The playing field for business has changed significantly in recent decades. The pace of change is accelerating, driven by increased technological progress and shrinking business lifespans. Economic and political uncertainty has risen dramatically and is likely to remain at elevated levels. Industry boundaries are blurring, increasing the potential paths to competitive disruption.

Strategy is not dead—in fact, as the gap between winners and losers within industries continues to grow, it is more important than ever. However, the playbook needs to be reinvented for today's business environment. Classical sources of competitive advantage, such as scale and differentiation, have not gone away, but they have been complemented by new dimensions of competition.

This book discusses the new role of strategy in a dynamic, unpredictable context. Part 1 of this book revisits classical strategy frameworks and what changes should be made to apply them to the modern era. Part 2 discusses new strategic capabilities companies need today, such as adapting to uncertain environments and shaping new or disrupted ones. Part 3 examines the expanding boundaries of strategy, including new competitive imperatives as well as the wider range of timescales on which businesses must now operate.

Drawing on the work of the BCG Henderson Institute and its fellows and ambassadors over several years, Dynamic Strategy will help business professionals as well as academics and students with an interest in strategy understand the new competitive challenges that businesses face and develop a playbook to address them.

Events around the book

Link to a De Gruyter Online Event in which Martin Reeves, Chairman of the BCG Henderson Institute, talks about successful business strategies in turbulent times: https://youtu.be/84YE4DBdQpo

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

In “The Rule of Three and Four,” written in 1976, Bruce Henderson put forth an intriguing hypothesis about the evolution of industry structure and leadership. He posited that a “stable, competitive” industry will never have more than three significant competitors. Moreover, that industry structure will find equilibrium when the market shares of the three companies reach a ratio of approximately 4:2:1.

Henderson noted that his observation had yet to be validated by rigorous analysis. But it did seem to map closely with the then-current structures of a wide range of industries, from automobiles to soft drinks. He believed that even if the hypothesis were only approximately true, it would have significant implications for businesses.

Fast-forward to the modern day. Has the rule of three and four held? If so, to what degree? Does it merit the attention of today’s decision makers? Our analysis yielded compelling findings.

Testing the Rule of Three and Four

To test Henderson’s theory, the BCG Strategy Institute (the predecessor of the BCG Henderson Institute), working in collaboration with academics from Chapman, Claremont, and Rutgers universities, studied industry data from more than 10,000 companies dating back to 1975.1 This analysis allowed us to confirm that Henderson’s hypothesis was indeed valid when he conceived it: it accurately described the market share structures current at the time, and trends in a wide range of industries. We can also confirm that the rule of three and four has remained a predictor of the evolution of industry structures in “stable, competitive” industries over the decades, with the caveat that many industries have experienced a departure from such stable conditions.

To facilitate our analysis, we divided companies into two categories: those with market shares of more than 10 percent (“generalists”) and those with shares of 10 percent or less. The prevalence of industries with no more than three generalists (the “three” part of Henderson’s rule) was striking. From 1976 through 2009, industries with one, two, or three generalists ranged from 72 percent to 85 percent and averaged 78 percent. The most common industry structure throughout the period was the three-generalist configuration, which prevailed in 13 of those 34 years and was the second-most common in 20 out of 34 years.

Industries with three-generalist structures have also proven the most profitable for industry participants, with an average return on assets a full 2.5 percentage points higher than in industries with four, five, or six generalists. Additionally, three- and two-generalist configurations appear to have the greatest stability and to act as the strongest “basins of attraction” – that is, more companies gravitate toward these structures every year than toward any other (Figure 1.1).

Figure 1.1: Three- and two-generalist configurations appear to have the greatest stability and to act as the strongest “basins of attraction”.

Our study also confirmed the “four” part of Henderson’s rule – the 4:2:1 market-share ratio that tends to characterize equilibrium in these industries. Over the period studied, the top players in nearly 60 percent of industries with three-generalist structures had relative market shares of 1.5x to 2.5x, quite close to Henderson’s prediction of 2.0x. And we confirmed that today, the 4:2:1 relationship is the most prevalent among industries led by three generalists.

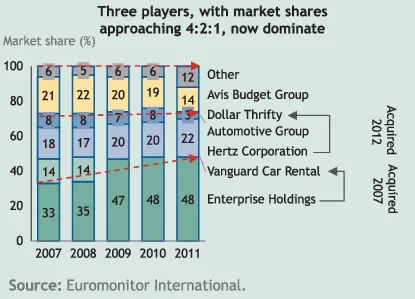

Current examples of the rule of three and four are easy to find. The U.S. rental-car industry is one (Figure 1.2). In 2006, four competitors – Avis, Enterprise Holdings, Hertz, and Vanguard Car Rental – had market shares exceeding 10 percent. The March 2007 acquisition of Vanguard by Enterprise, however, gave the latter nearly half the market – and set in motion competitive dynamics implicit in the rule of three and four. In fact, the market has closely followed Henderson’s script. In 2011, the three market leaders – Enterprise, Hertz, and Avis – had market shares of 48 percent, 22 percent, and 14 percent, respectively, close to the 4:2:1 ratio Henderson predicted. Hertz’s 2012 acquisition of Dollar Thrifty, which held a 3 percent market share at the time, made the numbers align even more closely with the rule.

Figure 1.2: The evolution of the U.S. rental car industry illustrates the rule of three and four.

All told, the rule of three and four appears to be very much alive and well today. But its applicability, as Henderson proposed, remains confined to “stable, competitive” industries characterized by low turbulence and limited regulatory intervention. Other examples of industries where the rule applies today include machinery manufacturing (companies such as John Deere, Agco, and CNH), household appliances (Whirlpool, Electrolux, and GE), and credit-rating agencies (Experian, Transunion, and Equifax).

The rule of three and four does not seem to apply to the growing number of more dynamic, unstable industries, such as consumer electronics, investment banking, life insurance, and IT software and services. Nor does it apply to industries where regulation hinders genuine competition or industry consolidation, such as telecommunications in the U.S. (for example, the U.S. government’s antitrust action against the merger of AT&T and T-Mobile).

The difference in applicability is stark. For companies in low-volatility industries led by three generalists, we measured a return on assets 6.1 percentage points higher than that of companies in low-volatility industries led by a larger number of generalists. Yet we found no such trend in high-volatility industries – the three-generalist configuration had no advantage over others. A possible explanation for this is that experience curve effects, which Henderson supposed underpinned the rule, are less applicable in industries where technological innovation and other factors shift the basis of advantage before the benefits of a lower cost position can be realized.

Rising turbulence in many industries has also reduced the rule’s impact over time. The higher return on assets associated with three-generalist structures, for example, has decreased, falling from an average of approximately 3 percentage points in the 1970s to roughly 1 percentage point today. The same holds true for the prevalence of the 4:2:1 market-share ratio among industries led by three generalists – that ratio is still the most common in such industries, but it is less common than it was at its peak.

Implications for Decision Makers

For corporate decision-makers, the rule of three and four has important implications. First, an understanding of the industry environment is critical. Is the industry one in which classical “rules” of strategy, such as the rule of three and four, apply? Or does it demand an alternative – for example, an adaptive – approach?2 Next, decision makers must determine whether their company has a long-term viable position in its industry. Where the rule applies, this is largely determined by market share. Being an industry’s largest player is the most desirable position; and the number two and three spots are also sustainable. Any other position is likely to be unsustainable.

Once they understand their company’s position, decision makers must shape their strategies accordingly. If the company is a top-three player, it should aggressively defend its share. If it is outside the top three, it should attempt to improve its position through consolidation or by shifting the basis of competition – or it should exit the industry. (As Henderson wrote, “… cash out as soon as practical. Take your writeoff. Take your tax loss. Take your cash value. Reinvest in products and markets where you can be a successful leader.”) If the company operates in an environment where the rule does not apply, it should employ adaptive or shaping strategies, which we will describe elsewhere.3

The rule has implications for other stakeholders as well. Investors, for example, should factor an industry’s dynamics and likely trajectory into their investment strategies. And policy makers should consider the rule and its ramifications as they weigh antitrust issues.

As we have seen, the rule of three and four remains relevant more than three decades after its conception – in a business environment that is, in many respects, profoundly different – and its implications continue to provide guidance for decision makers working in environments where classical business strategies hold. For companies in increasingly unstable environments, a new set of rules applies, calling for more adaptive approaches to strategy.

Notes

1

Our research, performed in collaboration with Professors Can Uslay, Ekaterina Karniouchina, and Ayça Altintig, employed Standard Industrial Classification (SIC) designations. Data were sourced from S&P Compustat’s database. In total, we studied more than 10,000 companies, from nearly 450 industries, representing more than $18 trillion in revenue in 2009.

2

See “Your Strategy Needs a Strategy,” Harvard Business Review, September 2012.

3

See “Adaptability: The New Competitive Advantage,” Harvard Business Review, July 2011.

Chapter 2 Revisiting the Experience Curve

MartinReeves

GeorgeStalk

FilippoScognamiglio

The experience curve is one of BCG’s signature concepts and arguably one of its best known. The theory, which had its genesis in a cost analysis that BCG performed for a major semiconductor manufacturer in 1966, held that a company’s unit production costs would fall by a predictable amount – typically 20...

Table of contents

Title Page

Copyright

Contents

Introduction

Part I: Updating the Classical Strategy Playbook

Part II: Mastering New Strategic Capabilities

Part III: Expanding the Boundaries of Strategy

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Dynamic Business Strategy by Martin Reeves, François Candelon, Martin Reeves,François Candelon in PDF and/or ePUB format, as well as other popular books in Business & Management. We have over 1.5 million books available in our catalogue for you to explore.