This collection empirically and conceptually advances our understanding of the intricacies of emerging markets' financial and macroeconomic development in the post-2008 crisis context. Covering a vast geography and a broad range of economic viewpoints, this study serves as an informed guide in the unchartered waters of fundamental uncertainty as it has been redefined in the post-crisis period. Contributors to the collection go beyond risks-opportunities analyses, looking deeper into the nuanced interpretations of data and economic categories as interplay of developing world characteristics in the context of redefined fundamental uncertainty. Those concerns relate to the issues of small country finance, the industrialization of the developing world, the role of commodity cycles in the global economy, sovereign debt, speculative financial flows and currency pressures, and connections between financial markets and real markets. Compact and comprehensive, this collection offers unique perspectives into contemporary issues of financial deepening and real macroeconomic development in small developing economies that rarely surface in the larger policy and development debates.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Aleksandr V. Gevorkyan and Otaviano Canuto (eds.)Financial Deepening and Post-Crisis Development in Emerging Markets10.1057/978-1-137-52246-7_1

Begin Abstract

1. Emerging Markets and the Post-2008 World

Aleksandr V. Gevorkyan1 and Otaviano Canuto2

(1)

Assistant Professor of Economics, Dept. of Economics & Finance at Peter J. Tobin College of Business, St. John’s University, Queens, NY, USA

(2)

Executive Director at the International Monetary Fund, Washington, DC, USA

End Abstract

1.1 Introduction

This volume is about a diverse mix of experiences across a broad group of emerging markets in the post 2007–2008 crisis environment. The term “emerging markets” became popular at the beginning of the 1990s to designate some developing economies that were then being incorporated into massive flows of global finance. The category remained strong since then as a reference for those economies that were developing fast and differentiating themselves from other developing countries, while not yet belonging to the club of advanced economies.

Risks and opportunities to sustainable macroeconomic development vary across this wide variety of countries, shaped by a long list of country-specific factors and degrees of global exposure. Our book covers a wide range of issues on theoretical and empirical grounds, going from generic, country group, to country-specific analyses. Before outlining those issues, it is worth approaching a recent broader story of hype and gloom about emerging markets’ prospects that serves as a common background.

1.2 Emerging Markets and the Switchover of Global Locomotives: From Hype to Gloom

While advanced economies at the center of the post-2008 global economic crisis were going through their process of putting their houses in order, emerging markets as a group seemed to be on the way to become the new engine of global growth, leading some analysts to talk about a switchover of global locomotives (Canuto 2010). Prior to the global financial crisis, not only had those economies been on a path of convergence of per capita income levels toward the ones of advanced economies but also their post-2008 resilience seemed to point to their ability to keep high growth rates going on. Such a “decoupling” might even make them able to rescue advanced economies from their macroeconomic quagmire.

However, analyses of common emerging economies’ prospects oscillated rapidly from hype to gloom over the last three years. More recently, the enthusiasm about these countries’ post-2008 economic resilience and growth potential has given way to bleak forecasts, with economists like Ricardo Hausmann declaring that “the emerging-market party” is coming to an end (Hausmann 2013).

Many now believe that the broad-based growth slowdown in emerging economies since 2013 is not cyclical but is instead a reflection of underlying structural flaws. That interpretation has contradicted those (including one of ours, see Canuto 2011) who, not long ago, were anticipating a switchover in the engines of the global economy, with autonomous sources of growth in emerging and developing economies compensating for the drag of struggling advanced economies.

To be sure, the baseline scenario for the post-crisis “new normal” has always entailed slower global economic growth than during the pre-2008 boom. For major advanced economies, the financial crisis marked the end of a prolonged period of debt-financed domestic consumption, based on wealth effects derived from unsustainable asset-price overvaluation. The crisis thus led to the demise of China’s export-led growth model, which had helped to buoy commodity prices and, in turn, bolster gross domestic product (GDP) growth in commodity-exporting developing countries.

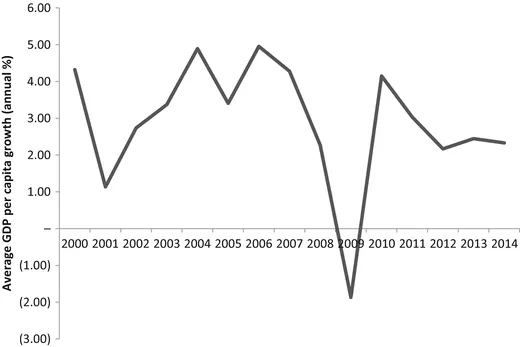

Against this background, a return to pre-crisis growth patterns could not reasonably be expected, even after advanced economies completed the deleveraging process and repaired their balance sheets. But developing countries’ economic performance was still expected to decouple from that of developed countries and drive global output by finding new, relatively autonomous sources of growth. Consider Fig. 1.1 that shows average growth rate for the Morgan Stanley Capital International (MSCI) Index (MSCI 2015) emerging markets group since 2000 reaching the peak by 2008, plunging in 2009, and yet gaining traction of the pre-crisis years. Note also that the crisis reaches the emerging markets in 2009 with a considerable lag—a factor in the initial optimistic reports on the global recovery at the time.

Fig. 1.1

Average GDP per capita growth rate for the MSCI emerging markets group. Source: Authors’ estimates based on the WDI (2015) data

According to this view, healthy public and private balance sheets and existing infrastructure bottlenecks would provide room for increased investment and higher total factor productivity in many developing countries. Technological convergence and the transfer of surplus labor to more productive tradable activities would continue, despite the advanced economies’ anemic growth.

At the same time, rapidly growing middle classes across the developing world would constitute a new source of demand. With their share of global GDP increasing, developing countries would sustain relative demand for commodities, thereby preventing prices from reverting to the low levels that prevailed in the 1980s and 1990s.

Improvements in the quality of developing countries’ economic policies in the decade preceding the global financial crisis—reflected in the broad scope available to them in responding to it—reinforced this optimism. Indeed, emerging countries have largely recognized the need for a comprehensive strategy, comprising targeted policies and deep structural reforms, to develop new sources of growth.

It has become apparent, however, that emerging-market enthusiasts underestimated at least two critical factors. First, emerging economies’ motivation to transform their growth models was weaker than expected. The global economic environment—characterized by massive amounts of liquidity and low interest rates stemming from unconventional monetary policy (Canuto 2013a) in advanced economies—led most emerging economies to use their policy space to build up existing drivers of growth, rather than develop new ones.

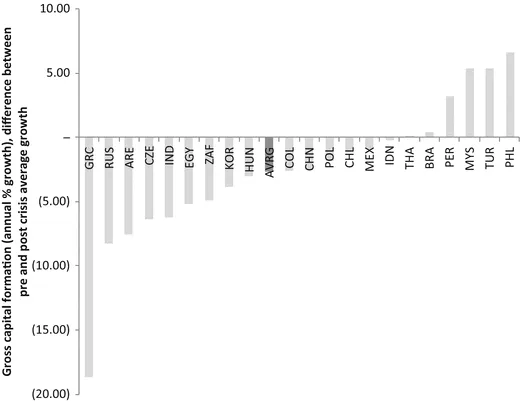

However, growth returns have dwindled, while imbalances have worsened. Countries like Russia, India, Brazil, South Africa, and Turkey used the space available for credit expansion to support consumption, without a corresponding increase in investment. China’s nonfinancial corporate debt increased dramatically, partly owing to dubious real-estate investments. The trend is clearly visible in Fig. 1.2 that shows the difference in average gross capital formation growth rates between the post- and pre-crisis periods (see the Note for technical clarification). The pattern is quite diverse across current members of the MSCI index, with investment rates on average declining in the post-crisis “recovery” period.

Fig. 1.2

Total investment: difference between post- and pre-crisis annual growth rates for the MSCI emerging markets group. Source: Authors’ estimates based on the WDI (2015) data. Note: Pre-crisis period covers 2000–2008 while post-crisis includes 2010–2015. See Appendix Table 1.1 for country codes

Moreover, not much was done in anticipation of the end of terms-of-trade gains in resource-rich countries like Russia, Brazil, Indonesia, and South Africa, which have been facing rising wage costs and supply-capacity limits. Fiscal weakness and balance-of-payments fragility have become more acute in India, Indonesia, South Africa, and Turkey.

The second problem with emerging-economy forecasts was their failure to account for the vigor with which vested interests and other political forces would resist reform—a major oversight, given how uneven these countries’ reform efforts had been prior to 2008. The inevitable time lag between reforms and results has not helped matters.

Nonetheless, while emerging economies’ prospects were clearly over-hyped in the wake of the crisis, the bleak forecasts that dominate today’s headlines are similarly exaggerated. There are still a number of factors indicating that emerging economies’ role in the global economy will continue to grow—just not as rapidly or dramatically as previously thought.

In the summer of 2013, the mere suggestion of a monetary-policy reversal in the USA sparked a surge in bond yields, which triggered an asset sell-off in several major emerging economies (Canuto 2013b). After bouts of volatility since then, global financial markets went through an extraordinary new wave of sharp sell-offs and increased volatility in the last few weeks of the summer of 2015, with equity markets and currencies across a range of emerging markets being especially hit. While recent financial events and policy responses in China may be pointed out as triggers of such emerging-market asset massive sell-off (Canuto 2014), it corresponded to an intensification of underlying, structural trends already at play.

1.3 Emerging Markets Face a Redefined Fundamental Uncertainty

In the context of the above discussion, Gevorkyan and Gevorkyan (2012a) suggested that the post-2008 crisis global economy environment may be characterized as one of “redefined fundamental uncertainty” (RFU): At the current stage, the newly realized interconnectedness of the global finance and the reality of new trade patterns—like global value chains (Canuto 2015)—render greater instability and uncertainty, particularly in emerging markets. Specifically, there are six RFU conditions that are also related to the risks facing the emerging markets today. Those are:

Global market and interlinks—financial and economic contagion.

Asset prices volatility (e.g., carry trade and commodity derivatives).

Short-run returns maximization and global speculation.

Evident decoupling of financial and real spheres.

Global economy rebalancing: deindustrialization, industrialization, and uneven human capital.

Sovereign debt pile-up and limited access to (and/or run-down on) international reserves.

All six aspects of the RFU are the subject of daily discussions and analysts’ commentary. The authors, however, remark the need to approach them all together as connected features of the current international ...

Table of contents

Cover

Frontmatter

1. Introduction

2. Emerging Markets’ Post-2008 Trends

3. Region and Country Case Studies

Backmatter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Financial Deepening and Post-Crisis Development in Emerging Markets by Aleksandr V. Gevorkyan, Otaviano Canuto, Aleksandr V. Gevorkyan,Otaviano Canuto in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.