they are now cheap, or the authorities close the market for a while hoping for the panic to subside, or use some kind of “lender of last resort” activity to restore confidence. However, it is rare to escape this phase without at least a serious economic slowdown and usually a recession.

IDENTIFYING BUBBLES

The description above is the typical pattern of a bubble in outline. In my view, it is comparatively easy to recognize a bubble when it is fully or nearly fully inflated, though some people dispute even this and argue that a bubble is only definitely confirmed afterwards, when it has burst. For an investor, recognizing a bubble is crucial if potentially large losses are to be avoided. From a public policy perspective, in terms of managing the economy it would be useful to identify a bubble or potential bubble early, before it reaches extreme valuations.

Table 1.1 presents a checklist of typical elements that have been observed in bubbles from the South Sea to the internet. Most of these are very obvious at the height of a bubble, though in the earlier stages it is more a matter of judgment.

Table 1.1

Checklist: Typical characteristics of a bubble

High expectations for continuing rapid rises

Overvaluation compared to historical averages

Overvaluation compared to reasonable levels (see

Chapter 10)

Several years into an economic upswing

Some underlying reason or reasons for higher prices

A new element, e.g., technology for stocks or immigration for housing

Subjective “paradigm shift”

New entrepreneurs in the area

Considerable popular and media interest

New lenders or lending policies

Consumer price inflation often subdued (so central banks relaxed)

Falling household savings rate

Source:Author, partly based on “Bubble trouble,” HSBC Economics and Investment Strategy, July 1999.

RAPIDLY RISING PRICES

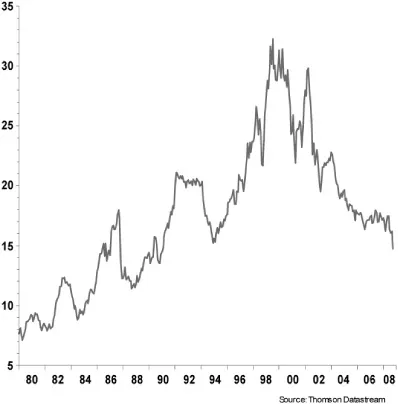

First of all, a bubble obviously involves a period of rapidly rising prices. However, a strong rise in prices in itself does not necessarily imply a bubble, because prices may start from undervalued levels. So we should only start to suspect a bubble if valuations have moved well above historical averages, on indicators such as the price-earnings ratio for stocks or the house price-earnings ratio for housing. The extent of this over-valuation probably gives us the best clue as to the exact probability of a bubble. For example, the US stock bubble in the 1990s took the price-earnings ratio on operating earnings (which excludes one-off factors) to over 30 times, well above the long-term average of about 14-16 times (see Chart 1.1)2

Chart 1.1

US S&P 500 price–earnings ratio

OVERVALUATION

The issue of valuation is contentious, with many people arguing that we can never be sure that a market is really overvalued. I disagree and believe that we can identify ranges for valuations that are more or less reasonable, such that if a market goes above them, we can say that there is at least a high probability that it is a bubble. Further evidence can then be sought in other characteristics.

ECONOMIC UPSWING

Typically bubbles develop after several years of solid, encouraging economic growth and rising confidence. The traumas of past recessions and bubble crises (at least in the same market) have faded away. For example, the US 1990s stock market bubble came in the last three years of a nine-year economic expansion and following fifteen years of a relatively strong stock market. And the Asian property and stock market bubbles that burst in 1997-8 came after over a decade of breakneck expansion, which had become known as the Asian Miracle.

The US housing bubble was a little different in that it started to take off soon after the economy emerged from recession. However, it did come more than 10 years after the last (much smaller) housing bubble burst in the early 1990s and was partly the result of the low interest rates put in place to fight the effects of the bursting of the stock bubble. Meanwhile, the biggest housing bubbles in the 2000s have been in Australia, the UK, and Spain, three of only a handful of major countries that avoided a recession during 2000-3.

NEW ELEMENT

As noted earlier, another typical characteristic of a bubble is a new development or change in the economy that can reasonably justify higher prices. In the 1990s it was computers and networking technology and, more broadly, the apparent sharp acceleration in US productivity growth that led to much talk of a “new economy.” In the 1980s in Japan it was the perception that the Japanese economic model, with all its panoply of “just-in-time” inventory management, worker involvement, and “total quality control,” was going to dominate the world. The housing bubbles have been linked to increased immigration and lower interest rates.

PARADIGM SHIFT

There is often the perception of a “paradigm shift” and this is usually argued energetically by some leading opinion formers. We shall see later that people seem to have an innate tendency to believe (or want to believe) that current events are entirely different from any episodes in the past. This is a natural characteristic of younger people especially and certainly the 1990s internet boom was very much led by young people. But of course, some people have a vested interest in arguing that “it is different this time”—especially brokers, fund managers, and real estate agents.

I do not for one moment want to sound like someone who has seen it all before and believes that nothing is new under the sun. Economic performance and market behavior do change over time and periods of strong performance and weak performance can persist for a long time, often decades or more. Nevertheless, it is dangerous to extrapolate this into justifying very high valuations, at least without serious caveats.

Even if higher valuations in a market can be justified by fundamental changes in performance, we should expect this to be a one-off move, not a shift to permanently faster price increases. For example, faster growth of profits would justify higher valuations, but once valuations have moved a step higher, stock price gains should then slow down to the rate of growth of profits. It is unrealistic to expect valuation multiples to expand further. The same goes for house prices. If a higher house price-earnings ratio really is justified now, as many people argue, once the step higher has been made house price growth should return to the growth rate of earnings.

The US 1990s experience is interesting in this regard. The acceleration in productivity growth in the 1990s, part of the paradigm shift that accompanied the bubble, has been confirmed. US productivity growth since 2000—that is, after the bubble-has averaged 4 percent a year, higher than in previous decades. Similarly, the new technologies continue to permeate the economy in ways that many of the new economy enthusiasts predicted. But during the bubble a crucial point was forgotten: Faster productivity growth does not mean higher profitability in the long run. At first it brings higher profits, but this then brings more investment, more competition, and, eventually, lower prices so that the gains flow through to increased real incomes. Profits fall back to normal levels because in a market economy companies cannot hold onto them in the long run.

NEW INVESTORS AND ENTREPRENEURS

Returning to the checklist, a regular feature of bubbles is that new investors are drawn in, people who had not invested before. They are persuaded by the bulls’ arguments and also by the continuing rise in the market. Subprime mortgage borrowers, usually people who had rented previously, are a good example. Often new investors are assisted by the emergence of new entrepreneurs, for example those offering new investment vehicles, like the internet offerings in the late 1990s or the buy-to-let funds in Britain and Australia in recent years.3

POPULAR AND MEDIA INTEREST

Popular interest in the market becomes intense and this is reflected in greatly increased media coverage. Some stories emphasize the “wow” factor, as big rises in markets make people rich overnight. During stock bubbles, media stories may be tinged with envy for the lucky few, or even hostility toward “speculators.” In the case of housing markets, where often a majority of readers will be gainers, the emotional hook may be glee at the good news. A subtext may be that the reader too can get rich and some coverage will put the emphasis on how to join the party, for example providing information on stock funds or on mort-gages and property investment.

Another type of media story will focus on the risk that the market is in a bubble, warning of trouble and usually critical of speculators and, sometimes, of the authorities for allowing it. There are nearly always some commentators who forecast the demise of the bubble. For example, in the late 1990s The Economist and the Financial Times regularly returned to the bubble theme in US stocks. When the bubble burst they were justifiably pleased with themselves, although too polite to gloat. In the 2000s they turned their attention to warning about housing bubbles.

MAJOR RISE IN LENDING

Typically bubbles also involve a significant rise in lending by banks or other lenders. Sometimes this reflects regulatory or structural changes in lending practices and often it involves new entrants to the market. The US housing bubble is a classic example, with the explosion of subprime and Alt-A lending and the emergence of complex structured products like CDOs (collaterized debt obligations). Debt expands and the household savings rate falls. Behind all this is often what I would characterize as a relaxed monetary policy. Sometimes this is evident from a rapid rise in money growth. Probably more important, though, is the rate of credit growth; that is, the increase in debt (related to but not identical to the rate of money growth). Sometimes too it can be seen in the level of real interest rates in the economy, which may look unusually low.

STRONG EXCHANGE RATE

A final characteristic of most bubbles is a strong exchange rate or, if the currency is fixed, an inflow of resources. During the bubble, money flows into the country, either attracted by the booming asset or drawn in by the strength of the accompanying economic boom. The strong currency then leads to trade and current account deficits. Indeed, that is the “purpose” in a sense, so that there can be a net capital inflow, by definition equal to the current account deficit.

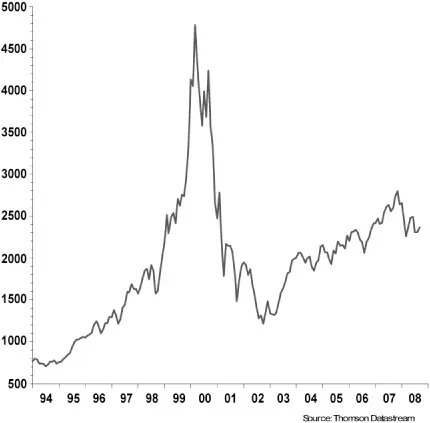

Not every item on the checklist is always present in every bubble. Ultimately, deciding whether a particular market boom is really a bubble is a matter of judgment, based on the number of characteristics present and how extreme they have become. If we think back to the internet bubble of the late 1990s, it should have been clear to all at the end of 1999 and the beginning of 2000 that this was a bubble. But by then the bubble was nearing the peak, with the US NASDAQ index rising from about 2,800 at the beginning of October 1999 to its peak of just over 5,000 six months later. It dropped back through the 2,800 level in December 2000 and went to a low of about 1,200 in 2002, the same level as 1996; see Chart 1.2. Ideally we would have identified a high degree of bubble risk as early as the middle of 1998 and some degree of risk also in 1997.4

Chart 1.2

The NASDAQ bubble

BUBBLES AND CONSUMER SPENDING

People respond to rising asset prices through so-called wealth effects. Small movements in asset prices may have little effect, but if the rise in wealth is large enough then, after a while, some people change their behavior. If the stock market has soared, perhaps they cancel their regular savings plan and use the money to go out to dinner more often, boring their friends with their skill in picking stocks. Others may take some profits and use the proceeds to buy a new car or a boat. If house prices rise fast they may increase their mortgage to spend money on a new kitchen or a home extension.

Some might say that people are foolish and shortsighted if they immediately spend gains. But many people have a target level of wealth and, if asset price inflation enables them to reach it earlier than they expected, why not spend more? After all, for most people the purpose of acquiring assets is for spending at some point. Of course, if the increase in prices is temporary and later reverses, they will be in for a rude awakening. There is also a danger that, after a period of price gains, they start to expect continuing gains at the same pace and adjust their spending further upward.

The evidence suggests that most people do not immediately spend gains but in fact respond only gradually. Possibly they are slow to realize that they are better off. Or perhaps they take a cautious approach to higher asset prices and only spend the gains when they believe that they are permanent. There is a potential trap there, though. The judgment as to whether or not higher asset prices are permanent tends to be based more on whether prices hold up for a while rather than whether valuations make sense. But as a bubble inflates, prices often exceed sensible valuations for an extended period and people start to see those high levels as normal.

Another common response to higher asset prices is to increase borrowing to finance higher spending. In the US it is relatively easy for people to borrow against stocks, even with only modest stock portfolios. In other countries often only those with a large portfolio can directly borrow against stocks, though there are other ways to...