Mortgages were among the most important and widely used financial instruments in the pre-modern European countryside; offering land as a collateral for a loan was a technique used from the Mediterranean to the British Isles. Land was a popular form of collateral for loans because it cannot disappear, or be taken away or hidden from creditors (or: mortgagees), and is therefore generally regarded as a particularly strong security. Only land has this particular quality: all other assets can be destroyed or removed by debtors (or: mortgagors) trying to prevent creditors to recover losses. Similarly, persons acting as guarantors and sharing liability for a debt can become impoverished, run off or pass away.

No wonder then that land was already used as a security in Biblical times. The book of Nehemiah, written around 400 BCE, and describing events around 450 BCE, already mentions the mortgaging of land by peasants looking to cope with dearth. By doing this, the peasants managed to borrow, so they could buy food, but there was also a downside to the transaction, as the debtors lost their right to the land for as long as they did not repay their creditors. They complained: ‘we are helpless because our fields and vineyards belong to others’ (Nehemiah 5:3–4). Hearing of this, an angered Nehemiah then proceeded to speak to the creditors, telling them:

please, give back to them this very day their fields, their vineyards, their olive groves and their houses, also the hundredth part of the money and of the grain, the new wine and the oil that you are exacting from them. (Nehemiah 5:11–12)

Apparently, as this chapter from the Book of Nehemiah shows, 2500 years ago creditors were willing to lend on collateral of land and this continued to be a preferred security ever since.

This volume is dedicated to the use of land as a collateral for loans. This topic is first of all important from a financial-historical point of view, as it deals with the question of how participants in exchange could secure transactions. A second reason to study mortgages is their role in economic and social change. The use of land as a collateral for loans has been linked to agricultural transitions that brought about the productivity improvements in the rural economy that are regarded as a prerequisite for sustained economic growth. The precise role of mortgage credit in this development is still unclear: did it allow enterprising peasants access to credit so they could invest and extend their landholdings? Or did it contribute to impoverished peasants eventually losing their land to their creditors—as apparently already happened in the time of Nehemiah?

The various chapters of this book all deal with the financial, economic and social aspects of mortgage credit in the pre-modern European countryside. They are all case studies into the actual use of land as collateral for loans, and the effects on economy and society. Such an approach is fruitful, as scholarship on the use and effects of mortgage credit is too often of a theoretical nature, assuming certain practices and their effects, rather than establishing these based on archival research. This empirical research has been ongoing for quite some time now, and some of the more recent results were, for instance, presented in a volume on rural credit edited by Schofield and Lambrecht (2009). Whereas these authors took an all-encompassing view that included the enormous number of ‘small-scale credit agreements’ of the pre-modern countryside (Schofield and Lambrecht 2009, p. 4), the present volume is focused on what one might call rural ‘high finance’: large loans on collateral of land. One of the main focal points is the development of mortgage contracts and mortgage law over time: the pre-modern European countryside was characterized by regional variety of mortgage contract types. As a result, conditions for lenders and borrowers were not the same everywhere, and large differences can be observed in the use of land to secure loans, as well as the use and socio-economic effects of mortgage credit. The contributions to this volume indicate a gradual convergence of mortgage contracts and mortgage law: initially, these provided much security to the lender, but over time there was a general development towards a more balanced ‘mortgage system’ that also looked after the interest of the borrower. It seems that this process of ‘institutional change’ was crucial for turning mortgage credit into a very popular credit instrument and that this was achieved in many European areas by the seventeenth century.

Rather than presenting a general overview of the historiography on mortgage credit—for this we refer to the excellent introduction to this topic by Lambrecht and Schofield (2009)—the introduction rather discusses the contract types used for mortgaging, the development of mortgage contracts and mortgage law, and their relation to economic growth and social developments. We begin with sketching the contract types available to those looking to use land to secure a loan.

1.1 Mortgage Contracts and Mortgage Law: Security, but for Whom?

Participants in many economic transactions deal with what Avner Greif called the ‘fundamental problem of exchange’: the risk that a counterparty does not live up to his or her obligations (Greif 2000). This problem occurs in any transaction where payment is postponed; to solve it—or at least minimize the risks involved—creditors are likely to demand securities from their debtors. Securities tend to come in many forms, ranging from informal arrangements, such as having witnesses to a transaction, to more formal arrangements, such as drawing up a legally binding contract. Usually, more valuable transactions require more formal securities: once a deal exceeds a certain value, the creditor is likely to demand stronger securities. On the one hand, this is because bigger loans can result in bigger losses, while on the other hand, it reflects the fact that bigger loans make cheating more attractive for the debtor: when the gains of cheating outweigh the damage of (for instance) reputation loss, informal securities no longer suffice, and creditors will demand formal securities, such as mortgages. Generally speaking, once loans exceed a certain threshold, it becomes worthwhile for creditors to demand a mortgage as a security. Michael Schraer’s chapter in this volume, for instance, demonstrates that medieval Jewish moneylenders’ mortgage-backed loans were substantially bigger than their other loans, suggesting a relation between loan size and the use of collateral as a security. Other case studies indicate that mortgages were not taken out for loans worth less than at least a month’s wages ; in fact, usually the principals easily exceeded several months’ wages (Lambrecht 2009, p. 78, and the chapters below by Dermineur, Gayton, Van Onacker and Wedd ).

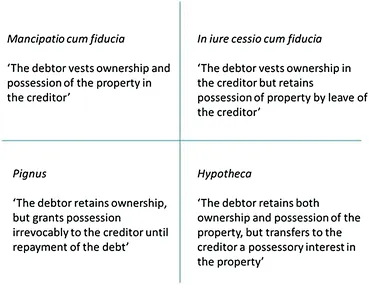

Mortgage contracts differed: some provided creditors with strong securities, allowing them almost automatic compensation once the debtor failed to repay the loan, or failed to pay mortgage interest . Others allowed debtors more leeway and did not result in immediate expropriation as soon as a single payment was missed. In general, it seems there were four contract types available in pre-modern Europe. They differed in terms of possession—who was allowed to work the land that was put up as a security?—and ownership—who held legal title to the collateral? Figure 1.1 gives the main contract types, based on Goebel’s (1961) reconstruction of securities of Roman law . Even though Roman law was not used everywhere in Europe, and the Latin terms mentioned in the scheme hardly ever emerge in the historical records, the figure does provide a general idea of the options available to creditors and debtors looking to use land to secure a transaction.

Fig. 1.1

Real securities of Roman law

Source Goebel (1961, p. 29)

A first option—mancipatio cum fiducia—was to provide the creditor with relatively strong security, granting him or her both possession and ownership of the land until the debtor repays the principal. In contrast, another option was to provide the creditor with relatively little security, by using the hypotheca that only granted him or her ‘a possessory interest in the property’: until a judge allows the creditor to execute his or her claim to the collateral, the debtor retains both ownership and possession. In between these two extremes, we find the pignus that allowed the creditor possession of the collateral, and the in iure cessio cum fiducia (or fiducia) that allowed him or her the ownership while the debtor was allowed to continue in the possession of the collateral. In the European countryside of the later Middle Ages and early modern period, we encounter contracts resembling the pignus (Ertl 2017, p. 15), and most of all the fiducia and hypotheca: contract types allowing the debtor to retain possession of the land for the duration of the mortgage contract were most usual.

An angered Nehemiah had to deal with debtors who had secured a loan by transferring ownership to their creditors, thus losing title to their lands, or so it seems at least. In theory, they could recover the land by repaying the debt plus possible interest— conditions similar to what later would be known as the fiducia of Roman law . This also was the usual type of contract used in Italy (De Luca and Lorenzini, this volume). And even though England did not have a Roman law tradition, using land as a collateral went along the same lines there as well (see the chapters here by Briggs, Gayton, Waddilove and Wedd ). In Flanders, such contract types were common in the thirteenth century (Thoen and Soens 2009, p. 24) but seem to have been used less often in later centuries. Here, another contract type—the hypotheca—emerged and was generally used from the late Middle Ages onwards. It provided the creditor with a claim to the property, so that he or she could expropriate in case of default . The debtor retained ownership and possession for the duration of the contract, unless a judge intervened and ordered expropriation to compensate the creditor for default . Here, the position of the creditor was less strong, as expropriation required a court order; the debtor was in a better position, as he or she retained ownership until a judge ordered expropriation. This was the usual type of contract in the north-west of mainland Europe (see the chapters by Dermineur, Limberger and De Vijlder, Van Onacker and Zuijderduijn ).

For creditors, the fiducia was the more attractive contract type; for debtors, this was the hypotheca. The former appears to have been available almost everywhere in the Middle Ages, whereas the latter only emerged in the course of the later Middle Ages, first in the north-west of Europe and the Iberian Peninsula, and later also in England and Italy . The general development of mortgage credit involved a move towards more debtor-friendly mortgage contract types. Schraer discusses how the introduction of the censal—which resembles the hypotheca—in late medieval Aragon gained so much popularity that it caused Jews— who usually used the pignus contract type—to lose ground. In Italy, a new contract type resembling the hypotheca was introduced towards the end of the sixteenth century, to protect the debtor: the chapter by De Luca and Lorenzini describes how the census consignativus improved the position of the debtor by no longer requiring...

Table of contents

Cover

Front Matter

1. Introduction: Mortgages and Annuities in Historical Perspective

2. Mortgages and the English Peasantry c.1250–c.1350

3. Mortgages Raised by Rural English Copyhold Tenants 1605–1735

4. Mortgages and the Kentish Yeoman in the Seventeenth Century

5. Why the Equity of Redemption?

6. Credit and Land: The Jews of Zaragoza 1383–1400

7. Not Only Land: Mortgage Credit in Central-Northern Italy in the Sixteenth and Seventeenth Centuries

8. Rural Credit Markets in Eighteenth-Century France: Contracts, Guarantees and Land

9. The Use of Perpetual Annuities in Rural Brabant in the Fifteenth and Sixteenth Centuries

10. Proactive Peasants? The Role of Annuities in a Late Medieval Communal Society: The Campine Area, Low Countries

11. The Other Fundamental Problem of Exchange: Mortgages, Defaults and Debtor Protection in Sixteenth-Century Holland

12. Afterword: Mortgages as Mediation Between Kin and Capital

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Land and Credit by Chris Briggs, Jaco Zuijderduijn, Chris Briggs,Jaco Zuijderduijn in PDF and/or ePUB format, as well as other popular books in Economics & Financial Services. We have over 1.5 million books available in our catalogue for you to explore.