This book responds to key issues in strategic management control by studying the interplay between strategy, operations, finance and controls. Grounded in research but written with practitioners and students in mind, it addresses the most up-to-date management control issues in the public sector, forecasting, budgeting and controls in international organisations.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

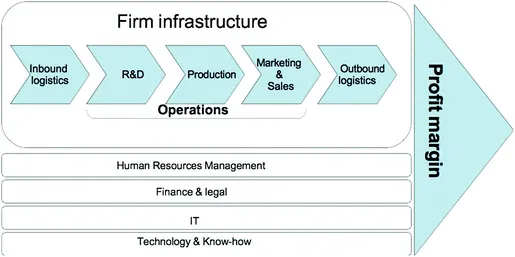

Value chain accountingGeneric strategyPosition on the marketMode of production

End Abstract

Management accounting is too often reduced to managerial accounting or cost accounting, as though costing were the sole central issue to managers. Yet, the usefulness of management accounting reports lies in data relevancy for management, i.e. the extent of their supporting of decision-making (Anthony, 1965, 1988). That is, strategic management accounting consists of accounting for what is especially pertinent for decision-making: accounting for what counts. In relation with this, there is no unique way of accounting for what is pertinent, i.e. outwith mere absorption or variable costing . Thence, strategic management accounting consists of accounting for what counts in a way that counts. What counts and how this counts require first that strategy be well identified, followed by what deserves to be accounted for and subsequently unlimited options for working units. In order to understand these issues in strategic management accounting, it is crucial to understand the notion of the value chain first: the organisation of activities that relate to the company’s core business, those coming in support and those peripheral (McGahan & Porter, 2002; Montgomery & Porter, 1991; Porter, 1985). Figure 1 presents the generic version of the value chain , however, knowing that each company’s value chain is unique, depending on its strategic issues.

Fig. 1

The value chain

Strategic management accounting consists of identifying at all times what the optimal value chain would be for the company. This consists of clearly identifying the generic strategy adopted by the company, as well as its position on the market and lastly the required mode of production . Each of these strategic reasoning’s three pillars highlights specific and different challenges for management accounting. It is therefore crucial that the management accountant be extremely vigilant as to what counts as strategy prior to determining what management control and accounting system is most suitable.

1 Accounting for Generic Strategies

The identification of strategy rests upon the understanding of the organisation’s business model traditionally revolving around five pillars (Kaplan & Norton, 2000, 2004): generic strategies, position on the market , product life cycle , mode of production and products’ or services’ international exposure. The first three dimensions are quite well known; they should have been studied in strategic management courses. The very novelty in this addressing of business models lays in the fact that mode of production relates to organisation theory, but not only: also operational management and international products and services to international management, international branding, etc.

1.1 Generic Strategies

The strategic management literature mainly views two generic strategies with specific implications in terms of value chain ’s organising and business model’s developing: cost domination vs. differentiation (Porter, 1985). As these two generic strategies are often presented as ideal types, it is more common to see bundle of both, consisting of differentiation at a reasonable cost .

1.1.1 Cost Domination

A company adopting a cost domination strategy sets out to offer the same product or service as competitors at a cheaper price. In this case, the strategic objective is to minimise all possible costs in order to maintain the same profit margin as other competitors within the industry. So doing implies that the main three types of costs are perfectly known and understood and their pertinence reviewed continually, viz. overhead , labour and materials .

Outwith the mere management of costs per se, a cost domination strategy implies an adapted business model or value chain . In order to minimise costs, the pertinence of each link in the value chain is questioned. Only costs directly enabling financial value creation are viewed as pertinent and can be retained. Conversely, links and associated costs perceived as irrelevant or peripheral to value creation deserve to be cut. Most often, a cost domination strategy is associated with a value chain focusing on core business activities, those deemed peripheral being outsourced (McGahan & Porter, 2002; Porter, 2008). The most common peripheral activities are seen as payroll, IT (Porter, 2001) or other services, such as cleaning or guarding. In other words, a cost domination strategy can be understood as the strictest application of Transaction Cost Theory’s canons: if an activity and the costs associated thither are not central to making profit , these should not be internalised but left to the market (Williamson, 1979, 1981).

Most of the time, cost domination strategies occur in mature industries with historical operators whose position on the market has never or rarely been contested by competitors. Such a strategy is often seen on growing markets attracting new competitors. New competitors’ joining results in an atomised market where customers have a large choice of product or service providers and then search for affordable options (McGahan & Porter, 2002; Montgomery & Porter, 1991).

Airlines are especially concerned with the emergence of new business models based on pay-for-service, since numerous companies went bankrupt since the 2000s’ (Alitalia, Swissair, Delta Air Lines, etc.). The advent of next economy’s companies has also challenged traditional business models in other activities, such as bookstores with Amazon (J. Morris, 2017; Stone, 2014).

Case n°1. Virgin Atlantic vs. British AirWays

Cost DominationStrategy

Since the early 2000s, British Airways has been confronted with major financial challenges, like other national airline companies : increasing costs and the advent of low fares airlines. Amongst them is Virgin Atlantic whose strategy is deliberately to beat the competition on costs. In order to achieve this, the company has developed an alternative business model to what other airlines would do:

an airline’s core business is to fly passengers from one port to another;

no or very limited free service onboard (pay for other service: entertainment, snacking, beverages, etc.);

limited weight allowance and a surcharge above this limit;

quick aircraft turnover (45 min when landed vs. 4 hours for a regular airline);

polyvalent staff (crew does the cleaning after landing and is ready to depart again);

departure and arrival times under constraint (cheaper airport fees early morning or late evening);

no-transportation activities purchased from suppliers (e.g. snacking and entertainment);

As a result, on similar flights, such as London-Auckland, Virgin Atlantic can offer tickets c.30% cheaper than British Airways offering free-of-charge snacking and entertainment and where crew is only recruited for services onboard (Balmforth, 2009; Gaskell, 1999).

1.1.2 Differentiation

A company adopting a differentiation strategy seeks to provide the market with a product different than the competitors’. The driver for this strategy is to of...

Table of contents

Cover

Front Matter

1. Accounting for What Counts in the Value Chain in a Way That Counts

2. Product Life Cycle Accounting and Target Costing

3. Performance Management and Measurement

4. Strategic Planning and Forecasting

5. Beyond Budgeting

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Strategic Management Accounting, Volume I by Vassili Joannidès de Lautour in PDF and/or ePUB format, as well as other popular books in Betriebswirtschaft & Buchhaltung. We have over 1.5 million books available in our catalogue for you to explore.