eBook - ePub

Asymmetric Demography and the Global Economy

Growth Opportunities and Macroeconomic Challenges in an Ageing World

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Asymmetric Demography and the Global Economy

Growth Opportunities and Macroeconomic Challenges in an Ageing World

About this book

The global demographic transition presents marked asymmetries as poor, emerging, and advanced countries are undergoing different stages of transition. Emerging countries are demographically younger than advanced economies. This youth is favorable to growth and generates a demographic dividend. However, the future of emerging economies will bring a decline in the working-age share and a rise in the older population, as is the case in today's developed world. Hence, developing countries must get rich before getting old, while advanced economies must try not to become poorer as they age.

Asymmetric Demography and the Global Economy contributes to our understanding of why this demographic transition matters to the domestic macroeconomics and global capital movements affect the asset accumulation, growth potential, current account, and the economy's international investment position. This collaborative collection approaches these questions from the perspective of "systemically important" emerging countries i.e., members of the G20 but considers both the national and the global sides of the problem.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

P A R T I

The Demographic Transition and the Macroeconomy: Setting the Stage

C H A P T E R 1

Demographic Asymmetries and the Global Macroeconomy

José María Fanelli and Ramiro Albrieu

This chapter sets the stage for the analysis in the rest of the book. We provide empirical and conceptual background concerning international demographic asymmetries and examine the consequences for the distribution of the international labor force, global savings, and the growth dynamics of countries experiencing different demographic stages. We focus on the countries of the G-20 and, particularly, the four emerging economies selected for the country studies: Brazil, China, India, and South Africa (see chapters 6–9). Based on this evidence, we discuss the implications for global imbalances, capital flows, and the required expansion of the domestic financial system in emerging market economies. We interpret the implications in light of the financial and monetary distortions and flaws in the rules of the game that the global postcrisis scenario reveals.

The analysis utilizes the findings of the literature on demography and growth, international capital movements, and financial development in emerging countries to identify and discuss a number of stylized facts that motivated our research hypotheses and contextualize our research results and policy questions. We aim to characterize demographic-driven forces that will have a bearing on the evolution of the international economy in the coming two decades and that consequently call for national and global initiatives that can be included on current policy agendas. Particularly important for developing countries is the fact that many of them are now going through the demographic bonus phase; if the opportunities associated with such phase are not exploited, they will be lost forever. In line with that aim, we will work with a shorter time horizon than what is canonical in the demographic literature because it is more suitable for the types of macroeconomic and financial issues that we will address.1 In this regard, consider that one of the main hypotheses motivating the project was that certain domestic and international macroeconomic and financial dysfunctions can become stumbling blocks along the path of the demographic transition, impeding emerging and developed countries from taking advantage of the opportunities that the asynchronous path of the global demographic transition creates.

1.1 DEMOGRAPHIC ASYMMETRIES: LABOR, SAVINGS, AND GROWTH

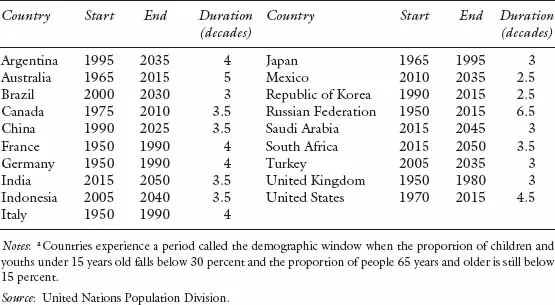

The global demographic dynamics reveals significant asymmetries across countries (Bryant, 2005). The concept of “the demographic window of opportunity” that we present in the introduction helps illustrate the existing and future evolution of demographic asymmetries. Applying this definition to G-20 countries and using United Nations (2013a) data yield the results shown in table 1.1.

Three facts stand out: the initiation year of the demographic window can differ substantially; developing countries enter this stage later than developed economies; and the duration of the demographic window is not constant across countries (United Nations, 2004). By the year 2100 the demographic transition will have ended (Lee, 2003). European countries entered the demographic window before Canada, the United States, and Japan. Emerging economies are either “children” (e.g., India and South Africa) or going through the demographic window (e.g., Argentina and Indonesia). Among rich countries, shorter windows (from two to three decades) correspond to Japan and the United Kingdom. Australia and the United States are ending longer windows (from five to six decades). In the case of emerging countries, the shorter windows are expected to occur in Mexico, Korea, Brazil, and Turkey and longer windows in Russia. With the exception of Russia, the duration of the demographic window in emerging economies appears to replicate the Japanese experience.

Table 1.1 The demographic window in G-20 countriesa

Global Reallocation of the Labor Force

Despite the asynchronous path of the demographic transition, the world is ageing. According to United Nations estimates, by 2030 the old age population (those above 65 years old) will have reached 12 percent of the total population, that is, nearly one billion people (United Nations, 2013a). Furthermore, ageing will accelerate over the coming years compared to previous dynamics (e.g., 1990–2010).

The old age population currently represents about 17 percent of the total population in advanced economies, but in 2030 it will have grown to about 24 percent. The situation in emerging economies is different: the working-age population is expected to maintain its share in total population in the future. A key consequence of the conjunction of asynchronies in the demographic path and global ageing is that the distribution of the world’s total labor force across countries is changing (see figure 1.1).

Although the characterization of advanced economies as the “old world” and emerging ones as the “young world” certainly reflect the current situation, we should not overlook the fact that important within-group asymmetries exist in advanced as well as emerging economies (see figure 1.2, and Wilson and Ahmed, 2010). The share of the working-age population in countries in the first group, such as Japan and Italy, peaked in the early 1990s; in France and Germany in the mid-1980s; and in the United States, the United Kingdom, and Australia in the late 2000s. We also see differences among the (future) peaks in the emerging economies’ working-age population. In South Africa and India the working-age population’s share is expected to peak in the 2040s, in Argentina and Brazil in the late 2010s, and in China in 2014. Differences are also foreseen in the speed of adjustment after the peak, with some countries (such as China and Brazil) expected to age at a faster pace than...

Table of contents

- Cover

- Title

- Introduction: The Project, the Results, and Policy Implications

- Part I The Demographic Transition and the Macroeconomy: Setting the Stage

- Part II Demographic Asymmetries and the Global System

- Part III On Challenges and Opportunities for Emerging Economies

- Bibliography

- List of Contributors

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Asymmetric Demography and the Global Economy by J. Fanelli in PDF and/or ePUB format, as well as other popular books in Social Sciences & International Business. We have over 1.5 million books available in our catalogue for you to explore.