This book explores the challenges faced by the Japanese economy and the Japanese banking industry following the financial crisis that emerged around the turn of the last millennium. The author explores how the Japanese financial crisis of the late 1990s engendered huge restructuring efforts in the banking industry, which eventually led to even more sweeping changes of the economic system and long-term deflation in the 2000s. The discussion begins with an overview of the unconventional monetary policy launched by the Bank of Japan at this time, while banking administrative policies maintained their strict code of governance. The author describes how, just as recovery seemed possible, the twin disasters of the Lehman shock and the Great East Japan Earthquake buffeted the recovering economy, and pushed Japan again into deflation. The book also looks to the very recent past, with the sudden advent of Abenomics in 2013, with its three-pronged approach, which was intended tobreak the deflationary mindset. Finally, the author projects what the future of the banking industry in Japan might encompass, as looming demographic changes gradually threaten both the economy and the banking industry.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Mitsuhiko NakanoFinancial Crisis and Bank Management in Japan (1997 to 2016)Palgrave Macmillan Studies in Banking and Financial Institutions10.1057/978-1-137-54118-5_1

Begin Abstract

1. Financial Crisis and Banking Crisis in Japan: 1997–2003

Mitsuhiko Nakano1

(1)

Momoyama Gakuin University (St. Andrew’s University), Osaka, Japan

End Abstract

1.1 Introduction

The banking crisis from the late 1990s in Japan remains the most memorable incident in Japanese financial history. It was commensurate with the Showa Kin’yu Kyoko, the Showa financial crisis in the 1930s, following the global Great Depression that began in 1929. The banking crisis led to a restructuring of the banking industry, which had not changed for 50 years after World War II. In this chapter, first the banking crisis that occurred mainly during 2000–04 is specifically examined. Secondly, causes, bank behaviours, political reactions including monetary policy, and the results are reviewed. In this book, the financial crisis is defined as a financial turmoil that includes all financial institutions from the early 1990s to the mid-2000s. The banking crisis is defined particularly as bank failures during 1998–2004. In that sense, the banking crisis is included in the financial crisis in terms of both substance and period.

1.2 Outline of the Banking Structure in Japan

The banking structure in Japan is a hierarchical one similar to those in other nations. It was established during the Meiji period (1868–1912). The banks in Japan are classified fundamentally by their origin and business area. The city banks are in the top tier. The regional banks are in the second one. The second regional banks are in the third tier. Finally, the cooperative financial institutions are in the fourth tier. Their numbers and the deposits controlled by organizations of each classification are presented in Table 1.1. In the late 1980s city banks numbered 13, reducing to 11 by April 1996 because of mergers. These have agglomerated into five in the four financial groups after the restructuring that occurred at the beginning of the 2000s. The regional banks numbered 64 in the 1980s, the same as in 2015. The second regional banks1 numbered 68 in the late 1980s; there were 41 in 2015. The cooperative financial institutions mainly consist of entities in four categories: the Shin’yo Kinko (Shinkin), the Shin’yo Kumiai (Shinkumi),2 the Rodo Kinko (Rokin),3 and the Nogyo Kyodo Kumiai (Nokyo),4 and others. The cooperative financial institutions have been aggregated since the early half of the 1990s.5

Table 1.1

Outline of the Japanese banking industry (trillion yen)

Mar. 1991a

Mar. 2015

Category

Numberb

Deposit

Numberb

Deposit

Domestic banking account

147

513.9

110

717.1

City banks

12

227.7

5

327.0

Regional banks

64

155.0

64

252.9

Second regional banks

68

59.0

41

64.8

Long-term credit banks

3

55.9

0

0

Shinkin

451

82.6

267

132.0

Shinkumi

407

22.4

154

19.2

Norinchukin banks

1

25.2

1

56.8

Agricultural cooperatives

3574

56.1

679

93.7

Japan Post Bank

1

136.2

1

177.2

Source: Japanese Bankers Association Kin’yu

Note:

aFY1990 ended in March 1991 was the peak year of the bubble economy in Japan

bThe number of each financial institution

In addition to the private financial institutions, a few financial institutions exist under the control of the government. Japan Post Bank Co. Ltd. (Japan Post Bank) which used to be part of the public agency, the Japan Post, is undergoing privatization. Japan Finance Corporation (JFC) is an institution wholly owned by the government and providing financial support to small and medium-sized enterprises (SMEs) and individuals. Development Bank of Japan Inc. (DBJ) is in charge of supporting industries financially based on the industrial policies of the government. Japan Bank for International Cooperation (JBIC) is responsible for supporting government policies in terms of internationally financial support, mainly to enterprises.

In terms of the deposit amount, it is readily apparent that the city banks are much larger than regional banks. For example, the deposit size of the city banks, on average at present is 20 times that of the regional banks. The average size of Shinkin is much smaller than that of the regional banks, reflecting their inherent histories.

Business functions of the financial institutions have been similar in terms of financial intermediaries, but the sizes of clients and scope of operations in addition to business areas have differed depending on their place in the financial hierarchy. The three megabanks have some background as a financial centre of a particular business concern such as the Mitsui Group, the Mitsubishi Group, the Sumitomo Group, and the Fuyo Group.6 The business areas of the megabanks extend not only throughout Japan but also all over the world. Their clients vary from individuals to large listed firms including transnational firms. However, the regional banks and the cooperative financial institutions originated as local financial institutions operating in one particular district. Therefore their clients are fundamentally limited to individuals and business entities in each district.

1.3 The Bubble Economy and Its Collapse

1.3.1 The Three Causes of the Bubble Economy

The Japanese economy was highly boosted and rapidly growing in the late 1980s. It was known as ‘the bubble economy’. The causes had originated in the 1970s during the two oil shocks. In the 1970s, demands for fixed investment of private firms in Japan decreased markedly and the annual Gross Domestic Product (GDP) growth rate in real terms declined from about 10 per cent in the 1960s and the early 1970s to less than half that. Then large firms had surplus funds for undefined uses. However, the government adopted an expansionary fiscal policy to inspire the economy. The bond market became larger and larger through large issues of Japanese Government Bonds (JGBs). As a result, high demand for financial investments was amplified. The result resembled the disintermediation phenomenon prevailing in the US financial market in the early 1970s.

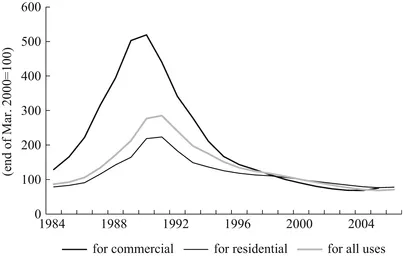

The US government under the presidency of Ronald Reagan strongly requested in the early 1980s that Japanese financial markets be deregulated and opened up to foreign financial institutions and investors. Under these circumstances, multinational firms and other large firms switched their funding sources from commercial banks to capital markets. As a result, the large banks rushed to expand mortgage loans responding to the sharp rise in real estate prices. The movement of land prices in Japan is shown in Fig. 1.1. Banks were trying to win a competition under inexperienced financial deregulation. The financial authority itself inspired them to take risks and mutually compete.

Fig. 1.1

Trends in urban land price index. Note: Figures are based on ‘six large city areas’ (Source: Japan Real Estate Institute ‘urban land price index’)

So many discussions have taken place about the causes of the Japanese bubble economy of the late 1980s. The situation can be summarized as follows, in comparison with the Subprime Loan Crisis in the USA and the banking crisis in Europe. The first cause was government economic policy. The Japanese government needed to inspire the domestic economy to increase imports because the trade surplus against the USA had become an important political issue in both countries. The G5 countries had already agreed to an alignment of the foreign exchange rates against the US dollar at the Plaza Hotel in September 1985: the so-called Plaza Accord. The Japanese government intervened in the foreign exchange market by selling the dollar in the market. The Japanese yen to US dollar exchange rate increased by 34.1 per cent from 237.10 yen at the end of August 1985 to 156.05 yen at the end of August 1986, as shown in Fig. 1.2. According to this appreciation, the purchasing power of the Japanese yen had been greatly increased.7 To prevent the further rise of the yen, the government intervened in the foreign exchange market by buying a huge amount of US dollars by selling Japanese yen. However, the Bank of Japan (BOJ), the central bank of Japan, did not adopt a sterilization policy. As a result, a huge amount of yen remained in the money market. The liquidity held by the banks increased considerably and led to the funding of speculative investments. However, the government tax revenues increased along with asset inflation in terms of a fixed property tax and a tax on income from real estate transfers. This functioned as an incentive for the government to continue with the existing conditions.

Fig. 1.2

Japanese yen to US dollar exchange rate: 1973–95. Note: Figures are based on a monthly average (Source: The Bank of Japan)

Th...

Table of contents

Cover

Frontmatter

1. Financial Crisis and Banking Crisis in Japan: 1997–2003

2. Change in Banking Supervision Policy and Their Effects on Bank Behaviour: 2002–05

3. The Lehman Shock and Its Influence on Banking Supervision Policy: 2008–13

4. The Launch of Abenomics and Its Effects on the Banking Business

5. The Future of Banking Management in Japan

6. Conclusion

Backmatter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Financial Crisis and Bank Management in Japan (1997 to 2016) by Mitsuhiko Nakano in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over 1.5 million books available in our catalogue for you to explore.