'Subtle and compelling.' Observer

'One of the best books of 2021.' The Times Are we in the middle of a generational war? Are Millennials really entitled 'snowflakes'? Are Baby Boomers stealing their children's futures? Are Generation X the saddest generation? Will Generation Z fix the climate crisis? In this original and deeply researched book, Professor Bobby Duffy explores whether when we're born determines our attitudes to money, sex, religion, politics and much else. Informed by unique analysis of hundreds of studies, Duffy reveals that many of our preconceptions are just that: tired stereotypes. Revealing and informative, Generations provides a bold new framework for understanding the most divisive issues raging today: from culture wars to climate change and mental health to housing. Including data from all over the globe, and with powerful implications for humanity's future, this big-thinking book will transform how you view the world.

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Chapter 1

Stagnation Generation

‘The Baby Boomers – Can They Ever Live as Well as Their Parents?’ This was the anxious question posed by Money magazine in March 1983.1 The implied threat to the generation’s financial security was seriously undermined by the accompanying photo shoot of a real-life couple, which contained glimpses of a luxurious and tastefully decorated (for the 1980s) home. The cover line offered a more direct spoiler: the couple were ‘Not yet 30’ but had ‘two strong careers and a prospering business on the side’. It’s clear that they were hardly the 1980s equivalent of minimum-wage employees toiling in an Amazon warehouse on zero-hour contracts, supplementing their meagre earnings by trading on eBay and waiting for their jobs to be taken by drones.

Of course, Money magazine had a particular target market – well-off middle managers who were interested in tables of mortgages and tax-efficient saving schemes. That makes the uncertainty implied in the question all the more striking now, when we know how things turned out. The question ‘Can they ever live as well as their parents?’ reflects the fundamental belief that animates the ‘social contract’ between generations. As individuals, we have a deep desire for our children to do better than us, and we’ve become accustomed to guaranteed generation-on-generation progress across society as a whole.

It’s easy to forget that progress was not always a given for Baby Boomers. Several serious economists raised doubts about their financial future. In his 1980 book Birth and Fortune, Professor Richard Easterlin argues that being part of a big cohort like the Baby Boomers is bad for your economic success, given the competition for education, resources and jobs. Being a member of a smaller cohort, like the inter-war generation, marks you out as part of the ‘lucky few’, where wages would rise as demand for workers outstripped supply. That seemed a perfectly reasonable assumption to many then, but, as David Willetts outlines in his 2010 book The Pinch, globalization entirely changed the calculation.

After countries with lower labour costs like China opened up to world trade in the 1990s, the generations following the Boomers had to compete with many more people, which kept wages down. As Willetts puts it: ‘The Boomers gain in two ways. When it comes to political power and all the decisions taken by national governments, they are a big cohort. But when it came to the post-war global labour market they were part of a small cohort: they were a scarce resource that could get away with charging a higher price for their labour.’2

Downward trends in financial progress in many Western countries came after the Baby Boomers were well established in their careers and more able to weather the storm. And then came the 2008 financial crisis. Before the COVID-19 pandemic, this was the generation-defining economic event and the cause of a largely lost decade that hit younger generations particularly hard. There were tentative signs of a recovery in generational progress in the late 2010s, which has made the timing of this latest generation-defining shock even more cruel.

The net effect has been that income growth for younger generations in many countries has ground to a halt or reversed, while the vast majority of gains in wealth that we have seen in the last decade or so have gone to older generations. A generational perspective, separating period, cohort and lifecycle effects, is vital if we are to understand how these shifting economic conditions have utterly changed the life course of whole cohorts. Not only have your chances of economic success been affected by the accident of when you were born, but they are also affected by your parents’ assets – to an increasing degree.

Poorer longer

The UK-based think tank the Resolution Foundation has analysed personal incomes across the US, the UK, Spain, Italy, Norway, Finland and Denmark, using data that stretches all the way back to 1969, when the oldest Baby Boomer was 24 years old. The study compares average disposable real incomes – that is, adjusted to take inflation into account and after subtracting housing costs – for three five-year slices of cohorts, to compare generations when they were the same age: in their thirties (Millennials vs Gen X, Gen X vs Baby Boomers), forties (Gen X vs Baby Boomers, Baby Boomers vs Pre-War) and sixties (Baby Boomers vs Pre-War).3 It shows a cascade of ever-decreasing gains for each new generation.

Baby Boomers enjoyed significantly improved incomes in middle age compared with the Pre-War generation, up 26 per cent aged 45 to 49. At the same age, Gen X started off well compared with Boomers, but their incomes stalled as they ran into the aftershocks of the 2008 recession, which hit when the oldest were in their early forties, and ended up only 3 per cent ahead of Boomers. Most strikingly, Millennials’ real disposable income was actually 4 per cent down on Gen X when they were each in their early thirties. Progress didn’t just stall, it reversed – driven by the financial crisis.4

These averages hide significant variation across countries. One of the best places to be a Millennial is Norway. There, Millennials aged 30 to 34 earned 13 per cent more than Gen Xers at the same age. Not too bad, you might say (while researching Norwegian work visa requirements). But this still represents a slowing down in economic progress: at the same age, Gen Xers earned 35 per cent more than Baby Boomers.

More typical is the pattern in the US. Gen Xers had 5 per cent lower real incomes than Boomers at 45 to 49, while Millennials earned 5 per cent less than Gen Xers at 30 to 34.

As demoralizing as things are in the US, they’re nothing compared with elsewhere. In Italy, Gen Xers had 11 per cent less income than Baby Boomers at 45 to 49, while Millennials had 17 per cent less income than Gen Xers at 30 to 34. This is not so much a ratcheting down as a freefall.

The trends in the UK have not been as dire, but they still represent a shuddering halt to progress, particularly with Millennials. Data from 2018 shows that Gen Xers were slightly ahead of where Baby Boomers were when they were in their mid-forties, but Millennials were slightly behind where Gen Xers were when they were in their early thirties.5

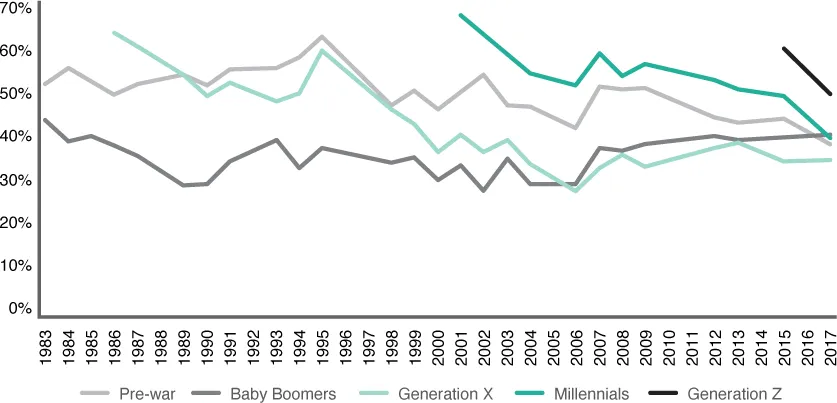

These economic realities are powerfully reflected in how the different generations in Britain feel. This is a key question, because if groups feel hard done by, they’re more likely to question the entire social contract. Since 1983, the British Social Attitudes survey has asked people what income group they identify themselves as being in: high, middle or low. And when we look at the proportions of each generation placing themselves in the ‘low income’ group over the past three and a half decades, in Figure 1.1, we can see huge life stories being played out in five simple lines.

Figure 1.1: Percentage of adults in Britain saying they have a ‘low income’ when asked, ‘Among which group would you place yourself: high income, middle income or low income?’6

One sad story stands out. Look at the gap between Millennials and all other generations for the years between 2008 and 2015. It is not normal for this many people in their early to mid-career (the oldest Millennial was 35 in 2015) to feel poorer than the rest of the population, including retired generations, for so long.

A large part of the explanation for the relative experience of Millennials is the remarkable fall in the proportion of people in the oldest living cohort, the Pre-War generation, who count themselves as having a low income over the last couple of decades. The trend is especially unusual given the changing labour market position of this group during this period. In 1983, only 26 per cent of the Pre-War generation had retired – but by 2017, when the youngest was 72, nearly all had retired.

While this may partly be due to decreased expectations (people generally expect to have less money in retirement), it also reflects the much stronger pension position for many in this generation compared with the generation before them, and compared with working-age people today. The UK’s Office for National Statistics estimates that the average pensioner’s disposable real income increased by 16 per cent between 2008 and 2018, while it increased by only 3 per cent for working households.7 By 2016, net incomes after housing costs were actually £20 per week higher for the retired than they were for working-age people, having been £70 per week lower in 2001. That’s a huge switch. More than this, the pattern extends down into the poorest ends of each group. The poorest fifth of working-age households are getting by on £2,000 less per year than the poorest fifth of pensioners.8

The end of the chart appears to promise a hopeful future for younger generations, with a steep drop in the proportion of Millennials who said that they had a low income, and Generation Z having entered adulthood much closer to the overall average than Millennials did. These are still the two generations that are most likely to feel poor, but the difference is less than in the recent past. It is too early to assess the lasting impact of the COVID-19 pandemic on incomes, but the signs are that these faint glimmers of optimism will be snuffed out. Analysis across China, South Korea, Japan, Italy, the US and the UK shows that everywhere except South Korea, the young are much more likely than others to have already experienced a drop in income, with the UK seeing one of the biggest relative declines.9

Blaming the victim

These major shifts in income make the ‘advice’ that is regularly targeted at these younger generations particularly maddening. ‘Small “Swaprifices” Could Save Millennials Up to £10.5bn a Year’10 was one especially toe-curling example of this trend, in a press release from Barclays Bank in 2019. Not only does it confirm that awful attempts at catchy portmanteau words should be a sackable offence, it also typifies the victim-blaming of young people for their tough financial circumstances.

The thrust of the ‘analysis’ was a breakdown of how young people spend £3,300 per year on daily treats, going out and fashion, followed by some finger-wagging about how this group could save a ‘whopping’ amount by making ‘minor changes to their spending habits’.11 Of course, £3,300 is not a huge amount to cover all those different types of spending in a year, especially when they include things like ‘food’ and ‘clothing’. Even the frivolous-sounding ‘daily treats’, for example, totalled just £441 a year, or about £1.10 per day.

This is typical of the curious double whammy experienced by younger cohorts today. Not only have they had a much tougher time financially, but they are also criticized for the reduced spending they do manage. It’s also a case of us missing the real shift in circumstances. In the UK, for example, over-fifties account for around one-third of the population but 47 per cent of consumer spending, which has increased by eight percentage points since 2003.12 In the US, overfifties already account for more than 50 per cent of spending, and they’ve been responsible for more spending growth in recent years than any other cohort.13 The figures are staggering: the American Association of Retired Persons (AARP) estimates that, in the US, the over-fifties spend nearly $8 trillion each year – more than the combined GDP of France and Germany.14

A new consumption gap has opened up between younger and...

Table of contents

- Cover

- Generations

- Title

- Copyright

- Contents

- Introduction

- Chapter 1: Stagnation Generation

- Chapter 2: Home Affront

- Chapter 3: Reaching Higher, Falling Flat

- Chapter 4: Happy Now

- Chapter 5: A Healthy Future?

- Chapter 6: The Sex Recession, Baby Bust and Death of Marriage

- Chapter 7: Manufacturing a Generational Culture War

- Chapter 8: Constant Crises

- Chapter 9: Consuming the Planet

- Chapter 10: Us and Them

- Chapter 11: The End of the Line?

- Acknowledgments

- Endnotes

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Generation Divide by Bobby Duffy in PDF and/or ePUB format, as well as other popular books in Social Sciences & Forecasting. We have over 1.5 million books available in our catalogue for you to explore.