This book provides a comprehensive and practical guide to Islamic finance. It covers abroad range of important topics including Islamic banking, capital markets, Takaful, wealth management, Fintech in Islamic finance, compliance and governance issues.

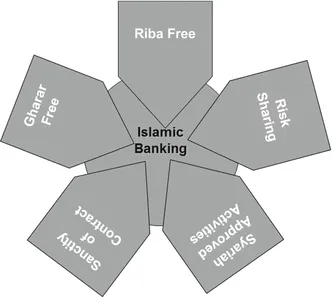

It begins by introducing Islamic banking, covering its objectives, principles and evolution, before moving on to discuss the religious foundations of Islamic finance. The prohibition of Riba and Gharar and Islamic contracts are explored, before Islamic deposits, and financing are discussed in practice. A comparative analysis is provided between Islamic banking products and services in a range of counties throughout the world. Information technology including fintech, payment and settlement networks, opportunities and challenges are also addressed. Corporate governance, Islamic capital markets, and Islamic insurance (Takaful) are all explored, before concluding with a chapter on wealth management and Islamic investment funds. Itfeaturescase studies based on the authors' own experiences consulting with Islamic financial institutions.

Ideal for those looking to improve their understanding of practical Islamic financing models, contracts, product structures and product features, this book will appeal to both students and practitioners in Islamic finance and banking, those based in Islamic financial institutions, and those based in conventional financial institutions who may be looking to enter the Islamic financial market.