eBook - ePub

Retail Banking

Business Transformation and Competitive Strategies for the Future

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

The world of retail banking is changing. While previously a purely money-making entity, the industry has brought social responsibility onto its agenda, and the ground rules for success have altered. Traditional convictions, rules and values that have influenced all banking business in the past are brought into question by this shift, and banks are adopting bold strategies in order to win out over competitors.

Taking both multidisciplinary and holistic approaches, Retail Banking is a comprehensive analysis of how traditional retail banks can meet the challenges of the emerging competitive landscape. It outlines the importance of considering the traditional fundamentals of banking and fitting them into the modern times, where technology is pervasive and developments in the macro and micro scenarios have changed the landscape of the industry. It highlights that modern retail banking is a conscious step away from the past, and suggests that for banks to succeed in this field, they must step away from ad-hoc initiatives and instead encourage loyalty and a life-long confidence in each of their customers.

This book will be of interest to those with in interest in retail banking, bank management, business models and strategies and financial services.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Appendix 1

Some Highlights on Bank Practices: Packaged Products, Bundling, and Tying

Bundling and tying are distinct practices with the common purpose of cross-selling to customers. When these products are available only as a bundle, we have pure bundling. Mixed bundling is when products are available separately and can be offered at a discount relative to their individual prices. Bundling products can be differentiated with the help of the following criteria:1

–The level of customization and integration between the different products and services involved;

–The underlying degree of expertise with the service provider for each of the products and services involved; and

–The value added for the customer, which is the ultimate goal of bundling.

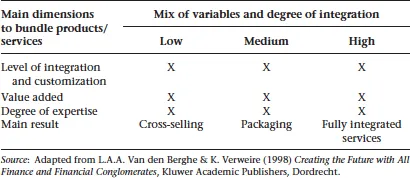

Many types of bundled services are developed at great speed in the market for financial services. Although it is not always easy for an outside observer to evaluate the degree of integration and customization as well as the level of expertise of the service providers and consequently the value added for the customer, some broad lines are clearly observable. The graph below gives a visual picture of the different types of bundling.

Table A1.1 Types of bundling: a representation

Two extreme cases can be observed, and between them a wide range is possible. At one end of the spectrum stands cross-selling with the lowest degree of integration and customization, with a limited scope of different expertise involved and a relatively low level of value added. Here, the emphasis of the supplier’s strategy is more on the volume of business and this from a perspective of transactional marketing.

At the other extreme, we find the fully integrated services with a high degree of integration and customization, many experts involved, and a high value added for the customer. Here, the supplier is looking for a competitive edge in tailoring different complementary products and services, such as personalized from a lifetime perspective or built around specific needs or events. This is a typical approach for relationship marketing and builds customer loyalty. Such an approach supposes a great deal of individual information per client, long-term planning in relation to the life cycle of the client with different event scenarios, and a dynamic approach for flexible updating and adaptation.

In between, all types of packaging can be found, with intermediate positions on the level of integration, customization, expertise, and value added. It must be said that products produced in different factories are unbundled and re-bundled to tailor them to the needs of specific client segments in order to offer them an integrated personalized solution.

The main idea for the future is to work with modular concepts. These modules form the building blocks around which new financial products can be built. This new approach allows for some standardization (there are only a few modules), but on the other hand, the combination of different modules and other features makes it possible for a financial firm to develop products tailored to the specific needs of a customer. For the moment, this is at best in the planning phase: a small number of companies are thinking of applying this idea in practice shortly.

Tying is another bank practice in which the purchase of one product is conditional on the purchase of another. In other words, tying occurs when two or more products are sold together in a package, and at least one of these products is not sold separately. Product tying is a common strategy for retail banks throughout the EU. Because it is relatively expensive and difficult for banks to win new customers, they often decide to focus their growth strategy on increasing cross-selling to existing customers. Product tying offers a simple way of increasing cross-selling. Such product ties are found in a range of core retail banking products, such as:

•Selling a current account to a consumer buying a mortgage or personal loan;

•Selling payment protection insurance or life insurance to a mortgage customer; or

•Selling a current account to an SME taking out a business loan.

The main advantages for financial institutions that sell packaged products, product bundles, or who tie products, are essentially concerned with the amount of cross-selling, since the customer is sold a number of products at the same time to meet a range of needs. For example, mortgages are usually accompanied by home insurance and possibly life assurance. The customer may also be required to open a current account if they are not already customers of the institution providing the mortgage. From the customer’s point of view, this does simplify the process, since all products can be purchased at the same time. The financial institution hopes that this bundle of products is going to strengthen its ties with the customer. Packaged products or bundles are most effective when they are meaningful to the customer and his or her needs, and also when the value of the bundle is more than the total value of the individual products. However, in many situations, it is difficult for the customer to assess the relative value of each of the components of the bundle.

Appendix 2

How Some Retail Banks Describe their Retail Banking Activities

In the following Tables A2.1–2, we illustrate how several large banks around the world describe their retail banking activities in their own words.

This group of banks certainly does not constitute an exhaustive list of institutions that provide detailed information on their retail banking activities. However, it is interesting to look at the passages cited here because they are representative of the information provided by some large banking organizations that identify distinct retail business segments on their website, even though some of them do not refer to such activity with this term but mostly explain their activity for individuals, families, and businesses.

We outline the key sentences to give a flavor of the different retail banking styles; in particular, we outline some profile information, the vision and mission, and the key values and beliefs. All this is taken and adapted from the banks’ websites on May 12, 2014.

Table...

Table of contents

- Cover

- Title

- Part ISetting the Scene: Using Past Experience to Inform the Future of Retail Banking

- Part II Controlling Consumption and Engaging Customers Seems to be the Issue for Every Retail Business

- Part III The Retail Banking of Tomorrow

- Appendix 1 Some Highlights on Bank Practices: Packaged Products, Bundling, and Tying

- Appendix 2 How Some Retail Banks Describe Their Retail Banking Activities

- Appendix 3 EU Retail Banking: An Overview

- Appendix 4 US Retail Banking: An Overview

- Appendix 5 Retail Banking in the Rest of the World: An Overview

- Appendix 6 The Net Interest Margin as the Key Root Value Driver for Retail Banks

- Appendix 7 Information Asymmetry in Retail Banking

- Notes

- Bibliography

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Retail Banking by A. Omarini in PDF and/or ePUB format, as well as other popular books in Technology & Engineering & Business General. We have over 1.5 million books available in our catalogue for you to explore.